After reaching lows in December, stocks have rebounded sharply, with strong breadth, as some of the worst fears appear to have subsided. But there are still uncertainties that are likely to cap near-term gains and/or lead to elevated volatility.

Earnings season has been mixed, with the main message appearing to be slowing growth but no near-term recession. The Fed has turned more dovish and is likely on hold for a while, depending of course on incoming data.

China’s economic slowdown is also causing concern, and the different way they are attacking the problem has generated more questions than answers.

“All of life is peaks and valleys. Don’t let the peaks get too high and the valleys too low.” - John Wooden

Treading lightly

U.S. stocks have rebounded sharply since the crescendo Christmas Eve lows, but some important headwinds remain. This is the nature of being late in a cycle, with often competing headwinds and tailwinds—and is the definition of volatility (sharp moves in both directions). The rally has had strong breadth conditions accompanying it, but it’s also taken U.S. stocks from deeply oversold technically in December to marginally overbought now. Oversold conditions developed as investors faced recession, trade fears and tighter financial conditions. At the late-December low, investor sentiment, according to the Ned Davis Research Crowd Sentiment Poll, reached pessimism levels. Stocks have since recovered more than half their losses as monetary policy has shifted in a dovish direction and financial conditions have eased; which has led to sentiment rebounding to a more neutral level. Breadth health of the rally aside, we believe this is more likely the correcting of oversold conditions rather than the start of a renewed robust uptrend. There are still plenty of uncertainties that could go either way, resulting in our continued mostly neutral and somewhat defensive posture. Such a stance will likely feel somewhat frustrating during sharp rallies, and also if there are renewed sharp downturns, but overall we believe is the right stance for investors to be able to mostly participate in rallies while still having some defense on the downside. Volatility has declined from the spike we saw late last year but still remains somewhat higher than the low levels seen in 2017. We think that year was the exception, rather than the new rule; and that a higher (read: normal) level of volatility is likely to persist this year.

VIX down from spike but still above recent years

One of the biggest uncertainties facing investors is the China/U.S. trade dispute, and the continued mixed messages regarding progress or lack thereof. Rumors of a possible decline in U.S.-imposed tariffs helped support stocks, while differing reports of potential meetings between the two nations seems to have only confused investors and caused some tumultuous intraday trading activity. The risk is not necessarily binary—i.e., deal or no deal. Improving relations and no new tariffs would likely be a positive development, while if the currently [scheduled March 1 increase in tariffs comes to pass, it would likely be a market negative and almost certainly an economic negative. We admit to having no idea how President Trump or President Xi will proceed, contributing to our current more cautious stance. We do believe that trade will be an important factor in determining the length of runway between now and the next (inevitable) recession.

Corporate mixed messages

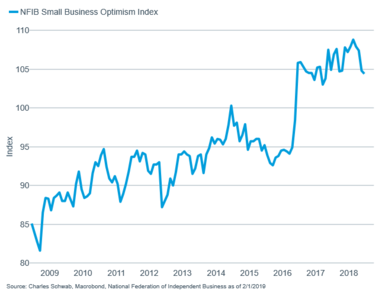

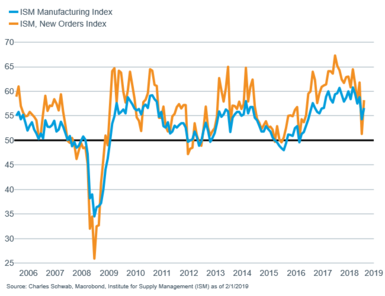

Companies have largely been echoing the uncertainty surrounding the trade standoff, which has contributed to mixed commentary coming out during earnings season (for more on earnings season read Brad Sorensen’s Gauging the Economy Through Earnings). The good news is that, for now, investors are no longer punishing stocks regardless of earnings results, which was the case last year. Although the “beat rate” is a historically-subdued 70% so far this season (FactSet), we’ve observed that companies beating expectations have been generally rewarded with higher stock prices—likely reflecting the relatively low expectations coming into the reporting season. Overall, companies are supporting the view we expressed in our 2019 outlook, which is that trade and other uncertainties have meaningfully dented “animal spirits.” It’s been witnessed in several important confidence measures, which have recently faltered, including the National Federation of Independent Business (NFIB) optimism index, the Institute for Supply Management (ISM) Manufacturing Survey, although we saw an encouraging rebound in the most recent reading, and Duke’s CFO Outlook survey. In fact, when the latter was released in December, it showed that nearly half of U.S. CFOs believe the U.S. economy will be in a recession by the end of this year.

Business confidence coming off the boil

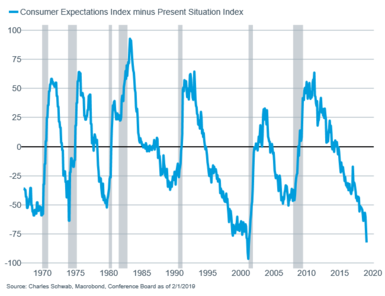

It’s not just business confidence that has suffered. When The Conference Board recently released its version of consumer confidence, it showed a plunge in the “expectations” component of confidence relative to little change in the “present situation” component. The spread between these two components recently hit a near-record low, which historically has been a consistent recession warning signal. It’s too soon to declare the trough in, but it rightly received a lot of investor attention upon its release.

Consumer expectations dampened

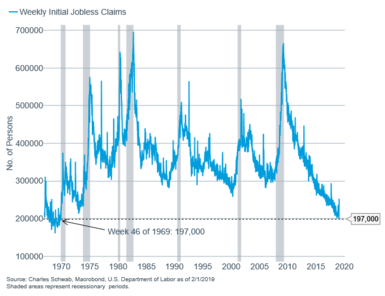

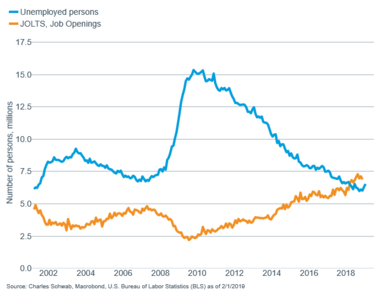

But all is not doom and gloom. Although up on a spike in the past week, potentially impacted by the government shutdown, unemployment claims remain near historically low levels and job growth remains strong; with the January jobs report reporting a robust gain of 304,000 jobs, although the previous month was revised lower by 90,000 jobs, to a still-good 222,000 gain, while the unemployment rate ticked 0.1% higher to 4.0%, attributed to the household survey counting of furloughed Federal workers—a temporary condition.

Claims spiked, but likely just short-term

As the labor market remains tight

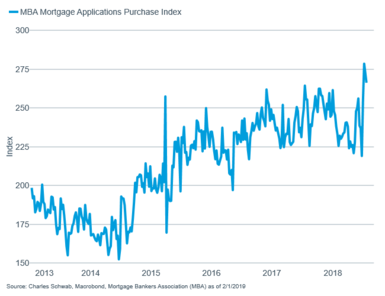

Mixed messages continue with the recent economic data, as regional surveys diverged. The Empire Manufacturing Survey declined to close to zero and the Richmond Fed Index remains below 0; while the Philadelphia Fed Survey improved, with the new order component rising to its highest level in six months. Adding to the weaker side of the ledger was a negative reading for Leading Economic Index (LEI) released by The Conference Board (for more on the LEI read Two Out of Three Ain’t (Good): Leading Indicators Falter Again). More positively, industrial production as reported by the Federal Reserve, rose a decent 0.3%, with capacity utilization also posting gains. The mixed message defines the housing arena as well; with existing home sales as reported by the National Association of Realtors falling 6.4%, but mortgage applications rebounding alongside lower mortgage rates.

Mortgage applications showing signs of potential housing improvement

Fed and government also contributing

As of the January meeting of the Federal Open Market Committee (FOMC) meeting, the Fed is now off auto pilot and expressed a much more dovish outlook than what had been expected. The lack of a move on rates was completely baked in to expectations, but the accompanying statement from the FOMC not only had a more dovish tilt, Fed Chair Jerome Powell’s comments on the Fed’s balance sheet were move dovish as well, with the ongoing balance sheet runoff also not on auto pilot. While this more dovish turn by the Fed was cheered by markets, uncertainty over further moves could contribute to volatility, which could be a bit binary. If the Fed is “right” in pausing because the economy is slowing more quickly than they or investors expected, markets could falter. Alternatively, if the labor market continues to tighten, and additional wage growth takes hold, concerns could elevate that the Fed has positioned itself behind the curve. It’s a bit of a pickle for the Fed.

In other D.C. news, the ending of the government shutdown was a relief given growing risk that a full-quarter shutdown could have wiped out much of the expected real gross domestic product (GDP). There are still economic consequences, but they are likely to be relatively minimal and likely to be followed by some semblance of a rebound. The Congressional Budget Office (CBO) is estimating a roughly 0.02% negative impact on full-year 2019 GDP. But the longer-term effects on confidence in the U.S. government’s ability to function properly are yet to be fully fleshed out, but may represent the more long-lasting impact.

China’s new approach to growth

The world’s second-largest economy is also causing some consternation as China’s economic slowdown is having a broad impact on global companies across sectors. An increasing number of companies in the United States and elsewhere are citing China as a source of weakness in their earnings results and outlooks, as you can see in the few random examples below from recent company earnings conference calls:

PP&G Industries: “In our Industrial Coatings reporting segment, sales volumes were negatively impacted by very weak industrial production activity in China. In the quarter, automotive builds were down 16% in China for the industry, with lower builds in each successive month during the quarter.”

Royal Phillips: “Consumer sentiment in China is a bit more subdued currently.”

AO Smith: “China sales were down 3% in local currency as the China economy continued to weaken.”

Texas Instruments: “On a regional basis, demand in China was weaker than the other regions.”

Lear: “Equity earnings were down year-over-year in the fourth quarter and full year, primarily due to weakened production environment in China”

The economic slowdown is evident even in the official GDP numbers compiled by China’s National Statistics Bureau. Last year ended with the slowest pace of year-over-year GDP growth in nearly 30 years. The pace of growth is now lower than that seen during global financial crisis of 2008-09, when a deep global recession took place.

China’s GDP growth ended 2018 at the weakest pace in decades

Source: Charles Schwab, Bloomberg data as of 1/29/2019.

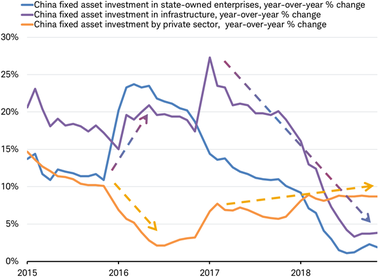

Current efforts by Chinese policymakers to stimulate the economy look very different than in the past. Looking back to the early-2016 slowdown in China, government support for the economy came in the form of infrastructure spending and loans to government-owned businesses known as SOEs, or state-owned enterprises. In contrast, capital spending by private businesses slowed sharply during that period.

Government vs. private sector: it’s different this time

Source: Charles Schwab, Bloomberg data as of 1/29/2019.

It now looks very different as the latest slowdown has unfolded over the past year. The current slowdown has been accompanied by a sharp deceleration in infrastructure spending and loans to SOEs; while private businesses have continued to invest at a solid pace (a pace similar to nominal economic growth, or real GDP plus inflation, of around 8%), as you can see in the chart.

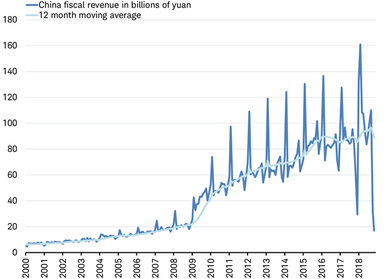

Current efforts by the Chinese government to support the economy have mirrored western governments’ efforts this time—focusing on tax cuts rather than infrastructure or support for SOEs. In fact, government revenue in China has slowed so sharply from tax cuts that November was the lowest of any month during the past 10 years (recall that 10 years ago China’s economy was half the size it is today).

Tax cuts: China’s government revenue has dropped to lowest level in 10 years

Source: Charles Schwab, Bloomberg data as of 1/29/2019.

China isn’t the only country pursuing tax cuts (for more on that read our recent article: Tax War: Will Global Competition to Lower Taxes Lift Growth?). The downside to China’s new approach is that tax cuts do not generally affect the economy as quickly as direct government spending. This may account for the lingering slowdown. Potentially, more may need to be done before the boost to private investment and consumption is large enough to offset the slowdown in government spending, and able to bring about a revival in China sales for global companies.

So what?

It’s difficult to get good footing in a market that has so many mixed messages bombarding it. We recommend patience, discipline and diversification as expect continued bouts of volatility. The U.S. government shutdown is over, for now…and the Fed is in pause mode, for now…but confidence in government is low and monetary policy is likely to persist. In the near term we believe the most important needle-mover will be the result of trade negotiations between the United States and China. The problem is the inability to gauge the likely outcome.