The sharp rebound in U.S. stocks since the Christmas Eve 2018 low has been a welcome development for the bulls, but we are concerned that the pendulum may have swung a bit too far.

The fourth quarter 2018 earnings season has been healthy, but estimates for this year’s first quarter have descended into negative territory. Meanwhile, the Fed has turned more dovish; but why and for how long are relevant questions.

Trade continues to be at the center of investors’ attention—the recent positive news from talks with China may be overplayed and there are other potential trade disputes simmering.

“Be careful not to compromise what you want most for what you want now.” - Zig Ziglar

Too much of a good thing?

Equity investors have been cheering the sharp rebound seen since the end of last year, with the S&P 500 up more than 16% since the Christmas Eve low. We don’t want to be buzzkills and we enjoy rallies as much as anybody; but just like you can eat too much cake with bad results, equity gains that come rapidly after sharp corrections can have consequences as well. It didn’t take long for sentiment to move from overly pessimistic to overly optimistic according to the Ned Davis Research (NDR) Crowd Sentiment Poll; somewhat concerning given the contrarian nature of investor sentiment, especially at extremes. We believed that U.S. stocks had gotten to oversold levels and were likely pricing in too great a risk of a near-term recession—so a rebound was to be expected. But some of the declines seen toward the end of last year were justified in our minds as economic growth has been slowing, trade uncertainties remain, government dysfunction persists, and corporate sentiment is deteriorating. In short, we don’t believe we’ll revisit the lows seen late last year if a recession remains a 2020 story, but a retrenchment of some of the recent gains seems likely. If a recession looks to be developing this year—and if there is no trade deal and additional tariffs kick in—those market lows could be retested (and beyond).

Economic growth slowing, while an earnings recession becomes more likely

U.S. economic growth, while remaining in positive territory, has definitely slowed courtesy of tighter financial conditions last year, weak global growth, the trade-related denting of “animal spirits,” and the effects of the government shutdown. Retail sales for December were weaker than expected, truck orders have declined, and auto sales have weakened (with inventories climbing 4% month-over-month according to Wards Auto).

Truck orders have weakened

As have auto sales

Also of note has been the upside breakout in initial unemployment claims; as well as the decline in banks’ willingness to make loans, showing more caution among financial firms and providing reduced capital to business.

Banks are becoming more cautious

The old chicken and egg argument comes into place now. Are businesses becoming more cautious because of weaker economic growth and last year’s market swoon; or is the economy weakening a result of reduced business confidence? Regardless, either scenario presents risks for the stock market in the near-term. The Institute for Supply Management (ISM) Non-Manufacturing Index fell in its latest reading, moving to 56.7 from 58.0, while the forward-looking new order component fell more sharply to 57.7 from 62.7—both still above the 50 mark which denotes expansion versus contraction, but not moving in the right direction.

This slowdown is clearly impacting the earnings story as well. Expectations were relatively subdued coming into the fourth quarter 2018 reporting season, which may have helped companies hurdle the bar. At the same time, companies reporting stronger earnings have been rewarded with higher stock prices—in contrast to the general trends of last year. But stocks tend to focus on the windshield, not the rear-view mirror, and the deterioration in earnings expectations for this year are notable. According to Refinitiv (formerly Thomson Reuters) first quarter estimates are now in slight negative territory, with the subsequent two quarters both in low single-digit territory—making the valuation case less attractive (for more on the earnings story read No Quarter: Could 1Q19 Bring Negative Earnings?).

On the other hand

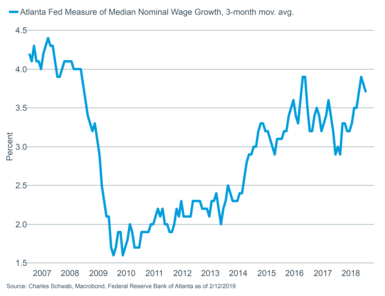

The story is not all bad. Both the ISM manufacturing and non-manufacturing readings remain above 50, the labor market remains strong: 304,000 nonfarm payroll jobs were added in January; and wage growth is improving, with the Atlanta Fed Wage Tracker moving within striking distance of its highest level since the Great Recession.

And wages are trending higher

We’ve heard more positive comments coming out of both China and the United States regarding the ongoing trade dispute. As reported in The Wall Street Journal, Chinese authorities came to the United States to negotiate, while U.S. representatives reciprocated the gesture more recently. But this could be a story of reality being less optimistic than perception. Trade progress is good, but false hopes are bad. We are concerned that investors may be pricing in too-high odds of a substantive deal, leading to risks skewed to the downside should that fail to come to fruition. Additionally—and getting insufficient publicity according to our man in Washington, Mike Townsend—Congressional approval of the recently signed USMCA (United States, Mexico, Canada Agreement) is far from assured; while increased auto tariffs on the European Union are still on the table. These point to lingering trade uncertainty for the foreseeable future (more details on trade below).

More dovish Fed…but why…and for how long?

Some of the U.S. stock market rally since year-end 2018 can be attributed to a more dovish Federal Reserve. At the January Federal Open Market Committee (FOMC) press conference by Chairman Powell, he appeared to go out of his way to emphasize that the FOMC is now “patient” and no longer in the “gradual hike” camp. A more friendly Fed is welcomed, but why the change? Is it because they believe the fed funds rate is near the “neutral rate,” or are they becoming more concerned about both U.S. and global economic growth? Additionally, while fed fund futures are pricing in roughly zero chance of rate hike this year, we can’t ignore the tightness of the labor market and upward pressure on wages. If wages continue to rise, filtering through to the broader economy, the Fed could be forced to step back in—not to move to neutral, but rather to tighten in order to battle a perceived inflation threat. This is a risk likely underappreciated by investors, which could contribute to greater volatility as we move through the year.

Trading places

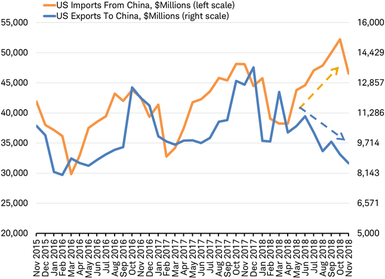

It usually takes quite a bit to wrestle attention away from the Fed, but trade seems to have done that as of late. The U.S.-China trade dispute deadline of March 1 may have gotten a reprieve, with President Trump open to letting the 90-day “trade truce” be extended; meaning an extension to the increase in tariffs from 10% to 25% on many imported Chinese goods. Since early 2018, when the United States announced the first set of tariffs, the trade balance between the United States and China has widened, with U.S. exports to China slowing, as you can see in the chart.

Trade gap was widening as U.S. exports to China slow

Source: Charles Schwab, Bloomberg data as of 2/12/2019.

Yet, indications from the Trump administration and Chinese officials suggest an extension of the “trade truce” may be the outcome on March 2. With this extension, we anticipate no increase in tariffs—but no removal of existing tariffs either. The easing of trade tensions seemed to help fuel the January rally in stocks, with an 11% gain in the MSCI China index and an 8% in the S&P 500 index of U.S. companies. But the optimism may have run its course, as the focus of trade disputes may see Europe and Japan trading places with China.

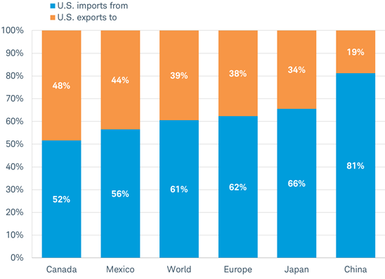

Although U.S.-China trade tensions appear to be cooling, other trade disputes may be heating up, with yet another 90-day window over which investors are likely to fret. The United States’ widening trade gap with China garners much attention, but the United States also has significant trade gaps with Europe and Japan, as you can see in the chart.

Balance of trade with select U.S. trading partners

Source: Charles Schwab, Bloomberg data as of 2/12/2019.

Why now? February 17 is the deadline for the U.S. Department of Commerce to submit its report on automotive imports and U.S. national security, after which President Trump could respond by imposing tariffs within 90 days. Much of the U.S. trade gap between both Japan and Europe is accounted for by auto imports. Threats of auto tariffs by the Trump administration against Canada and Mexico likely helped to obtain concessions on this industry, as well as in other areas in the final USMCA. It seems likely that the threat of auto tariffs may again be used as a tool for negotiating a new trade deal with Japan and Europe.

U.S.-Japan trade talks

In December 2018, the United States released a comprehensive list of goals for the negotiations with Japan. There are a number of items that should be of little contention; since Japan previously agreed to many of these conditions as part of the Trans-Pacific Partnership deal negotiated near the end of the Obama administration. Nevertheless, there are challenges to getting to a deal in 90 days:

The main objective of United States is to lower the trade deficit with Japan. This will likely require auto import quotas, since Japanese cars account for two-thirds (Bloomberg) of the deficit. This is a major issue for Japan since autos drive their economy (pun intended).

Another potential barrier to a deal is the so-called "anti-China clause" that would require Japan to inform the United States before engaging in trade talks with China, or otherwise risk a renegotiation with the United States.

Yet another challenge to a deal may be found in Washington. It is unclear whether House Democrats would approve any U.S. trade deal, given their opposition to President Trump and their track record of disapproving of new trade agreements. This may limit Japan’s willingness to make tough concessions within the 90-day window.

Over the coming 90 days, Japanese stocks may be driven by prospects for a temporary and renewable exemption from tariffs on the auto industry.

U.S.-Europe trade talks

In January, the Office of the U.S. Trade Representative notified Congress of the Trump administration’s negotiating objectives with the European Union (EU). However, Europe is in no position to negotiate over the coming 90 days:

The elections for the EU parliament take place in May, followed by the appointment of a new European Commission in October. Any deals over the coming 90 days might have to be renegotiated to pass a potentially very different body of lawmakers. As populist parties appear set to take more seats, it leaves little incentive to make tough compromises.

The United States has put the opening of Europe’s protected agricultural sector high on the list of objectives from trade talks. Targeting agriculture, combined with threats of auto tariffs, may divide Europe by pitting France, Europe’s agricultural capital, against Germany, Europe’s auto powerhouse. France has already opposed putting agriculture into the scope of the talks with the European Commission.

Over the coming 90 days, European stocks may be driven in part by any progress in negotiations. Resolution of smaller issues, such as non-tariff barriers and regulatory issues, may provide a temporary relief for the EU from auto tariffs, until broader negotiations over a free trade agreement can begin.

Another deadline

Auto tariffs on Europe and Japan could impose a direct trade cost of $30 billion, the same as the escalation of China tariffs estimated at $30 billion—a 15% increase on $200 billion in Chinese goods as planned on March 2 (Strategas Research estimates). Stock market investors remain concerned about barriers to trade, especially as global growth slows. With another 90-day trade window beginning to tick down to a tariff deadline, investors may have fresh concerns that could weigh on stocks. Investors might also downgrade their expectations of a U.S.-China trade deal as they see the Trump administration renew tough talks on trade.

So what?

Markets got a healthy reprieve from last year’s fourth quarter carnage as a few headwinds became tailwinds; including a more dovish Fed, some hopes on trade, strong fourth quarter earnings growth, and an end to the government shutdown. But there are lurking risks, including equities having become technically overbought, and investor sentiment having moved back into the high optimism zone. We continue to recommend investors remain near their long-term equity allocation, using rebalancing during bouts of volatility and keeping portfolios diversified across asset classes.