As is often seen in investing, we believe the pendulum swung too far in the negative direction for equities late last year, but now may have swung a bit too far in the positive direction.

U.S. economic data has deteriorated and the threat of recession, while still relatively low, has risen. The Fed is reading from that playbook, hence its more dovish tilt since it last hiked rates in December.

Slowing economic and sales growth aren’t the only things to be watching—rising wages around the world could pressure earnings and profit margins.

“History has always been a series of pendulum swings, but the individual doesn’t have to get caught up in that.” - Robert Johnson

Complacency danger?

65%! That’s the annualized gain for 2019 if the S&P continues along the pace of gains registered year-to-date. Of course, that’s highly unlikely. And with volatility across asset classes in very low territory, we’re also concerned that a bit of complacency among investors may be setting in.

The sharp rebound…

…and declining VIX cause us concern.

With the winter weather much of the country has seen recently (congrats to those who escaped, those of us who didn’t are jealous), a young driver trying to correct a skid on ice came to mind—they often overcorrect, making the situation worse. We’re concerned that’s the environment we’ve entered as we begin the final month of the first quarter. With the stock market’s gains, alongside a deteriorating corporate earnings outlook, the valuation recovery suggests equities are priced for a stream of good news—a deal with China, a continued-dovish Fed, no inflation, continued economic growth, no damaging Brexit, etc. While we believe there is hope for some of these to come to fruition, it’s a stretch to assume the full crescendo. And with investor sentiment continuing to extend into the overly optimistic zone, according to the Ned Davis Research Crowd Sentiment Poll, contrarian analysis suggests a near-term pullback is increasingly likely.

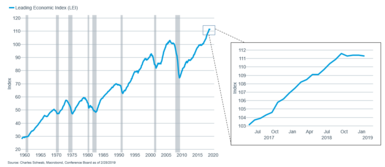

Economy slowing

The recent market gains are in contrast with the slowing in economic data. We’re not calling for a recession in the near-term; but as we often say “better or worse tends to matter more than good or bad,” and the trend in many indicators is decidedly down. Perhaps the best overall picture of this can be seen in the Index of Leading Economic Indicators (LEI) from The Conference Board, which peaked last September and has declined in two of the past four quarters, including last month.

LEI rolling over?

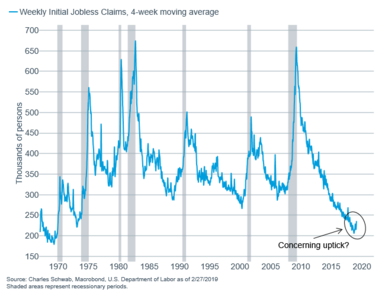

According to the National Association of Realtors, existing home sales, which can impact consumer confidence as homes are the largest asset most Americans own, fell 1.2% in January, to the lowest level since November 2015. That said the recent fall in mortgage rates did help the National Association of Homebuilder Index Housing Market Index (HMI) increase from 58 to 62, revealing relatively healthy optimism among homebuilders. But the weakness in sales could help to reinforce the weak retail sales reading from December, with the Census Bureau reporting a 1.4% drop ex-autos and gasoline. That reading may be a bit skewed as some other reports (MasterCard spending pulse, Johnson Redbook, etc.) regarding holiday spending indicated a more positive season. Nonetheless, the trend in consumer spending has deteriorated. And while the labor market retains its healthy glow, we are watching the forward-looking jobless claims closely, given the general uptrend since last fall. Persistence in this trend, based on history, would suggest elevating risk of a recession.

Uptick in claims concerning

As a result of the deterioration in data, the Atlanta Fed’s GDPNow estimate for this year’s first quarter has dropped from around 2.8% at the beginning of February to 1.8% now; while the New York Fed’s Nowcast is only 1.2%.

Trade hopes and Fed turn

There is little doubt, however, that at least some of the gains seen over the past couple of weeks can be attributed to some positive reports coming out regarding the Chinese/U.S. trade dispute—culminating recently with an extension of the deadline for a deal to be completed before the United States raises tariffs on imported Chinese goods. For now, this is a “can kick” and we remain skeptical that a game-changing announcement is forthcoming. Given the market’s rally since last Christmas, we now believe there may be more market downside if no deal is struck than there is upside opportunity if we get some sort of deal—especially if the deal doesn’t address the longer-term issues around intellectual property theft, patent violations, forced technology sharing, etc. We believe the most likely scenario is an announcement of an agreement that both sides will proclaim as ground breaking; but ultimately won’t change the competitive landscape all that much. As such, this could be setting up as a classic buy the rumor, sell the news scenario. And even if there is a deal in this trade dispute, Congress is making noise about holding up the USMCA (United States, Mexico, Canada Agreement), while the threat of increased tariffs on European autos appears to be accelerating (and is under-appreciated).

However, the major positive that has the potential to counteract some of the above is the clear dovish turn by the Federal Reserve. The release of the minutes from the January Federal Open Market Committee (FOMC) meeting solidified that the Fed is keenly aware of the slowing in U.S. economic growth; while also not, for now, feeling pressure from rising inflation. In fact, the minutes revealed that the Committee is contemplating keeping a larger balance sheet than may have been expected by noting that, “Almost all participants thought it would be desirable to announce before too long a plan to stop reducing the Federal Reserve’s asset holdings later this year (emphasis ours).” That’s sooner than the consensus had expected and could provide a cushion to equities and the economy if the slowdown in growth continues.

Earnings recession?

It isn’t just slowing economic growth that would likely pressure top line corporate revenue growth—rising labor costs also pose a key risk for a potential earnings recession this year.

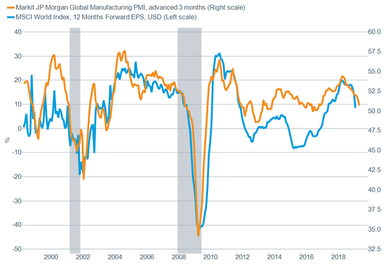

Analysts have been lowering their 2019 earnings forecasts over the past few quarters. The cuts have been tied to last year’s oil price collapse, the effect of the “roll-off” in the corporate tax cuts’ impact on year-over-year earnings growth, and slower global growth. In particular, the global economic slowdown is visible in the widely-watched global purchasing managers’ index (PMI), as you can see in the chart below. Slower sales on the “top line” of the income statement flow all the way down to earnings.

Slowing top line: earnings estimates are tracking global economic slowdown

Source: Charles Schwab, Macrobond, MSCI Barra as of 2/27/2019. Shaded areas represent global recessions.

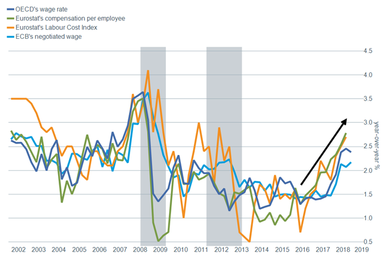

But what about changes in costs—labor and otherwise? If costs are falling too, then the impact of slowing sales growth on the “top line” may be lessened on the “bottom line” of pre-tax earnings. Unfortunately, that doesn’t seem to be the case. In fact, wages—the largest portion of corporate costs—are rising at the fastest pace in a decade. In many major countries, wage growth has finally recovered to levels last seen in 2007, just ahead of the 2008 recession.

There is no one simple way to measure wage growth across the world, but we can look at measures in Europe, the United States, and Japan—encompassing the operations of the vast majority of the companies in the MSCI World Index—and we can see the rising path of wages. Even within a region, like Europe, there are many ways to measure wages—but no matter how they are measured, wages are growing the fastest pace in many years, as you can see in by the upward trend lines seen in the chart.

Rising costs: no matter how you measure it, wages are going up in Europe

Source: Charles Schwab, Macrobond, ECB (European Central Bank), Eurostat, OECD (Organization for Economic Co-operation & Development), Eurostat Database as of 2/27/2019. Shaded areas represent recessionary periods.

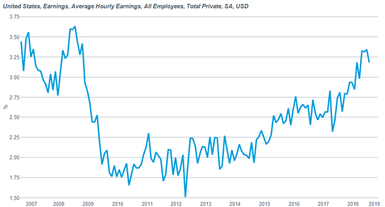

The rising trend in wage growth in the United States can also be clearly seen in the chart, notwithstanding the recent downtick.

Rising costs: wages rising in the United States

Source: Charles Schwab, Macrobond, U.S. Bureau of Labor Statistics (BLS) as of 2/27/2019.

Remarkably, wages are rising in Japan, as well. Not only is wage growth relatively rare in Japan; wages are rising at the fastest pace in decades, as the chart shows a breakout above past wage growth numbers.

Rising costs: wages are rising in Japan at the fastest pace in decades

Source: Charles Schwab, Macrobond, Japanese Official Statistics (e-Stat) as of 2/27/2019.

The tight global labor market is continuing to push up costs even as growth slows; in part because labor is a lagging indicator, and wages tend to peak after the economic recession is well underway (and can take a long time to pick back up again after the start of the recovery).

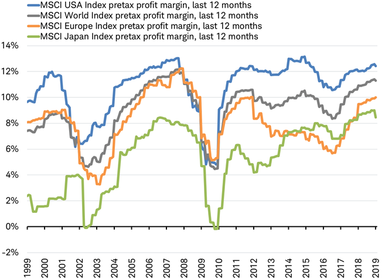

Has the rise in wages finally led to a peak in profit margins? That may be the case. Profit margins have started to slide this year from near-peak levels, as shown in the chart by the downticks in most areas’ margins. Only in Europe do profit margins appear to be still significantly below their prior peaks and have continued to rise. Elsewhere margins are at or near their prior peaks and have ticked down this year.

Peaking profit margins?

Source: Charles Schwab, Factset, MSCI data as of 2/28/2019.

A narrowing of profit margins could result in an earnings recession (falling corporate earnings), even if the overall economy avoids a recession and allows sales to continue to grow, but at a modest pace. To see how this can have a big impact we can use a simple example of a theoretical company that had $100 in sales last year and a pre-tax profit margin of 11.3%. If this year, sales increase 2% while costs rise 3%, it could mean a 6% drop in pre-tax earnings, as shown in the illustration.

Falling bottom line: profits could feel the crunch

Theoretical illustration of costs rising faster than sales.

Therefore, it doesn’t take an economic recession and an accompanying decline in sales to cause an earnings recession. A shift to a focus on the growth in costs, rather than just the weaker outlook for sales growth, might be increasingly appropriate for investors.

While many investors have breathed a sigh of relief that the Fed’s pause of rate hikes may have eased the near-term threat of an economic recession, it may allow cost pressures to continue to rise and pose the threat of an earnings recession.

So what?

Equity markets can swing like a pendulum—moving beyond what fundamentals justify in both directions. We believe the strong rally off the Christmas Eve 2018 lows may be an example of that, suggesting a rising risk of a near-term pullback. U.S. economic data has softened alongside weak global growth, while ongoing trade uncertainties threaten to throw a wrench in stock market gains if deals not to be had. We recommend a modestly defensive position for tactical investors, while keeping an eye on tried-and-true longer-term disciplines like diversification and rebalancing.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. . Supporting documentation for any claims or statistical information is available upon request.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. The policy analysis provided does not constitute and should not be interpreted as an endorsement of any political party.

Ned Davis Research (NDR) Sentiment Poll shows perspective on a composite sentiment indicator designed to highlight short- to intermediate-term swings in investor psychology.

The S&P 500 Composite Index is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The Chicago Board of Exchange (CBOE) Volatility Index (VIX) is an index which provides a general indication on the expected level of implied volatility in the US market over the next 30 days.

Leading Economic Index (Indicators) is an index that is a composite average of leading indicators and is designed to signal peaks and troughs in the business cycle.

The National Association of Homebuilders (NAHB) – Wells Fargo Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to measure homebuilder sentiment in the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. It is a weighted average of separate diffusion indices for these three key single-family series.

Markit J.P. Morgan Global Manufacturing PMI gives an overview of the global manufacturing sector. It is based on monthly surveys of over 10,000 purchasing executives from 32 of the world's leading economies, including the U.S., Japan, Germany, France and China which together account for an estimated 89 percent of global manufacturing output. It reflects changes in global output, employment, new orders and prices.

The MSCI World Index captures large and mid-cap representation across 23 Developed Markets (DM) countries. With 1,632 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

Eurostat Labour Cost Index, abbreviated as LCI, is a short-term indicator showing the short-term development of hourly labour costs incurred by employers, the total cost on an hourly basis of employing labour. In other words, the LCI measures the cost pressure arising from the production factor “labour”.

The MSCI USA Index is designed to measure the performance of the large and mid-cap segments of the US market. With 620 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in the US.

The MSCI Europe Index captures large and mid-cap representation across 15 Developed Markets (DM) countries in Europe*. With 439 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The MSCI Japan Index is designed to measure the performance of the large and mid-cap segments of the Japanese market. With 323 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.