Just over a decade ago, global markets began to recover from the biggest shock in postwar history. In these 10 charts, we aim to show how much has changed since then and how market conditions over the past decade may influence big changes that are beginning to unfold today.

Even as financial markets have rallied in early 2019, uncertainty is still in the air today. Macroeconomic growth, corporate debt, central bank policy and geopolitical risks are all adding to the anxiety. The roots of today’s market conditions can be traced back to the global financial crisis (GFC), the subsequent recovery that began in March 2009 and surprising developments around the world since then. For investors to overcome market challenges and position themselves in today’s complex environment, they should start by taking a closer look at some of the massive changes that have reshaped the financial world we live in today.

After the GFC, extremely accommodative monetary policy lowered market volatility, culminating in an exceptionally calm year in 2017. In 2018, volatility returned to global equity markets and is widely expected to continue this year. Turbulent markets can be unsettling for investors, but also provide more opportunities for active managers to generate returns.

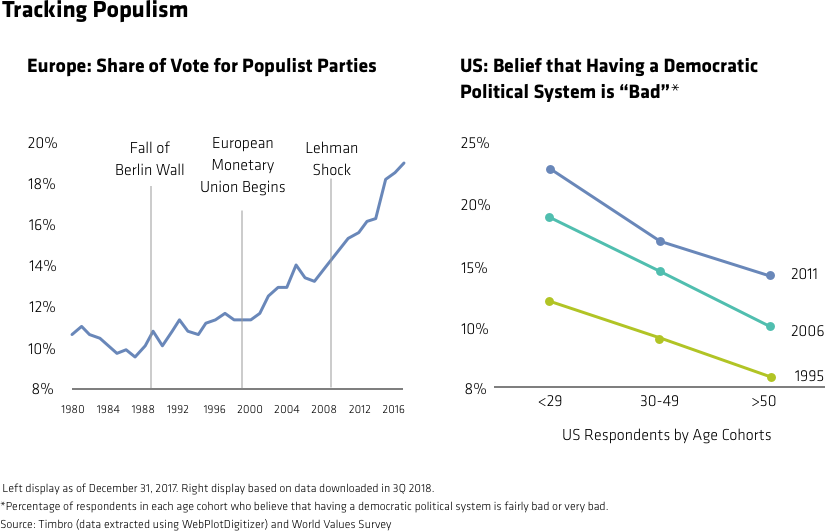

Voters around the world are increasingly turning to populist parties, rejecting mainstream ideas and institutions that have underpinned stability for decades. A blizzard of political risks, from Brexit to trade wars, adds new challenges for economic growth and investors.

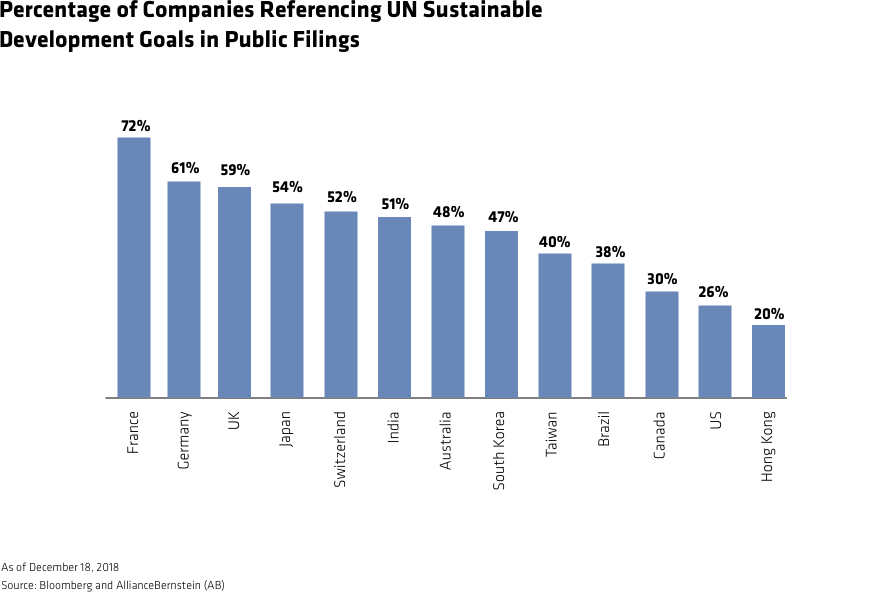

Greater scrutiny of environmental, social and governance (ESG) factors has gained significant momentum over the past decade, and is becoming an essential ingredient for building responsible investing portfolios. Some countries are further along than others, but the trend is clear.

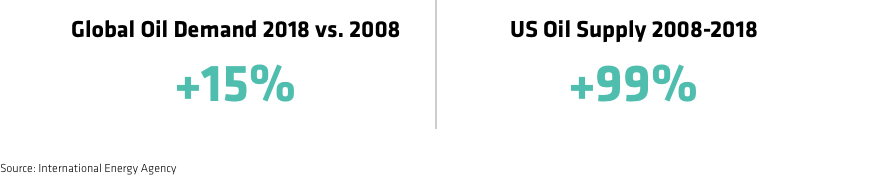

Surging production of US shale oil is making the US less dependent on global oil supplies—and has pushed down oil prices in recent years. But US oil only makes up 15% of global supply, so conventional projects may still be needed in the coming years.

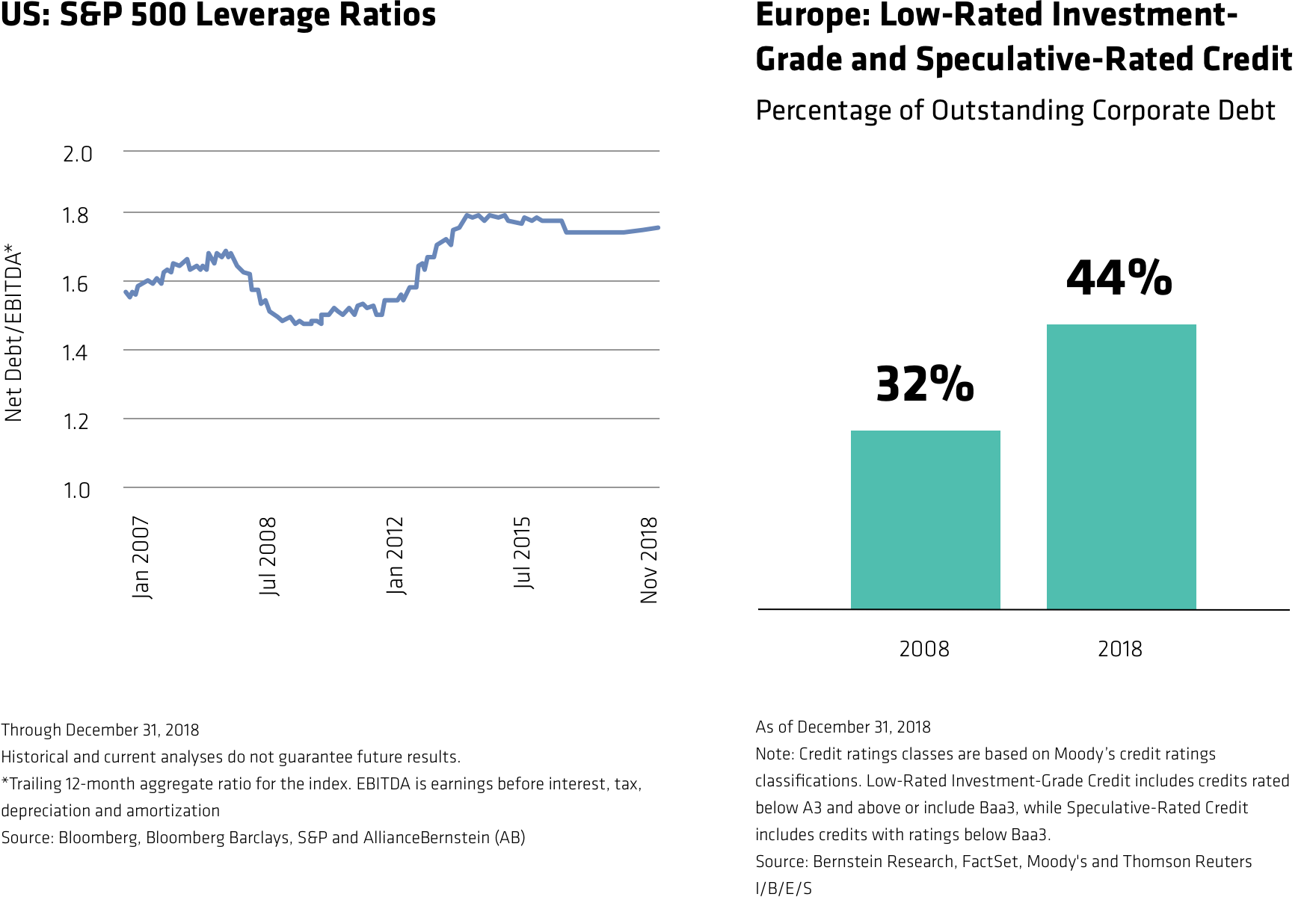

In both the US and Europe, low interest rates have fueled corporate leverage, and the quality of debt has deteriorated. Caution is paramount as quantitative easing turns to quantitative tightening. Selective fixed-income investors can find opportunities in companies with lower-rated debt that have solid fundamentals. For equity investors, it’s important to pay close attention to debt levels and credit ratings when selecting stocks.

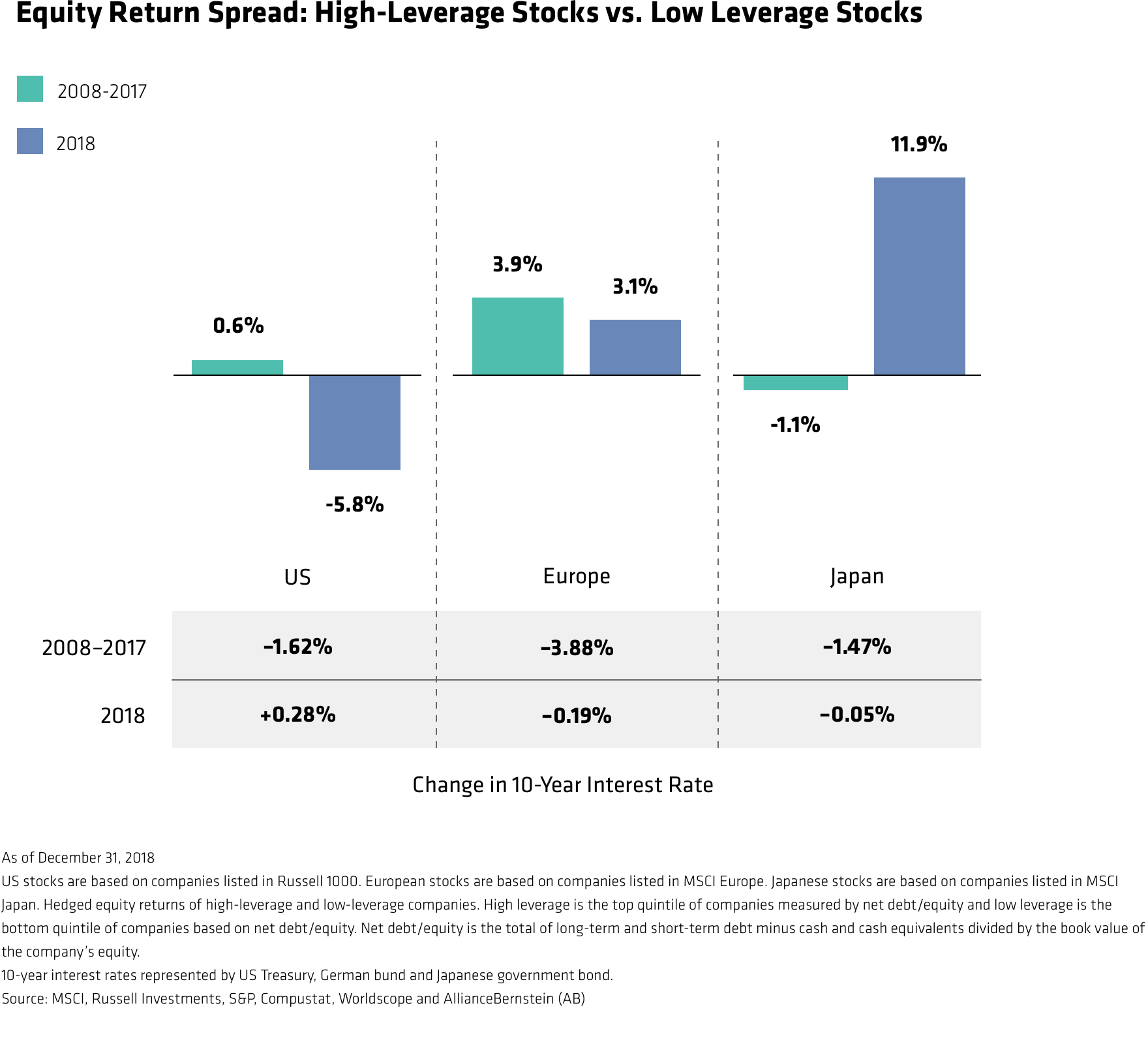

For the last decade, historically low interest rates spurred corporate borrowing around the world. But in 2018, stocks of US companies with higher debt levels underperformed low-leverage stocks as interest rates began to rise. In Europe and Japan, leverage didn’t matter much—but that could change if rates start to rise from near-zero levels.

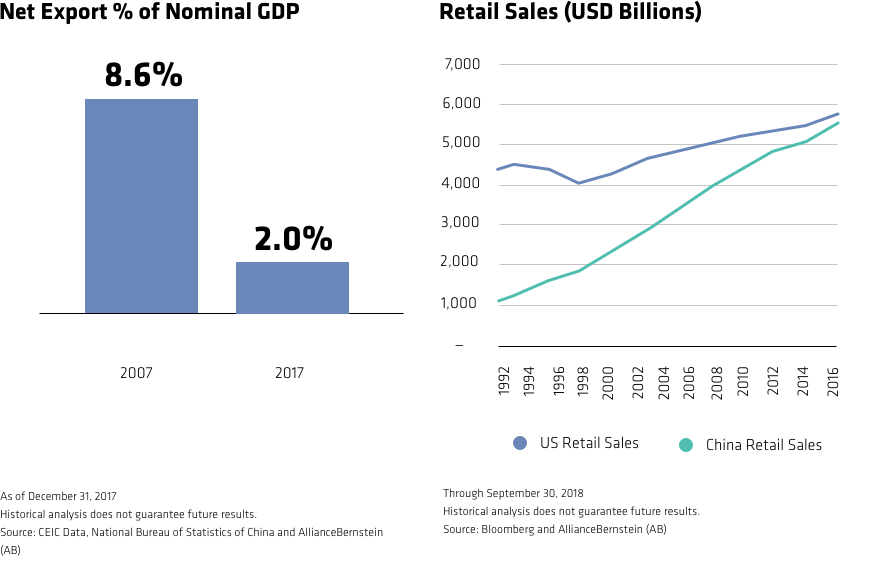

While China’s economic slowdown grabs headlines, the changing composition of its economy will reshape its future growth path. Exports are becoming less important while the domestic retail industry gains dominance. These trends will create new opportunities, and new risks, as the onshore stock market opens to foreign investors.

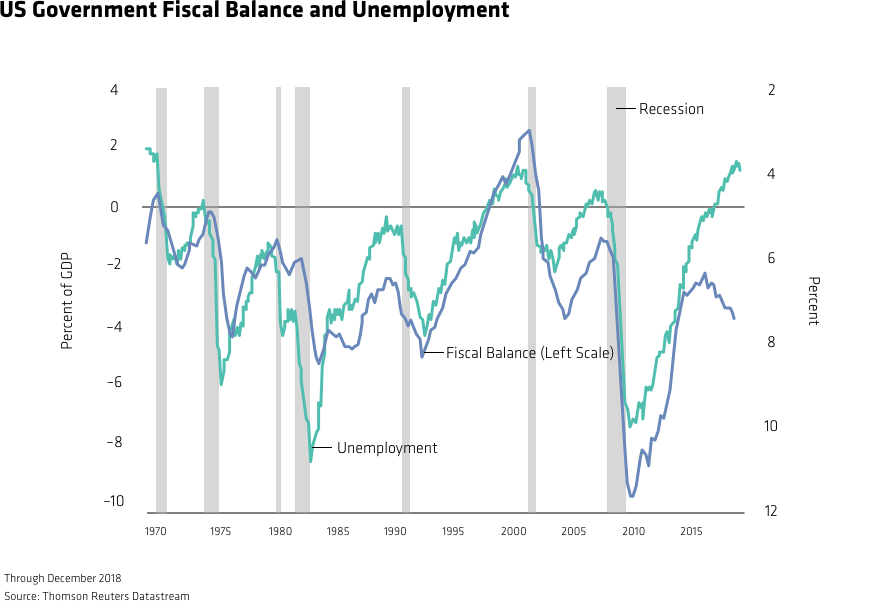

The US deficit typically narrows when unemployment falls. But in recent years, the deficit has kept widening even as unemployment declined. This reflects an unprecedented public spending spree that could have unintended consequences for the stability of the world’s largest economy down the road.

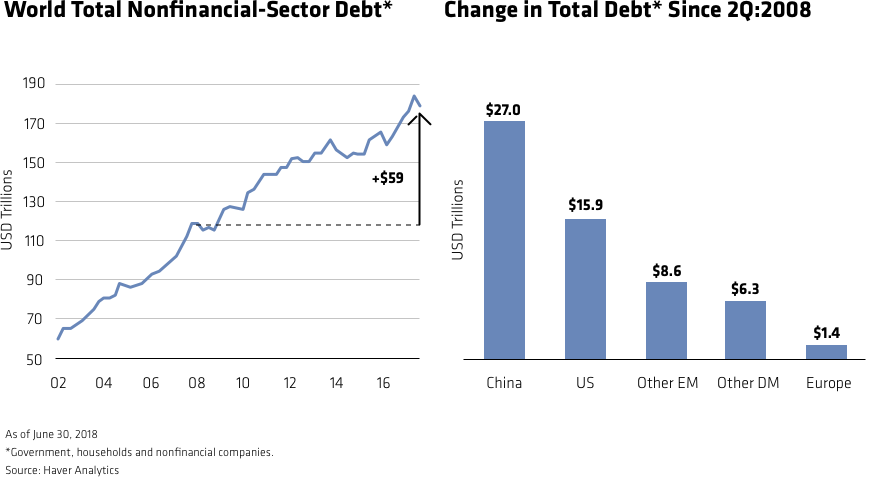

Low interest rates around the world since the GFC have incentivized borrowing. Global debt reached approximately US$178 billion by 2018. China, the US and many other nations have added to their debt burdens over the past decade. Massive debts and stretched balance sheets could be dangerous if financing conditions tighten.

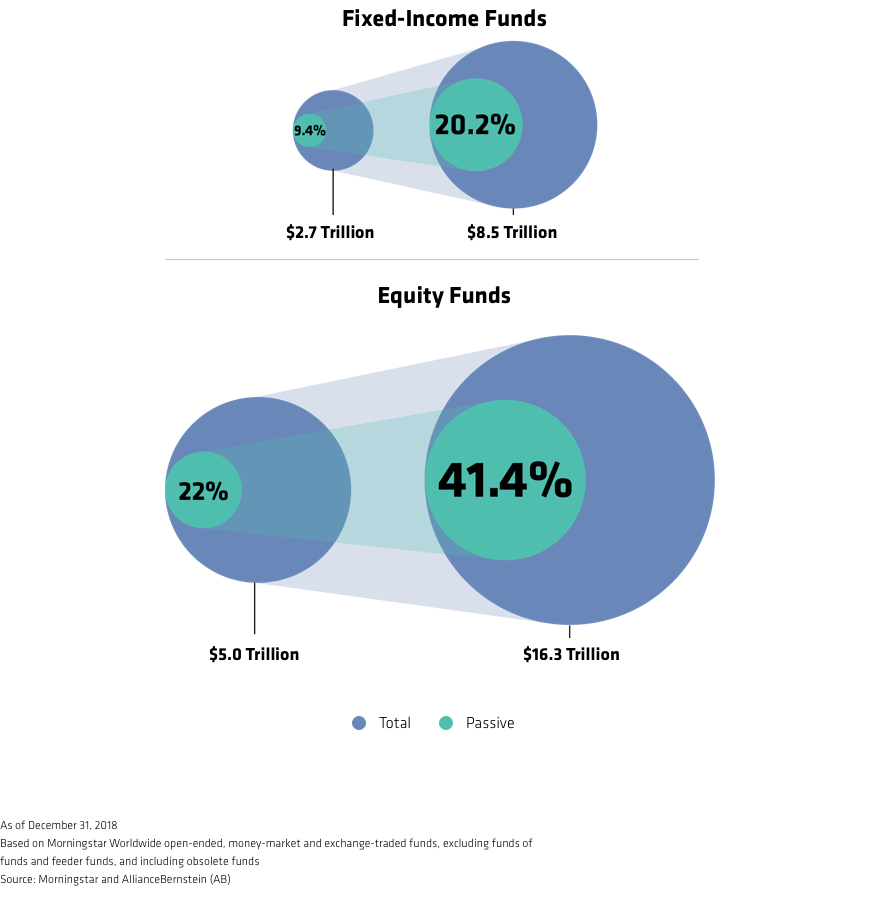

Investors have continued to move their money into passive investment funds that track an index, in both equities and fixed income. While passive funds are cheap, they aren’t risk free. As major imbalances around the world begin to unwind, we believe active investment portfolios are essential to help investors navigate the risks and capture return potential.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein