Last week’s meeting of the Federal Open Market Committee (FOMC) surprised even those who expected a dovish outcome. As the Fed wrangles with its policy framework, one takeaway is clear: don’t expect rate hikes this year—and possibly next.

As recently as six months ago, the committee expected to raise official short-term interest rates three times this year. Now, it doesn’t expect to raise rates at all in 2019. Sure, the FOMC’s economic forecasts have deteriorated, but only modestly. Much too modestly, in fact, to justify such a big swing in the committee’s rate-hike expectations.

We think two factors are behind the sudden shift: a reassessment of what the “neutral” interest rate actually is and recognition that inflation has been too low for too long.

The Neutral Interest Rate Has Been Creeping Lower

In economic theory, the neutral interest rate is the rate that doesn’t encourage or discourage inflation, assuming no external shocks jumble the picture. Nobody really knows what the actual neutral interest rate is. It’s best to think of it as a range of rates, as the Fed has emphasized recently.

The FOMC has steadily lowered its median estimate of the neutral rate during this expansion, from 3.75% in 2018 to 2.75% today. Several members think it may be lower. There’s uncertainty in the estimates, and this seems to have convinced many in the FOMC that the market disruption after December’s rate hike is a sign that we’ve already reached neutral. These members don’t think we need any more hikes until inflation warms up and hints at an overheating economy.

The Case of the Missing Inflation

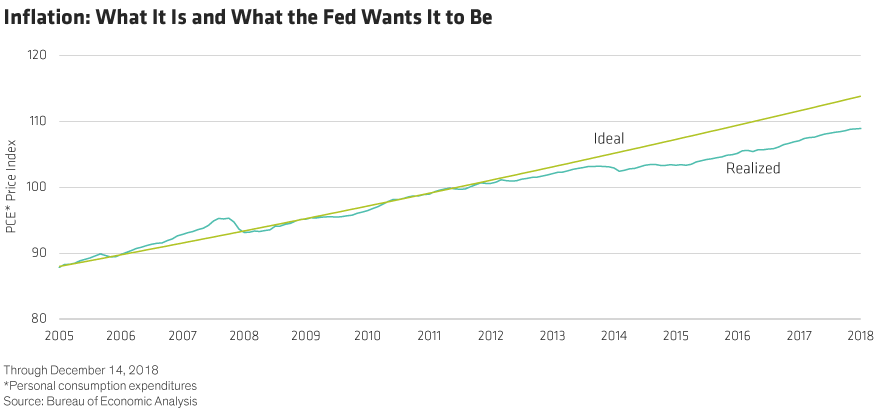

The second factor behind the Fed’s aggressively dovish pivot runs even deeper. As we see it, several FOMC members, including most of the influential monetary policy thinkers, worry that inflation and inflation expectations are simply too low (Display).

The logic is simple: The Fed wants to keep inflation averaging 2% across the business cycle. And inflation typically runs well below 2% in bad economic environments. If that’s the case, the Fed must target inflation rates higher than 2% in good economic environments to keep the average at 2%. The Fed hasn’t really done this. Using the committee’s preferred price index, inflation has averaged a meager 1.3% over the past five years and 1.4% over the past 10 years.

That’s a lot of “missing” inflation.

Market-based measures of inflation expectations reflect the shortfall. Break-even inflation rates have been about 60 basis points lower over the past five years than they were in the decade before that. Inflation expectations play a big role in determining actual inflation, so if the market believes the Fed won’t tolerate 2%-plus inflation, we may be looking at a self-fulfilling prophecy.

Will the Fed Encourage Inflation to Run Hotter?

How could the Fed fix the inflation mechanism? As this camp within the FOMC sees it, the path would be to encourage inflation above 2% during economic expansions. For starters, that would mean not raising interest rates even if inflation starts to bubble up. With inflation cool right now, there’s no reason at all to raise rates in the foreseeable future.

The inflation topic is clearly on the Fed’s radar. The FOMC has formed a committee to study its monetary policy framework, and we expect the result to be a pivot to an explicit “makeup” strategy, with the Fed trying to boost inflation in good times. Vice Chair Richard Clarida hinted at this approach in an overlooked but very important speech in February.

Rate Hikes Not Likely This Year…or in 2020

This pivot isn’t full-fledged yet, but the combination of a lower neutral-rate estimate and a higher inflation threshold implies that rate hikes aren’t likely to happen in the near future. We no longer expect any hikes in 2019 or in 2020. And, in our opinion, we think it would take a big jump in inflation to push the Fed back into tightening mode.

Eric Winograd is a Senior Economist—Fixed Income

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

More Fixed Income Topics >