U.S. stocks resumed their uptrend after a short respite, but with the economy slowing, the yield curve inverted, and earnings likely negative for at least the first quarter, the risk of a pullback appears elevated.

The first quarter was highly likely weak for both earnings and the economy overall; but it could be followed by at least a modest rebound in the second quarter if traditional seasonal patterns hold. Given the slowdown, the Fed is now forecasting no rate hikes in 2019, which suggests binary risks of either slower growth than expected, or higher inflation than expected.

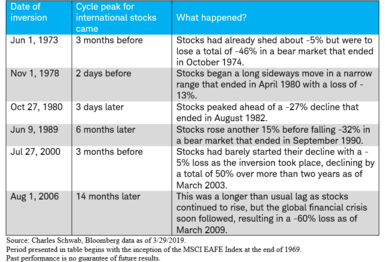

The recent inversion of the most widely-watched U.S. yield curve is not only a sign of rising recession risk, it can also be instructive as to international markets as well.

U.S. stocks have continued their sporadic move higher, after a short-lived dip associated with the inversion of the yield curve (read more in Liz Ann’s article Blue, Red and Grey: Yield Curve Inversions); recovering much of their fourth quarter 2018 losses. We never scoff at rising equity prices, but we are becoming increasingly concerned that gains have exceeded the fundamental underpinnings, at least near-term.

Uptrend intact—but too far too fast?

Positive macro supports have been evident, including hopes for a trade deal with China and the 180 degree turn toward dovishness by key central banks, including the Federal Reserve and the European Central Bank (ECB). There are also some temporary factors which put downward pressure on first quarter growth, including severe weather and the government shutdown. That said we are concerned that those positive vibes may be obscuring some potentially negative developments; not least being the message the bond market and yield curve has been sending.

In keeping with rally, investor sentiment, according to the Ned Davis Research Crowd Sentiment Poll, is back in extreme optimism territory, while valuations have moved back into elevated territory. The forward P/E for the S&P 500 is now 16.3, above the 15-year average of 14.9 (Strategas Research). This has been driven by both stocks moving higher and earnings estimates moving lower. As mentioned, Refinitiv shows the consensus for first quarter S&P 500 earnings to be -1.8%, with only slightly positive expectations for the subsequent two quarters. And while financial conditions have eased, contributing to multiple expansion so far this year; earnings may have to start doing more of the market’s heavy lifting—a not insignificant task given myriad headwinds facing earnings growth.

Real story may be somewhere in between

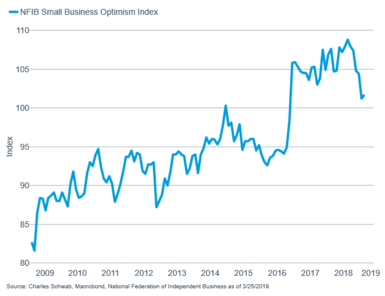

For those who lived through the Polar Vortex, spring is likely a welcome reprieve. Add in the government shutdown, and it made for a rough first quarter The Atlanta Fed’s GDPNow estimate has moved up to a still-weak 1.5% annualized growth, up from just 0.2% just a few weeks ago; and the government is still trying to catch up from the shutdown with respect to some economic data. As mentioned, some temporary factors appear to be fading, which could lead to a lift in the second quarter. Even the Fed acknowledged at the March FOMC meeting that “economic activity has slowed from its solid rate in the fourth quarter.” How much of a rebound we’ll get is in question; but we continue to believe trade holds the key. According to myriad reports, including from The Wall Street Journal, trade talks with China remain bogged down; although there were recently high- level talks again scheduled. Adding fuel to the concerns was President Trump’s recent proclamation the tariffs will remain in place for a “substantial period.” Reports from Politico also indicated that the Commerce Department has given the White House a report noting that tariffs on European autos would be justified. Finally, the third leg in the trade stool also looks shaky with Schwab’s own Washington expert, Mike Townsend, believing that passing the U.S. Mexico Canada Agreement (USMCA) through Congress is nowhere a done deal at this point. The outcome of each of these is impossible to know at this point, but it does keep business confidence under pressure and will likely result in ongoing delays to investments in capital and equipment (see the plunge in small business confidence below).

Corporate confidence dented—and could be at further risk

But all is not lost The Conference Board’s Leading Economic Index (LEI) rose 0.2% in February, the first increase in five months. In addition, the U.S. Citigroup Economic Surprise Index has been stabilizing over the past month, although it remains in negative territory.

Will modest improvement in economic news continue?

We remain concerned that investors may be overly complacent about both corporate earnings and economic growth; and that a pullback in the near-term is an increasing possibility.

Fed doubling down on dovishness

Many investors have pointed to the Fed as a reason to get more bullish on stocks. We concede its turn toward dovishness and putting rate hikes on hold have been positive market supports. The Fed’s so-called “dots plot” of economic and rate forecasts from its most recent meeting now show no rate hikes in 2019. Investors on the other hand, as per the fed funds futures market, believe the next move (this year) will be a rate cut. We lean more toward a cut than a hike, but we are concerned that investors may become complacent to the binary risks of a sharper slowdown in growth, or a flare up of inflation due to the tight labor market. We continue to believe any inflation flare up would be fairly benign, but with wage growth having picked up sharply (average hourly earnings are up 3.4% y/y as of February), and the rampant skills shortage, we don’t think an inflation scare should be taken off the table.

Could the worst already be over internationally?

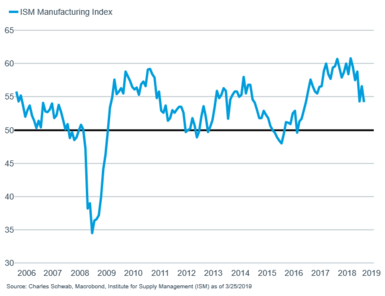

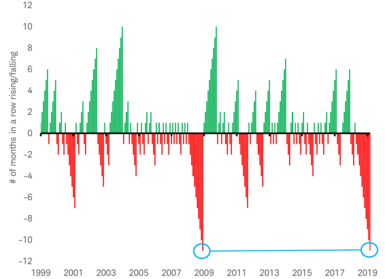

Growth concerns aren’t isolated to the United States; in fact, they appear to be exacerbated when looking past the border. Last week’s preliminary “flash” purchasing managers’ index (PMI) pointed to further economic weakness from many countries around the world. This makes it likely that the global manufacturing PMI will fall for the month of March to its lowest level in nearly three years when it is reported next week. March could be the 11th month in a row of declines for this indicator—a streak not seen since the last global recession in 2008.

Longest losing global PMI streak since Global Financial Crisis?

Source: Charles Schwab, Factset data as of 3/26/2019. Chart includes estimate for March 2019.

The weakening global economy is being highlighted by the inversion of the U.S. yield curve, with long-term bond yields continuing to fall. Over the past 50 years, U.S. yield curve inversions came about one year before each global recession. More significantly, they came close to the cyclical peak in international stocks, as measured by the MSCI EAFE Index.

U.S. yield curve inversions vs. peaks in MSCI EAFE

While the yield curves of individual countries often do a better job of predicting recessions in their domestic economies, the U.S. yield curve does a better job of measuring global economic conditions which can affect broad international stock markets. Why is the U.S. yield curve so much better at gauging global economic conditions? For one thing, the United States is the world’s largest economy and a major source of demand for global companies. In addition, the U.S. government bond market is the largest and most liquid in the world; which may mean it better reflects global conditions and is less susceptible to domestic influences than other countries’ bond markets.

Being prepared for volatile markets has been a key message as we pointed to the yield curve’s march toward inversion over the past few years; most notably in our annual Outlooks published at the end of 2017 and 2018. But now that it has inverted, what should you do? If you have prepared your portfolio, reevaluated your investment plan, confirmed your risk tolerance, and rebalanced your assets, there may be little you need to do. Remember, staying disciplined allows investors to ride out market downturns better than those investors who throw discipline to the wind.

Due largely to the drop in the fourth quarter of last year, international stocks fell 32% from their peak in January 2018 to their low in December 2018. That decline was very similar to the average 37% peak-to-trough decline during the six cyclical peaks over the past 50 years (referenced in the table above). It could suggest that the peak in international stocks came 14 months before the inversion—rather than 14 months after the inversion, as it did in 2007. Perhaps we should consider appending the table above with the following line:

The yield curve has done a remarkable job signaling peaks in international stocks over the past 50 years, in a variety of political and economic environments. However, there can be no guarantees it will always do just as well. It is possible that we haven’t seen the peak yet, meaning there could be significantly more gains to come before the overall cycle peaks—the market would have to recover 14% to make a new high. It would be welcome news if the worst of the decline for global stocks, historically associated with the yield curve inversion and slide in economic indicators like the global PMI, is already over. Of course, there is no way to be sure and both U.S. and international stocks could resume the declines seen last year. Either way, the message for investors is the same: remain prepared for volatile markets.

So what?

Brief dips in U.S. stocks have done little to dent investor confidence; and with an inverted yield curve, trade uncertainty continuing, economic growth slowing and earnings possibly declining in the first quarter, we believe a pullback is becoming increasingly likely. Investors should remain disciplined and diversified and continue to prepare for the inevitable end of this cycle—without needing to pinpoint the timing precisely.