The market has grown less anxious about an imminent wave of bond downgrades. That’s good, because overestimating the risk can lead to missed opportunities. But the risk hasn’t disappeared, making research as important as ever.

At the end of 2018, nearly $140 billion worth of BBB-rated bonds were trading as if they were already below investment grade, reflecting widespread concern about unsustainable corporate leverage. That’s the kind of thing bond investors find hard to ignore—with good reason. A wave of downgrades could lock in big losses for investment-grade strategies and spark a disruptive repricing in the high-yield market, a risk for high-income-oriented portfolios.

At the time, we said that a group of US investment-grade bonds worth a much smaller amount were at risk of becoming fallen angels, as formerly high-grade bonds are known. Our research suggests about $80 billion worth could tumble to high yield (Display 1), and we think the process could take years to play out.

The market has recently edged a bit closer to our point of view. Demand for BBB-rated bonds surged in the first quarter, with the sector delivering returns of nearly 6%. Why the change of heart? Probably because conditions have changed. Six months ago, the Federal Reserve expected to raise rates three times in 2019. Now, it says it won’t raise them this year at all. This may sustain US growth and ease pressure on corporate borrowers.

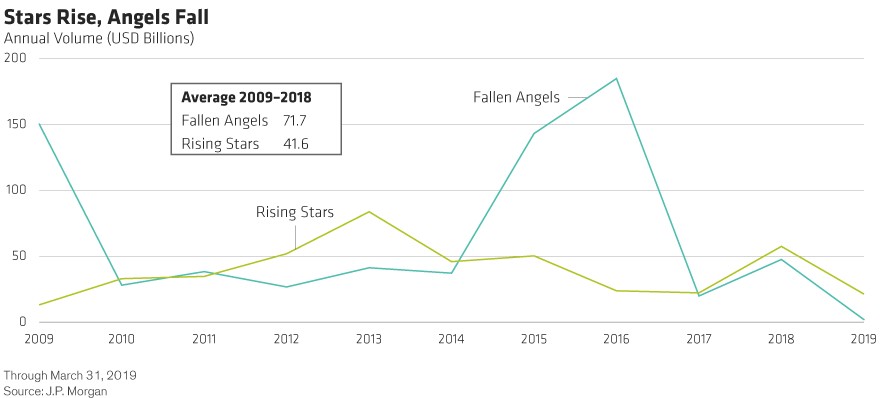

Don’t get us wrong: some of the companies still clinging to the bottom rung of the investment-grade ladder will become fallen angels this year. That’s not so unusual, though. A certain number of investment-grade bonds are downgraded to high yield every year—about $72 billion worth on average each year between 2009 and 2018 (Display 2).

Fallen-angel volume was high after the global financial crisis and following a plunge in oil prices in 2014 and 2015, though this did not overwhelm the high-yield market. Recently, there have been more rising stars—bonds that were upgraded from high-yield to investment-grade status—than fallen angels, a trend that has continued so far in 2019.

Even so, performance will depend on investors’ ability to distinguish between those bonds likely to fall and those that the market is erroneously pricing as high-yield credits. This requires an internal ratings system that draws on extensive research—both quantitative and fundamental—to separate the weak from the strong.

For Many Companies, Paying Down Debt Is Still an Option

It’s true that sharp increases in leverage at investment-grade companies over the past decade and challenges to firms’ business models have made many more vulnerable to downgrade.

But as we noted last year when downgrade fears were at a fever pitch, not all BBB-rated bonds are created equal. Sure, companies that responded to pressures in their industries by pursuing leveraged mergers and acquisitions—many food-and-beverage companies fit the bill—face significant fallen-angel risk today.

In many other sectors—energy, capital goods and basic industry, to name a few—firms still can clean up their balance sheets and pay down debt. GE, for example, is targeting aggressive debt paydown by selling off parts of its business. Other companies can prioritize debt reduction by reducing dividends and share buybacks. This flexibility should limit the number of bonds facing downgrades over the next few years.

Don’t Skimp on Credit Research

The market doesn’t always make these distinctions, and that presents opportunities for investors who do. Using our own internal ratings, we can isolate those investment-grade bonds that come with high-yield risk but investment-grade prices. The securities that fall into this category are the ones we consider most vulnerable to a downgrade.

On the other hand, bonds with strong internal ratings that the market is pricing as “junk” represent attractive opportunities with the potential to boost overall return.

This is important for all types of investors to know. For managers who are prohibited from owning high-yield bonds, avoiding the riskiest BBBs in today’s market should be a top priority. Since these investors must sell any high-yield credits, they’ll be better off unloading the vulnerable securities before the rating agencies act.

For investors who can hold high-yield debt, owning some angels after they’ve fallen may make sense. This is because fallen angels tend to enter the high-yield universe undervalued relative to their credit fundamentals and often end up outperforming original-issue high-yield bonds.

Of course, no investor should expect to be right all the time. Fortunately, there are other ways to hedge risk. For instance, investors may want to focus on shorter-maturity bonds, which will be more likely than longer-dated ones to outperform should they fall to high-yield status.

We expect concern about downgrades to wax and wane all year. It’s important not to overreact to swings in sentiment and the market. Increasing exposure to all BBB-rated bonds because they’re cheap by historical standards is just as risky as avoiding the market entirely for fear of downgrades. In our view, careful analysis is essential for uncovering value and raising overall return potential, no matter what your return objective or fixed-income strategy.

Matthew Sheridan is Portfolio Manager—Global Multi-Sector, Matthew Minnetian is Director of Investment-Grade Credit, and Gershon Distenfeld is Co-Head of Fixed Income and Director of Credit at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein