The Case of the Missing Inflation…and What the Fed’s Doing About It

US inflation has been running low for some time, and key members of the Federal Reserve Open Market Committee (FOMC) are pointing a finger at the traditional policy framework. So rate hikes are on hold for the time being—and monetary policy is under the microscope.

Since the beginning of this year, bond markets have dramatically adjusted their expectations for US Federal Reserve interest-rate hikes. The market is no longer pricing in further increases this year, or in 2020, for that matter. We don’t expect further rate hikes either, but our rationale is different from popular wisdom.

Inflation Has Gone Missing

As we see it, the Fed didn’t stop hiking interest rates because there’s a growth problem—it stopped because there’s an inflation problem. Simply put, inflation has gone missing, and the Fed is worried about it. That concern led to a freeze on rate hikes—even though the US economic growth outlook remains solid.

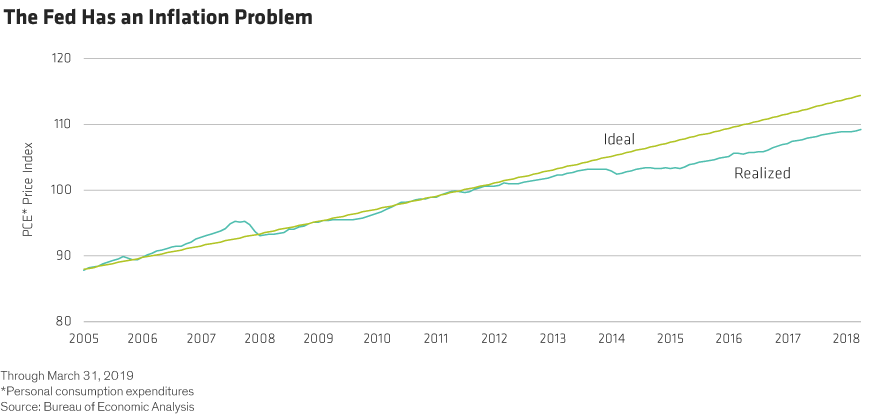

The Fed’s inflation target is 2.0% year over year, as measured by the personal consumption expenditure deflator index. Based on that data series, inflation has averaged less than 1.5% per year over the course of this economic cycle. As a result, current price levels are almost 6% lower than they would have been if the Fed had achieved its inflation target (Display).

That’s a lot of missing inflation!

Because of this inflation shortfall, inflation expectations are about 50 basis points lower than they were in earlier economic cycles. Inflation expectations can be self-fulfilling: businesses tend to set prices based on where they think inflation is headed. So lower inflation expectations today could mean lower actual inflation tomorrow.

That’s a problem for the Fed. It may seem counterintuitive to some, but low inflation could end up being a bigger headache than high inflation. If deflation sets in, it can be hard to break free of—as the Japanese have discovered over the past couple of decades.

Setting Sights on a New Inflation Target

With inflation running persistently below target, some FOMC members are worried that inflation could get stuck at too low a level. A newly formed FOMC group is looking at changing the framework for monetary policy, and this has already started to shape the way the committee discusses policy.

In our view, the Fed is likely to shift to an “average” inflation target of 2.0% over the course of a business cycle. Since we know inflation will be under 2.0% when times are bad, the Fed will need to keep inflation above 2.0% in good times. Otherwise, the math doesn’t work.