Emerging-market (EM) bonds got off to a strong start after a difficult 2018. Are more gains possible? We think so, and volatility sparked by increased trade tension may provide a buying opportunity for selective investors.

Last year was a tough one for emerging-market debt (EMD), which sold off broadly in an environment of rising interest rates, a strong US dollar and a global drift toward tariffs and trade protectionism.

Since then, some of the key risks that weighed on the market in 2018 have faded. The US Federal Reserve signaled that it wouldn’t hike interest rates again this year or next. And economic data indicated that China’s economy got off to a solid start in 2019 as the government ramped up stimulus support, easing fears of a sharper slowdown in the world’s second-largest economy. As a result, all EMD sectors posted gains in the first quarter, led by a nearly 7% return for dollar-denominated sovereign bonds.

But volatility returned with the recent escalation in the US-China trade war, and it’s likely to persist in the months ahead. We still think the two sides will reach a deal, but the risk of a protracted negotiation has gone up.

The good news is that there is still a lot to like in the EMD universe today, and investors may be able to take advantage of higher volatility to add EMD exposure. Investors who fear they missed the first-quarter rally may be especially well-positioned to increase exposure to attractively-priced assets.

Fundamentally Strong: Why the EM Growth Outlook Is Bright

Despite their rough ride in 2018, EM countries are still the world’s most powerful growth engine. The growth gap between EM and developed-market (DM) countries is widening. Portfolio flows into EM countries generally increase when the growth gap widens, which we expect it to do provided the US and euro area economies continue to slow to trend without contracting.

What’s more, EM countries are broadly less dependent on foreign investors for short-term financing relative to history. This makes them less vulnerable to sudden outflows. Outside of a few outlier countries, emerging markets have reduced current account deficits. That means many countries can cover a greater share of their deficits with foreign direct investment—a steadier source of financing because it tends to be longer term in nature.

At the same time, inflation across most of the EM world is low and expected to get lower. This gives central banks room to cut rates and stimulate growth. Many were forced to tighten policy last year to support their currencies and slow outflows.

Corporate fundamentals are strong, too. Despite recent market turmoil and sharp declines in many local currencies, default rates have been low. Display 1 shows the default rate among outstanding bonds across the emerging world, with last year’s rate falling to 1.6%. Selectivity is still important, as J.P. Morgan expects defaults to rise to 3% this year. But that’s still below the historical average. The default rate for the JP Morgan Emerging Markets Corporate Bond Index, which includes a smaller number of bonds, was even lower last year, at 1.2%, and is expected to rise to 1.9% in 2019.

Missed the EMD Rally? Don’t Fret.

Valuations remain broadly attractive in select parts of the market, and may get even more so if worries about trade depress prices in the months ahead. This means there are still opportunities for investors who have so far stayed on the sidelines in 2019.

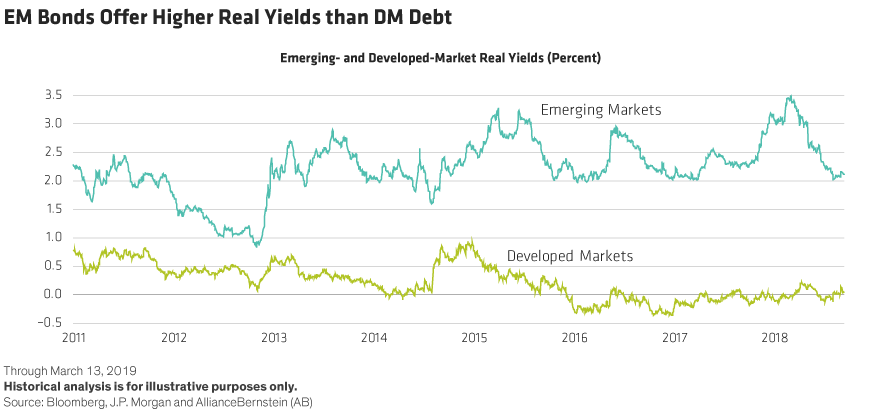

As Display 2 illustrates, real, or inflation-adjusted, yields on EM local-currency bonds are still significantly higher than those on DM ones, where the aggregate yield is stuck around 0%.

Meanwhile, investors can earn substantially higher yields on dollar-denominated EM investment-grade bonds—both sovereign and corporate—than they can on US debt of comparable credit quality. And anyone with high income needs should note that EM high-yield sovereign bonds have rarely traded at a higher premium to US high-yield corporate bonds.

Many EM currencies are still attractively priced, too. And they could benefit if the US dollar, which has been overvalued on a long-term basis, starts to weaken now that the Fed has said it won’t raise rates again this year.

Finally, the supply/demand dynamics still favor investors. Net issuance of EM sovereign and corporate debt has been light this year, while demand from investors eager to get in on the EM rally has increased. That is likely to be supportive of asset price performance.

An Active Approach Is Essential

Of course, with assets having come so far so fast this year, finding significant alpha opportunities means investors will have to be selective. There’s still variation in macroeconomic stability, governance and fiscal policy among countries.

For example, we worry about Mexico’s ability to balance its dual aims of maintaining fiscal conservatism and increasing social spending programs. This is a concern because PEMEX, the state-owned oil company, suffers from weak fundamentals and will likely require government support.

We’re more optimistic about Brazil, where a new government is pushing an ambitious agenda of privatization and pension reform and is trying to reduce bloated public-sector debt. But political infighting illustrates how challenging it will be to make these plans a reality. While we expect Congress to pass some reforms, they may get watered down.

Earlier this year, we thought investors in Argentina were too complacent about political risk. Now we think the recent sharp widening in spreads on dollar-denominated bonds has been exaggerated, creating opportunities for investors. While economic data has disappointed so far this year, we still expect President Mauricio Macri or another centrist candidate to win the presidential election this fall, an outcome that would keep market-friendly policies and a major IMF financing deal in place.

In Turkey, last year’s stark currency depreciation helped turn a current account deficit into a surplus. But there are still concerns about the central bank’s commitment to tackling inflation and the government’s vague economic plan. A recent decision to cancel the results of a local election in Istanbul have added to the uncertainty. We think the authorities still have work to do to regain the market’s confidence.

Other potential hurdles for investors this year include a full calendar of important national elections with the potential to move asset prices (India, South Africa, Argentina) and geopolitical risk, including the possibility of additional sanctions on Venezuela and Russia.

The bottom line: investors must do their homework, even when it comes to countries with solid fundamentals and the right policy priorities. But the global macroeconomic conditions—decent growth, accommodative monetary policies—are good for EMD, and the a renewed bout of trade-induced volatility should provide opportunities for discerning investors to add risk at attractive prices.

© AllianceBernstein L.P.

Shamaila Khan is Director of Emerging-Market Debt at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein

.png?uuid=232472e8-75c0-11e9-be41-8b1fba25cf73)