U.S. stocks suffered a 7-10% pullback throughout May as trade tensions and growth concerns heated up. The selling was disconcerting and bouts of weakness could persist, but potential opportunities may also emerge.

Warning signs are increasingly flashing for economic growth, while recession probability models have been moving higher; but for now we believe the bar remains relatively high for Fed rate cuts this year—although futures have priced in a 80% likelihood by July.

Elevated consumer confidence in the world’s economic leaders may not be painting an accurate economic picture.

“Though patience be a tired mare, yet she will plod.” ― William Shakespeare

Danger rising, potential opportunities emerging?

May saw equities pull back between 7-10% as trade tensions and growth concerns ratcheted up. After a solid rally since the early-June lows, the question now is: Is there more weakness to come?

We never try to time every near-term peak or trough in stocks; but we are concerned some of the issues which have rattled the market could get worse. First, the trade dispute with China could escalate even further as the United States is looking at imposing tariffs on the remaining ~$325 billion in Chinese goods that U.S. companies import. Additionally, trade talks with Europe have deteriorated recently and the threat of U.S. tariffs on all Mexican imports were dual escalations in the global trade battle. Due to tariffs’ growing impact, as well as weak global growth, S&P 500 earnings estimates for the second quarter have been in retreat—Refinitiv now shows a negative year-over-year earnings expectation. In addition, a historically fairly reliable predictor of recessions has flashed yet another warning; with the yield curve inverting again (well-outlasting in duration the brief inversion in March). This has fed into the Atlanta Fed’s GDPNow estimate for second quarter growth, which has moved down to a meager 1.5%; while the NY Fed’s recession probability model is up to 30%, the highest since the last recession.

Stocks have fallen, before staging a recent rebound

And volatility has trended higher

As the yield curve has inverted further

Although the story is relatively grim, we never suggest investors should head for the exits. May’s selling pressure helped relieve overly optimistic investor sentiment conditions that had accompanied the late-April market highs, helping set up the opportunity for the bounce since early June (for more on investor sentiment read Liz Ann’s The Age of Worry: Investor Sentiment Takes a Hit article). There may be further chipping away at optimism to set up for a more sustainable move upward; especially if the latest rally leads investors to do a sentiment about face. What else could be catalysts for a durable rebound? We’ve already seen instances of perceptions about trade turning on the proverbial dime (or tweet); and we could certainly see that again. An upside surprise on trade could make for a more sustainable rebound. In addition, it’s important to remember that the stock market is a forward-looking mechanism, so much of this quarter’s earnings and economic weakness may already be reflected in prices. We continue to think that risks are roughly balanced at the current time and that investors should continue to stay near their long-term equity allocations, using strength to pare back holdings if necessary. Within U.S. equities, we continue to favor large cap stocks at the expense of small cap stocks due to the latter’s weaker earnings outlook and significantly higher debt levels.

State of the economy

As noted, a weaker second quarter appears to be reflected in stocks, but what does the economic data tell us about the potential for future quarters? On the surface the 3.1% growth rate for real gross domestic product (GDP) in the first quarter looked healthy, but it was biased up by inventories and net trade, both of which appear to be reversing in the second quarter. Absent a significant cooling of trade tensions, economic risk now seems tilted to the downside. Manufacturing surveys have suffered, as a much weaker Markit PMI reading was followed by a softer Institute of Supply Management (ISM) Manufacturing Index. To some degree, it has filtered through to the service side as well, with weakness seen in Markit’s services index (although the ISM non-manufacturing reading did move slightly higher, bucking the trend). For now, all of the above remain in territory depicting continuing economic expansion, but the general deterioration bears close watching.

Manufacturing surveys weakening

And service indexes are recently split after both trending lower

Adding to the aforementioned weakness, the recent downturn in commodity prices such as copper also speaks to the weakening in the global economy.

Copper indicating weak global growth

But the glass isn’t all empty. Consumer confidence surprisingly rebounded in May reading (although it may not reflect the latest escalation in the trade war and attendant stock market pullback), and initial jobless claims remain historically low after a brief period of a rising trend.

Forward-looking labor indicator looks solid

However, more labor market news was out on Friday, although it is of the lagging variety, with the Bureau of Labor Statistics reporting that a disappointing 75,000 non-farm payroll jobs were created in May, although the unemployment rate remained historically low at 3.6%. The report was even a bit weaker than the headlines as revisions subtracted a total of 75,000 jobs from the prior two months. Employment gains have downshifted in 2019, as you would expect in the latter stages of a business cycle and as the number of available workers dwindle. Job gains averaged 223,000 a month in 2018 and has moved down to a still-solid 164,000 thus far in 2019. Despite the tightness of the labor market, the same report showed that wage gains remained muted, moving down a tick to a 3.1% gain y/y—a bit better than the 3.0% average seen in 2018, but not likely enough to influence the Fed to become concerned about inflation flaring up—yet.

Fed remains on hold

The mixed economic picture has kept the Federal Reserve in a holding pattern since January; although Fed Chair Jerome Powell sounded a dovish tone in a recent speech, noting that the Fed is monitoring the escalation in trade tensions and will act “as appropriate” to sustain the economic expansion. The market is now pricing in close to a 90% chance of two rate cuts by the end of the year, the Fed has not corroborated the market’s extremely dovish view in its recent commentary. At some point the market or the Fed will be forced to adjust their respective views; with the process of convergence possibly adding to volatility in the stock market.

Too confident?

The economies of the United States, European Union, and Japan are the first, second and fourth largest economies in the world, respectively according to the International Monetary Fund (IMF). These economies are driven primarily by consumer spending, and together they account for more than half of the world’s economy. High levels of consumer confidence in these countries might make it seem as if the global economy is resilient to a downturn, but history shows just the opposite.

As you can see in the chart below, consumer confidence in the United States and Europe may have already peaked for this cycle, at a level similar to that which preceded past global recessions of 1990-91, 2001, and 2008-09.

U.S. and European consumer confidence at levels preceding past recessions

Source: Charles Schwab, Bloomberg data as of 6/5/2019.

Peaks in consumer confidence occurred in the United States and Europe in 1989-90, 1999-00, and 2007, just ahead of prior global recessions. The most recent slump in Europe could reverse, with another surge in confidence to an even higher peak than the current cycle peak of 2018; but, it is a worrisome sign for the global economy that the peak was near or above the levels where prior cycle peaks occurred.

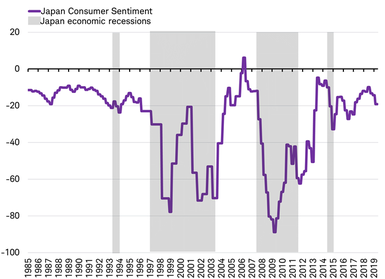

Japan is also showing signs that consumer confidence may be past its peak for this cycle. Japan’s consumer confidence seems to be retreating from its recent peak of -10; a level that preceded past recessions in Japan, as you can see in the chart below.

Japan’s consumer confidence past the peak for this cycle?

Source: Charles Schwab, Bloomberg data as of 6/5/2019.

Given the aforementioned greater bias toward consumer goods of any subsequent round(s) of tariffs, this could easily and quickly weigh on consumer confidence. In economies driven mostly by consumer spending, high consumer confidence may seem like a positive; but, confidence that is low and rising tends to be more consistent with a brighter growth outlook than when it is high and starting to fade. Contrary to being a sign of resilience to the tariffs, consumer confidence may now signal a risk to the global economic cycle.

So what?

We won’t speculate about the final outcome of ongoing trade tensions, but we are growing more concerned that the hit to business confidence will increasingly filter through to consumer confidence and hard economic data. A more positive outcome could elongate the runway between now and the next recession. In the meantime, we continue to recommend that investors maintain a relatively neutral stance consistent with long-term asset allocations, using inevitable gyrations to rebalance as needed.