The 11-year equity bull market is certainly getting long in the tooth, but several important indicators suggest we may not be at the end yet.

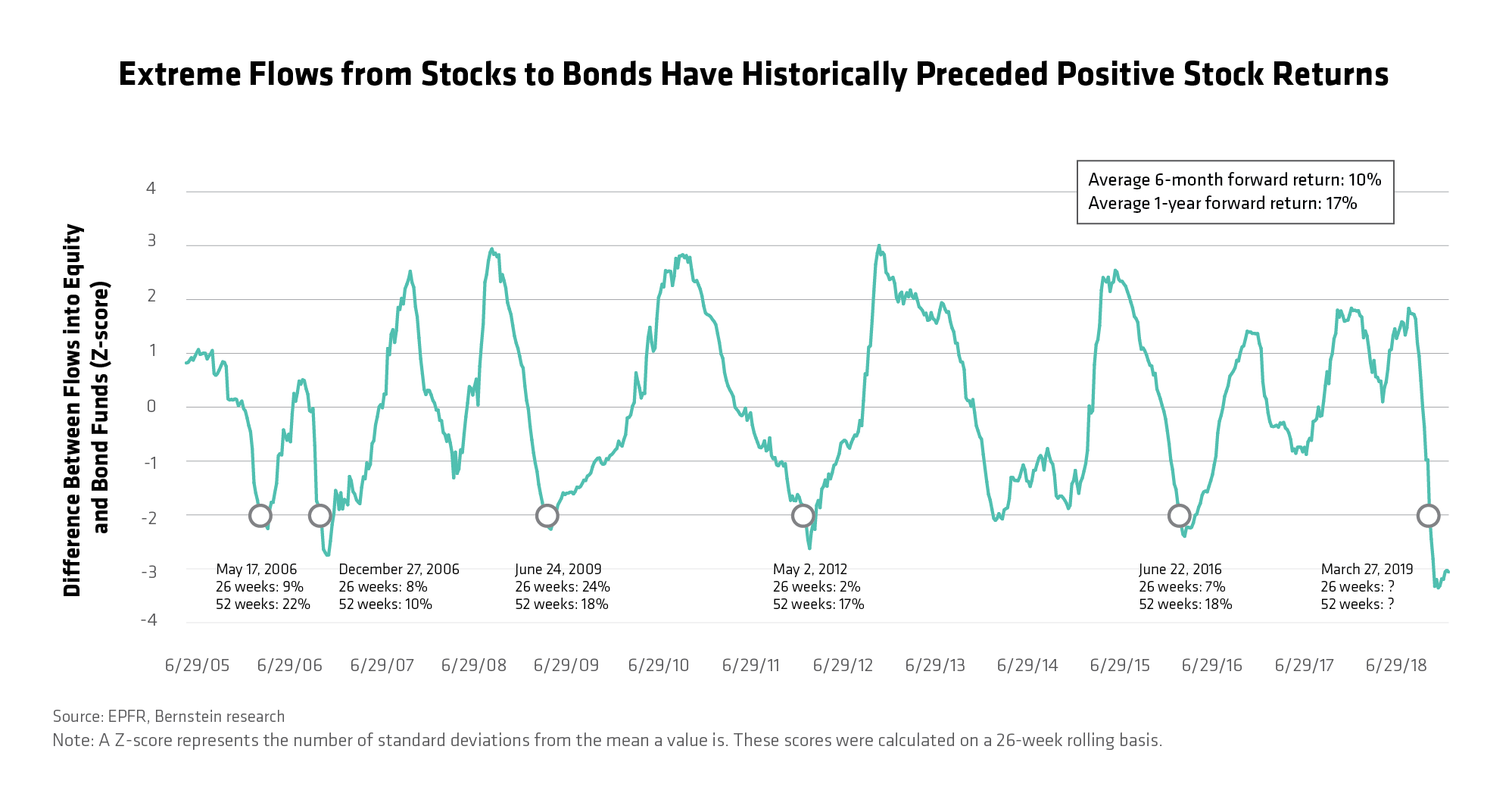

First, investors are selling stocks and buying bonds at extreme levels. The difference between inflows to global stock and bond funds is three standard deviations lower than normal, the lowest point since the data series began 15 years ago.

Historically, markets have experienced positive equity returns six months and one year after similarly wide divergences—specifically, after the difference between stock and bond inflows reached two standard deviations lower than normal. It’s possible that stocks became “oversold” at these times, and that investors running for the exits lowered the market’s collective expectations, setting a relatively low bar for a comeback.

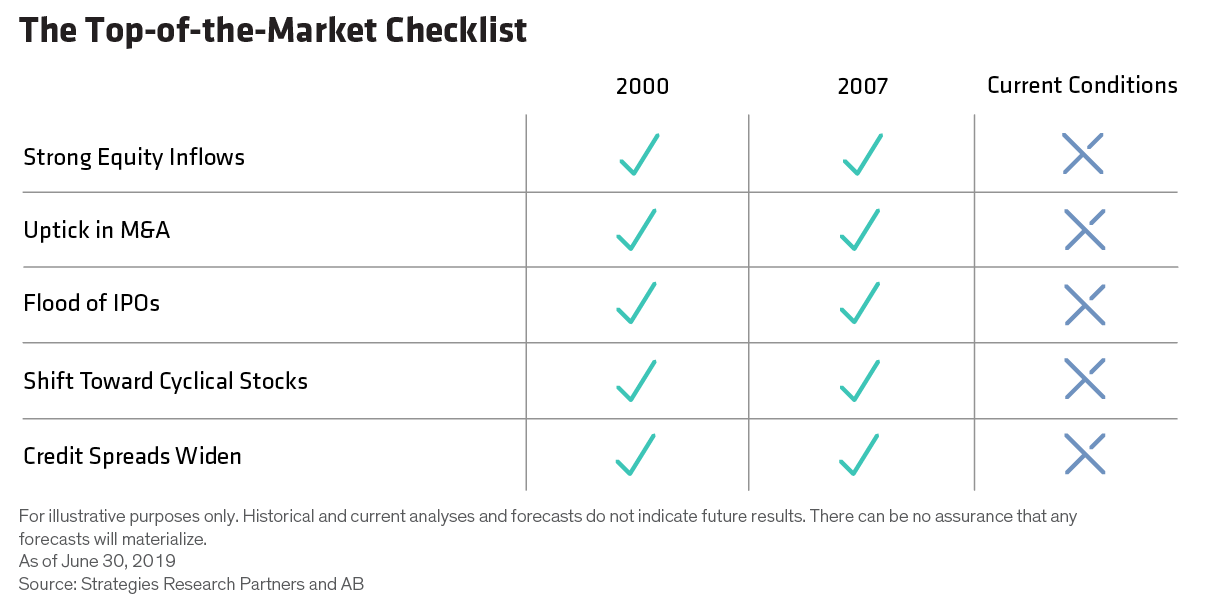

Asset-class flows aren’t the only sign the bull market isn’t ready to top out just yet. Five market indicators that were flashing red at the top of the bull markets of 2000 and 2007 are not doing so now.

Of course, equities face plenty of challenges. Policy risks, including trade wars and Brexit, as well as macroeconomic risks make for a complex environment. Volatility is likely to stay elevated as markets digest these risks, even as central bank pledges to maintain loose monetary policy should support stocks.

The bottom line? It may be the wrong time to join the herd and start selling out of equities altogether, but it is important to remember that the cycle is aging and eventually will turn. In these conditions, we think it’s especially important to focus on high-quality companies with a track record for generating earnings growth and specific qualities that imply they can continue doing so. Investors should also consider flexible strategies that can both take advantage of the potential for additional broad-based stock-market gains while also defending against an eventual downturn.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein