Key Points

-

U.S. equities have trended higher, largely ignoring weakness in the manufacturing sector and cheering looser monetary policy, but the recent pullback could be a sign of things to come.

-

While manufacturing and business indicators have weakened, the consumer remains solid, bolstered by a strong labor market. After cutting rates, the Federal Reserve held its dovish stance; but vulnerabilities remain for investors, including a worsening trade situation.

-

The Japanese economic outlook is mixed, with monetary, fiscal and trade policies all intersecting.

“History is a vast early warning system.”

― Norman Cousins

Warning Signs

Investors have largely ignored mounting economic warning signs, pushing U.S. stocks steadily higher over the past two months (albeit with some minor bumps along the way). A perceived softening of trade tensions between the U.S. and China (prior to President Trump’s most recent tariff threat), along with a dovish Federal Reserve, has bolstered investor sentiment. We remain positive but are getting a bit concerned that markets have gone too far, too fast—with investor sentiment reaching extreme optimism levels, according to the Ned Davis Research Crowd Sentiment Poll. Additionally, the manufacturing sector—which is more sensitive to trade and tends to be a leading indicator of economic activity—has shown signs of weakness; yet, this hasn’t been reflected in investor behavior. Due to the increased likelihood of a decent-sized pullback in the near future in our view, as well as the newly-imposed 10% tariffs on $300 billion in Chinese goods scheduled to go into effect on September 1, we continue to suggest investors remain patient and diversified, with a bias toward large cap stocks and a defensive tilt regarding sector allocations (See Sector Views for more).

Brief slump or signal for the future?

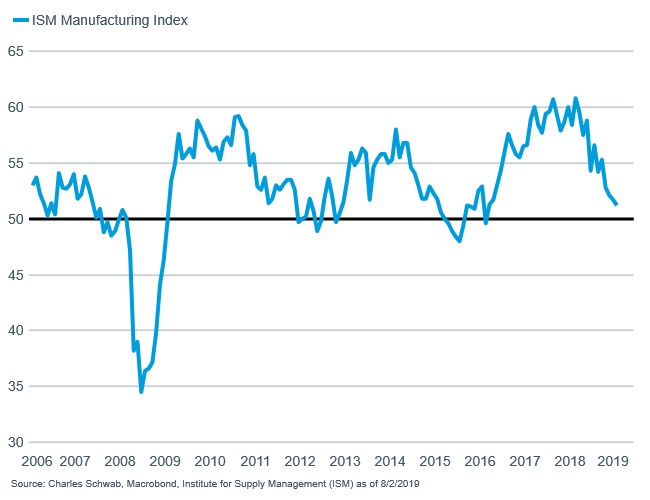

The aforementioned softening in manufacturing may start to negatively impact the services sector and broader economy. Markit’s Manufacturing Index fell to 50.4 in July, accompanied by the Institute for Supply Management (ISM) Manufacturing Index’s drop to 51.2.

Manufacturing weakening

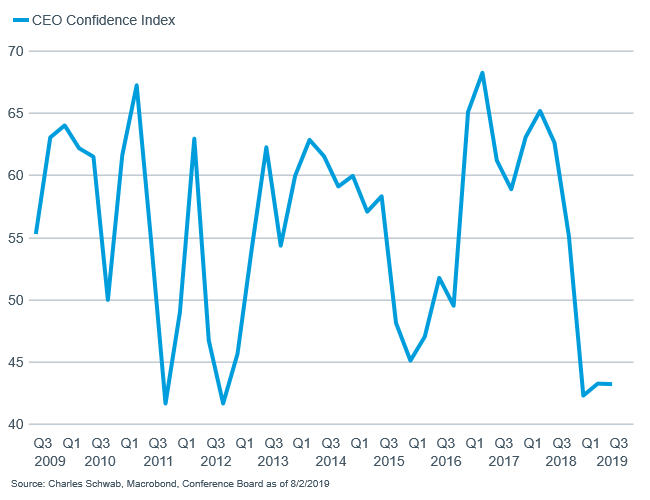

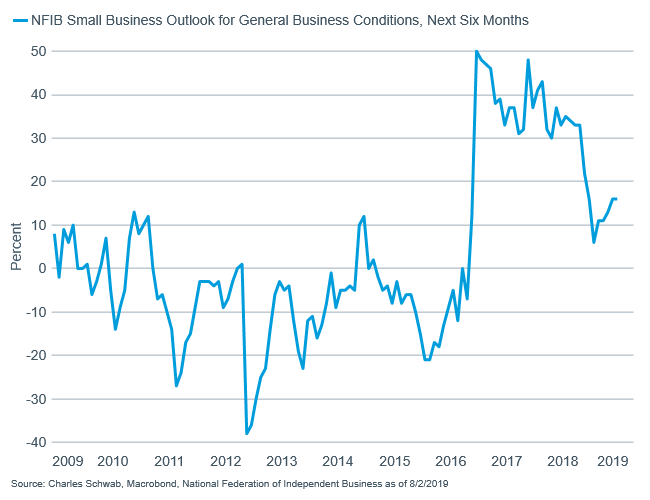

Unsurprisingly, both surveys indicated that trade was a significant contributor to the weakness in manufacturing activity; and we are concerned it may start to bleed through to other areas of the business world. Both the CEO and NFIB outlooks have struggled of late. According to Strategas Research Group, planned capital expenditures based on Fed regional surveys have declined sharply, which historically has led to a decline in actual capital spending.

Business confidence weakening

As is the outlook for small businesses

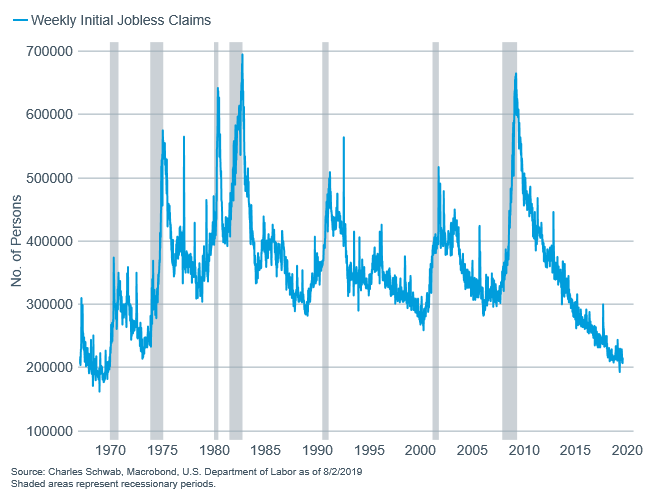

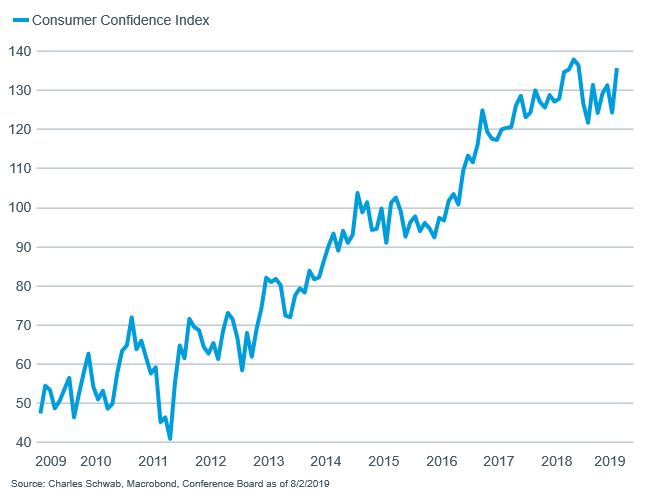

Thus far, the weakness seen in the business world hasn’t bled into consumer sentiment. Businesses have positively contributed to a strong labor market by continuing their solid hiring pace. Jobless claims remain near historic lows; and July’s labor report showed 164,000 jobs were added in July (although the previous two months were revised lower by 41,000 jobs), while the unemployment rate stayed at a low 3.7% and wage gains remained modest by posting a 3.2% y/y gain. Sustained strength in employment data has elevated consumer confidence, which should in turn help support the economy in the near-term.

The labor market remains healthy

And should continue to bolster consumer confidence

While it’s no reason to get overly excited, second quarter earnings season is nearing completion. As of now it appears we will avoid negative year-over-year earnings growth, as Refinitiv’s current estimate for the quarter is 2.5% growth. Commentary has been mixed, with many businesses expressing concern with regard to trade and remaining cautiously optimistic for the second half of the year.

Regarding trade tensions, they appear to be worsening, as President Trump introduced on Thursday another round of tariffs set to go into effect in September. Despite meetings between the United States and China this past week and another scheduled for September (which may now be in question), a comprehensive deal appears to be distant. Additionally, disputes with Europe and India, along with uncertainty regarding passage of the USMCA, will likely continue to be headwinds.

Fed reacts…but is it enough…and will it matter?

Trade uncertainty and slowing global growth both contributed to the Fed’s decision to cut rates; and easier policy in the future remains a possibility. Despite the easing—which the market was expecting—we are a bit concerned for two reasons. First, evidenced by the selloff during Jerome Powell’s press conference, investors may be disappointed if the Fed isn’t dovish “enough”. This could prove true due to continued strength in the labor market or a tick up in inflation. Second, we remain skeptical that trade should play a large role in rate policy decisions—especially given their already-low levels, as the “cure” to trade-related uncertainties doesn’t seem to be lower rates—at least to us. These two areas of concern lead to the possibility of choppiness in the second half of the year, as investor expectations and Fed policy converge.

Japan: beyond the VAT

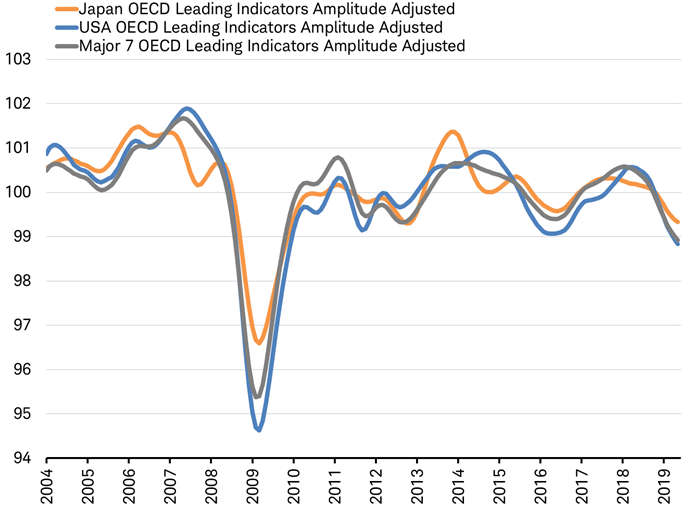

Across the globe, we can see another example of monetary policy failing to carry the entire weight of an economic outcome. Japan is the third largest economy in the world (following the U.S. and China) and has the brightest economic outlook of the major Group of 7 (G7) countries, according to leading indicators. Yet, its economy is the most likely to experience a recession this year. We will explain how these two seemingly opposing views actually make some sense.

Leading economic indicators for the world’s major economies are all headed lower, suggesting a lingering global slowdown. But, they are not all falling at the same rate. Japan has the highest composite leading indicator of all members of the G7 (the United States, Canada, France, Germany, Italy, Japan, United Kingdom) countries, including that of the United States (which is currently the weakest of the G7), as you can see in the chart below.

Japan has strongest leading economic indicator of the G7 countries

Source: Charles Schwab, Bloomberg data as of 7/29/2019.

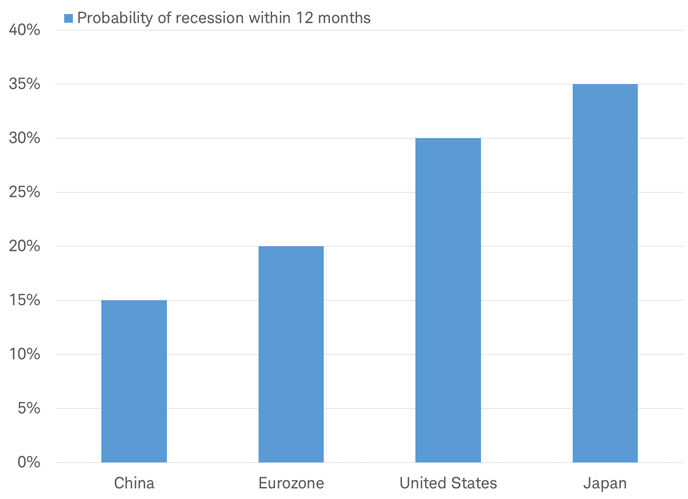

Japan’s economic outlook may be aided by the 2020 summer Olympics in Tokyo (helping to lift capital spending), an acceleration in bank loans, and the lowest level of corporate bankruptcies since 1990. Yet, the Bloomberg-tracked economists’ consensus currently pegs the probability of recession in the next 12 months at 35% for Japan—higher than China at 15%, Europe at 20%, and the United States at 30%.

Recession odds within next 12 months according to consensus of economists

Source: Charles Schwab, Bloomberg data as of 7/29/2019.

Why does Japan carry the highest odds? The increase in the sales tax, or the value-added tax (VAT), from 8% to 10% currently planned for October of this year could result in a short, technical recession. Ahead of the implementation of the tax, spending may be pulled forward and then stall. The last time the VAT was increased in 2014, GDP fell -1.8% (Bloomberg). This year’s planned tax hike is smaller and includes offsetting exemptions and subsidies. However, a one-quarter dip in GDP is more likely in Japan than in any of the other G7 nations this year.

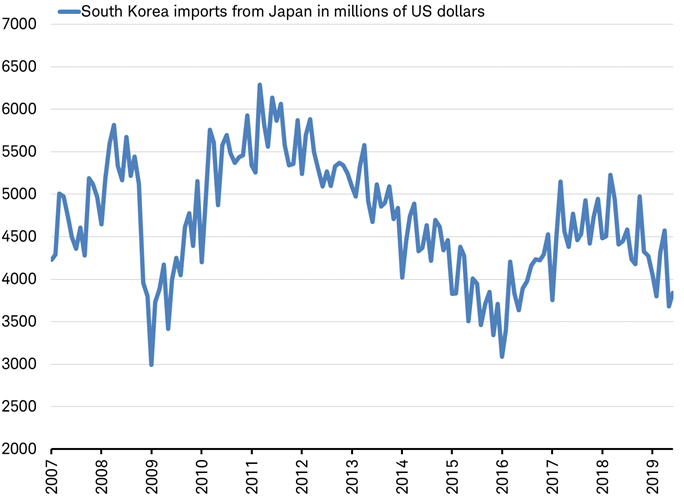

Another factor clouding the economic outlook is the brewing trade battle between Japan and South Korea. On July 1, Bloomberg reported that Japan removed chemicals critical to South Korea's technology industries from the expedited export list, which could subject them to delays of up to three months. In addition, as of last week, Japan imposed lengthy national security vetting for goods exported to South Korea, dropping the nation from its 27-nation “white list” of those that receive preferential treatment. Korean imports from Japan appear to be back at lows last seen in 2009 and 2016.

Korean imports from Japan sliding back toward lows

Source: Charles Schwab, Bloomberg data as of 7/29/2019.

Seeing the risks to domestic growth, the Bank of Japan appears set to follow the lead of the U.S. Federal Reserve and may step up action to bolster the economy. These risks include recognizing the pressure on Japan’s economy from soft global growth, trade uncertainty, a strong yen, the pending tax hike and geopolitical developments. Japanese government leaders may also stimulate the economy with an increase in the minimum wage.

Despite the heightened near-term risk of a short economic contraction for Japan, the outlook for a return to growth in 2020 appears brighter than in other countries—but isn’t assured. Equity markets tend to be a leading indicator and Japanese stocks, as measured by the MSCI Japan Index, have trailed all other G7 nations this year—except the United Kingdom, which is also facing a near-term economic risk in Brexit. Japanese stocks may stagnate until the impact of the tax hike is clearer and the focus of investors turns to new stimulus and a potential economic rebound.

So what?

Hope for looser monetary policy has boosted investor sentiment and pushed indexes to record highs. However, the manufacturing sector has weakened and threatens to impact the still-confident consumer; and could worsen if the next round of tariffs kicks in and the trade dispute with China worsens. We remain relatively cautious and suggest investors stay patient and diversified, as the potential for an even greater near-term pullback has grown.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. The policy analysis provided does not constitute and should not be interpreted as an endorsement of any political party.

The S&P 500 Composite Index is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

Markit Manufacturing Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index includes the major indicators of: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The CEO Confidence Survey is a monthly survey of 100 chief executive officers (CEOs) from a variety of industries in the U.S. economy. The survey is conducted, analyzed and reported by the Conference Board.

The NFIB Small Business Economic Trends is an index derived from 10 components, with 1986=100. The index is seasonally adjusted for variations within the year. Monthly surveys are derived from a large sample of respondents drawn from the membership files of the NFIB. The NFIB survey provides an early health check on small businesses, which are critical to the economy

The Consumer Confidence Index is a survey by the Conference Board that measures how optimistic or pessimistic consumers are with respect to the economy in the near future.

The Organization for Economic Cooperation and Development (OECD) is a unique forum where the governments of 34 democracies with market economies work with each other, as well as with more than 70 non-member economies to promote economic growth, prosperity, and sustainable development.

The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. With 318 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

©2019 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

More Factor-Based Investing Topics >