It’s been 20 years since a Chinese bank failed. But recent bailouts of three regional lenders have raised concerns about systemic problems in China’s financial sector. While risks have grown for China’s smaller banks, we believe that the Chinese banking system remains robust.

In May, Chinese financial regulators took control of regional lender Baoshang Bank because of serious credit risks. While personal and small business accounts were protected, some corporate and interbank customers suffered losses. This shocked investors who had formerly believed that the government effectively guaranteed all Chinese financial institutions. The takeover briefly sparked fears of a domino effect across other small banks.

In late July, the country’s largest bank, state-owned Industrial and Commercial Bank of China (ICBC), and two other state-owned “bad banks”* rescued another regional lender, the Bank of Jinzhou. And in August, a subsidiary of China’s sovereign wealth fund** took over a third troubled regional lender, Hengfeng Bank, which is owned by the same parent company as Baoshang Bank.

It sounds like China’s banking system is in dire straits. But is it?

Assessing the Breadth of Distress

In China’s diverse banking system, the risky lenders are found in the third- and fourth-tier banks. These comprise about 20% of total banking assets in China (Display 1).

For 20 of these low-tier banks, we have detected early risk indicators. These signals include failure to release data, deterioration in financial metrics, and ratios that denote higher risk and/or lower transparency. For instance, a telltale sign of hidden nonperforming loans (NPLs) is when overdue loans appear to grow faster than published NPLs. This divergence flagged problems at Baoshang Bank.

These 20 low-tier banks, with ¥3 trillion (US$426 billion) of assets, make up just 1.2% of China’s entire banking system. But beyond these 20 banks, many very small lenders are unlisted and do not disclose financial statements. These comprise 10% of the Chinese banking system, and they are an enigma. If we make a conservative assumption that half of these unlisted banks are in trouble, that would mean the percentage of troubled banks relative to total Chinese banking assets is in the mid-single digits. This is not a sign of broad-based banking distress.

Several Factors Help Stabilize the Banking System

We view the risks to China’s banking system as under control because of three stabilizing factors:

First, restructuring is under way. To minimize market impact, several distressed small banks in China have already been restructured and recapitalized behind the scenes. In fact, this process has been going on for the last five years, as NPLs in China have trended up. This shows that China can prevent contagion from pockets of regional instability.

Second, funding risk is limited to small banks. Large financial entities, which comprise the lion’s share of the Chinese banking system, face very little funding risk. For one thing, these banks rely very little on external funding, which minimizes vulnerability to capricious foreign flows. On the asset side, most of Chinese banks’ borrowers are either state-owned enterprises (SOEs) or local government financing vehicles (LGFVs) that the government continues to effectively underwrite. Otherwise, the banks have some exposure to households, which are only moderately leveraged. This is not a recipe for a broad-based asset quality shock

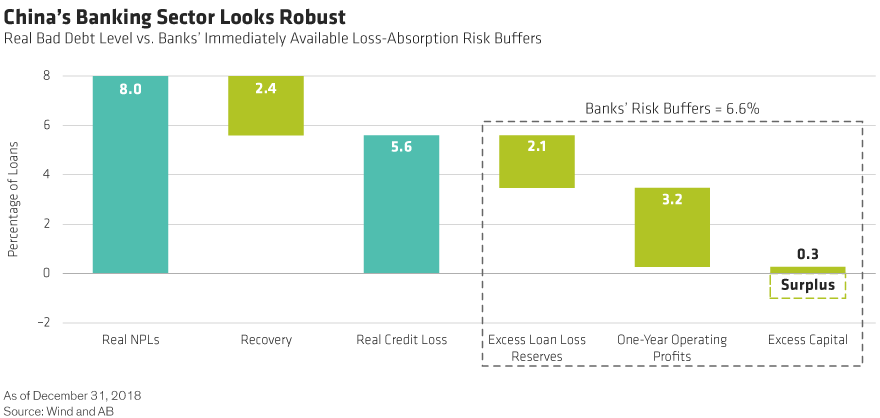

Third, the system can absorb bad debts. China’s reported NPL ratio is just 1.8%. But even if—as we believe—China’s true NPL ratio is more like 8%,† and even if all these loans become immediate losses, the banking system has available internal resources to absorb the hidden bad debts in full and still have surplus capital remaining (Display 2). That puts their reported capital ratio above the Basel III minimum requirement.

Concerns over Consolidation, Reforms and Funding

Some investors worry that the government will ask China’s big banks to perform national service by consolidating distressed small banks. But we believe that China will keep the core of its banking system—the first-tier, state-owned banks and second-tier, nationwide banks—clean. These tiers comprise 60% of the banking system.

Over the past 20 years, no state-owned or nationwide bank has ever recapitalized or consolidated a distressed small bank. However, as part of the latest bailout, ICBC will become a minority shareholder in Bank of Jinzhou, even though there are no obvious synergies between the two banks. If more such bailouts materialize, the cleanup of smaller, distressed banks could contaminate big banks’ balance sheets.

To complicate matters, necessary and desirable banking sector reform has the potential to disrupt the real economy. Compared to previous behind-the-scenes bailouts of smaller banks, the recent cases of Baoshang Bank and Jinzhou Bank mark a material increase in transparency into how China deals with distressed banks. We believe that China’s financial regulator, the China Banking and Insurance Regulatory Commission (CBIRC), desires this transparency. Its chairman, Guo Shuqing, is an advocate for banking reforms.

We welcome increasing transparency, because investors should understand that China’s banking system is not risk free. But we also acknowledge that this is a tough time to start the reform process, given recent downward pressure on the Chinese economy.

What else is a potential red flag? Small banks’ funding troubles.

Small banks have faced funding difficulties since the Baoshang Bank takeover. That’s been especially true for AA-rated banks, whose funding costs have surged compared to banks rated AAA.

Funding constraints will likely limit small-bank loans to private companies, either directly or through reduced financing for the non-bank financial institutions (NBFIs) that also lend to private enterprises through structured financial products.

What’s more, counterparty credit risk in the interbank market is inherently highly contagious. It could easily spill over into the real economy, which would also hurt the private sector. So far, we’ve seen capital raising by small banks dry up, and more defaults among private companies that rely on small banks and NBFIs for financing.

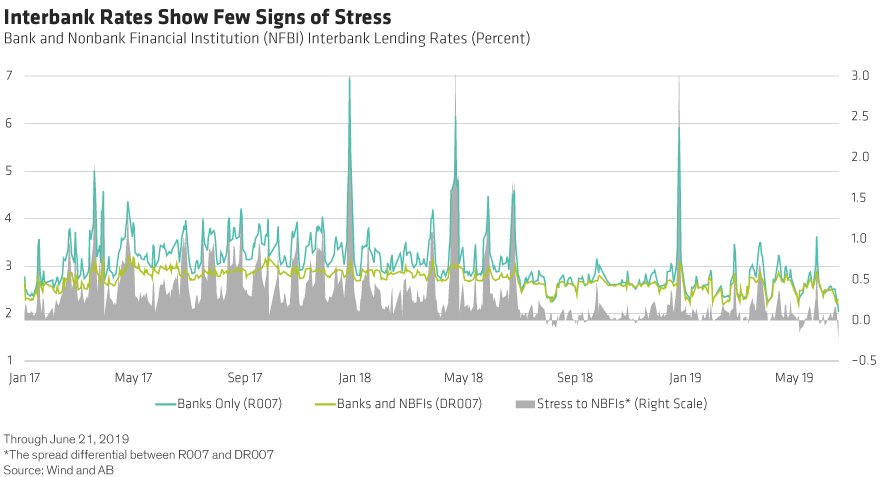

Thankfully, these risks are limited to small banks, NBFIs and private companies. There’s been little stress at either the core of the banking system or the core of the real economy, consisting of SOEs and LGFVs. Interbank rates also show no broad-based stress (Display 3).

Investment Takeaways

Providing the first- and second-tier banks aren’t compelled to consolidate smaller distressed banks, investors can remain comfortable with them, in our view. We don’t see problems at Baoshang Bank, Bank of Jinzhou or Hengfeng Bank posing a systemic risk to China’s banking system. With respect to top-tier banks’ subordinated debt, we expect dollar-denominated Additional Tier 1 ($AT1) bonds to outperform the $AT1s of third-tier banks. Despite the latter’s seemingly attractive yields, their downside risks are high.

The recent bank bailouts have raised some points of concern for the future. Investors need to stay vigilant as the potential impacts—particularly on private companies—unfold. If China permits additional and widespread defaults across the corporate sector, investors can expect an acceleration of financial sector reforms, which must lead the way for corporate reforms to be effective.

*China Cinda Asset Management and China Great Wall Asset Management, two of the four asset management companies established by the Ministry of Finance as “bad banks” and charged with buying the four state-owned banks’ NPLs.

**Central Huijin Investment is a subsidiary of the China Investment Corporation (CIC). CIC acts as the Chinese government’s shareholder in the country’s four biggest banks.

†To arrive at this 8% figure, we assume that all Chinese corporate lending with interest cover below one will ultimately default and become NPLs for banks.

Hua Cheng is a Research Analyst for Corporate Credit at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

More Fixed Income Topics >