For years, when institutional investors talked about the makeup of their emerging-market (EM) bond portfolios, they were talking about currency. Some bonds would be denominated in US dollars, others in the local currency of the issuing country—Mexican pesos, for example, or Chinese renminbi. But nearly all were sovereign bonds.

EM corporate bonds have historically been relegated to the periphery of fixed-income portfolios—if they’re represented at all. There was $113 billion benchmarked to J.P. Morgan’s EM corporate indices as of June 30, about one-sixth of the amount tied to its hard- and local-currency sovereign indices.

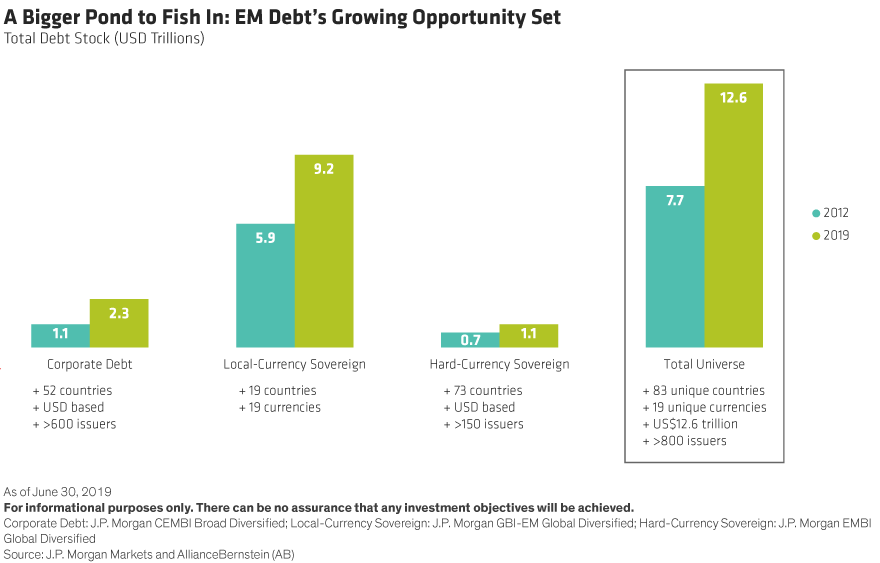

This under-allocation may have been understandable a decade ago when the outstanding debt stock was lower and less diversified. It isn’t anymore. The total EM corporate debt stock doubled between 2012 and 2018 to $2.3 trillion, about twice the amount of outstanding hard-currency EM sovereign debt. And the standard EM corporate benchmark, the J.P. Morgan CEMBI, encompasses bonds from more than 600 corporate issuers in 52 different countries (Display 1).

Widening the Opportunity Set

How investors add EM corporates to an existing fixed-income allocation will depend to some extent on their individual needs and comfort level. For institutional investors with dedicated EM mandates to hard- and local-currency sovereign bonds, it can be as easy as adding a stand-alone allocation to EM corporates.

An allocation to corporate debt provides diversification through exposure to more countries and to different parts of the credit cycle. It also gives investors access to a wider range of issuers in different sectors, often with a spread pickup over EM sovereign debt.

The Limits of a Sovereign-Only Allocation

Investors with discretionary mandates who entrust their allocation to a manager might benefit from a blended approach that adds corporates to the 50/50 mix of hard- and local-currency sovereign debt that most investors use today.

Again, diversification and downside protection are key. For example, a sharp rise in the US dollar—and a corresponding slide in EM currencies—hit local-currency sovereigns hard between 2013 and 2016 and wreaked havoc on traditional 50/50 blended strategies.

An allocation to hard-currency corporates would have diversified the currency risk in the 50/50 blend by giving investors exposure to companies with dollar-denominated export revenues. For these types of issuers, a rising dollar was good news because it boosted margins and cash flow.

In 2015, there was a 16.7% difference in annual returns for hard-currency corporates and local-currency sovereigns. Such disparities aren’t unusual.

High Quality—and Lower Volatility

Institutional investors with a lower risk tolerance might consider getting exposure to emerging-market debt (EMD) through an investment-grade only approach, split between sovereign and corporate debt. This is an increasingly popular strategy among insurance companies, pension funds and others who have traditionally focused on developed-market (DM) credit exposure.

Adding investment-grade EM corporates can give investors high quality with attractive yields. That’s because yields are higher than those on comparably rated debt from US companies—an important consideration at a time when low interest rates globally are making it harder than ever for investors to generate income.

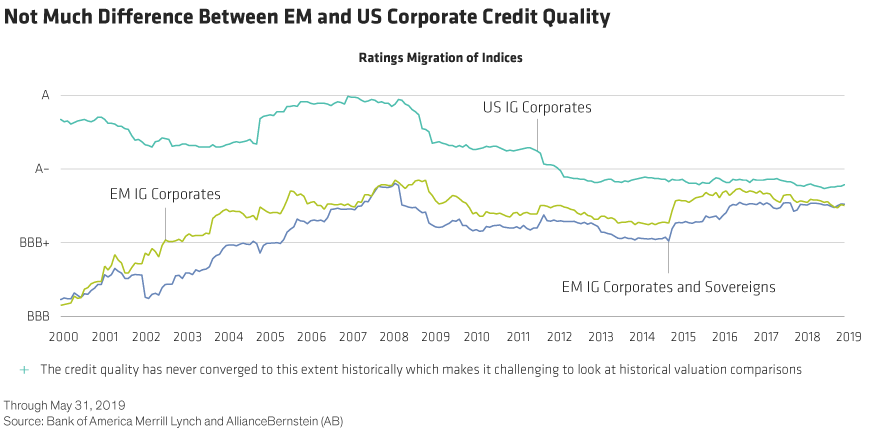

And in recent years, the average credit quality of investment-grade EM corporate debt has converged with that of US investment-grade bonds. In fact, there’s never been such a small gap between the average ratings of the two sectors (Display 2).

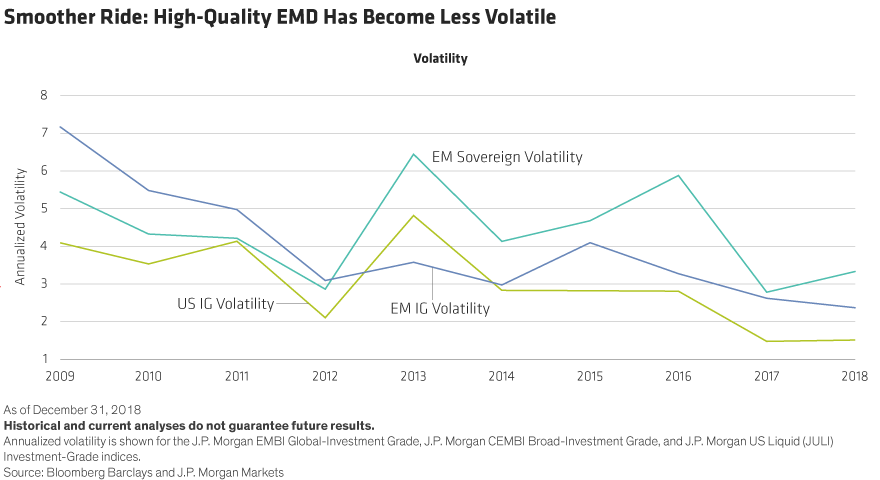

Volatility for the asset class has also declined sharply in recent years (Display 3).

What to Look for in an Asset Manager

EM corporate bonds aren’t entirely without risk, of course. While corporate governance, transparency and protections for creditors and shareholders have improved over the last decade, they still lag standards in developed economies. This is why it’s so important to choose the right manager for your EMD allocation.

First, let’s tackle the issue of expertise. Investors or their advisors should make sure that prospective managers have a long track record of investing in all types of EMD assets and a thorough understanding of the risks associated with emerging market corporates—economic, political, credit and industry-related.

Equally important is having a team of dedicated EM analysts who focus exclusively on EM issuers and collaborate with industry specialists, who can add important perspective when determining the relative value of a credit.

Prospective managers that cut corners in the research process probably aren’t seeing the whole picture of the credits they’re investing in.

As wealth continues to shift from developed to emerging economies, growth across the emerging world is likely to accelerate, boosting the bottom lines of an increasingly dynamic set of EM companies. There are complexities associated with analyzing EM corporate credit. But we think the size and diversification benefits that EM corporates offer make them a valuable addition to any bond portfolio.

Shamaila Khan is Director—Emerging Market Debt, and Elizabeth Bakarich is Portfolio Manager—Emerging Credit at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© AllianceBernstein L.P.

© AllianceBernstein

More Fixed Income Topics >