“We often confuse what we wish for with what is.” ― Neil Gaiman

Rally with conviction?

U.S. stocks have broken out of their recent trading range and moved closer to all-time highs as trade tensions have marginally subsided and the European Central Bank (ECB) has engaged in further easing. Despite this move, attitudes among investors have been less than enthusiastic as the Ned Davis Research Crowd Sentiment Poll (CSP) recently dipped into extreme pessimism territory and has rebounded only slightly into a zone that has historically been the best in terms of the S&P 500’s annualized performance (although past performance is no guarantee of future results). We remain cautious despite the recent move and still-supportive investor sentiment measures as trade news continues to dominate market behavior, and that is virtually impossible to predict. [See the details of our study in Chop, Chop, Chop: Stocks’ Choppy Behavior Around Trade News].

Attempting to trade around short-term news has proven to be a treacherous task; and though hope has emanated from anticipated trade talks in October and the delay of the October 1 tariffs (to October 15), a comprehensive deal remains elusive. Additionally, our colleague Mike Townsend has noted that, while the topic has garnered less attention than the trade dispute with China, the United States-Mexico-Canada Agreement (USMCA) still awaits Congressional approval. A failed ratification may increase trade tensions and sour investor attitudes. More broadly, sentiment around the world—particularly in response to Hong Kong’s abandonment of the “extradition bill” and another delay in Brexit—has also marginally improved. Yet, no major issues have been resolved and we believe there is heightened risk of volatility, keeping us in line with our theme of “be prepared.”

Mixed picture but weakness could be deepening

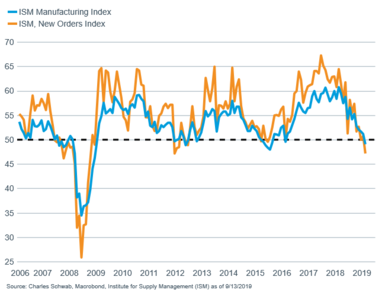

Google reported that search volume for “recession” recently hit highs last seen in 2009—when the U.S. was in a recession. Though recession chatter has persisted, overall economic data doesn’t show that one is imminent. Key, larger components of the economy—including services and the consumer—have held up well in light of trade uncertainty; while manufacturing has weakened further. The Institute for Supply Management’s (ISM) Manufacturing Index fell to 49.1 in August (below the 50 mark that separates expansion from contraction) and the forward-looking new orders component dropped even further to 47.2.

Manufacturing continues to weaken

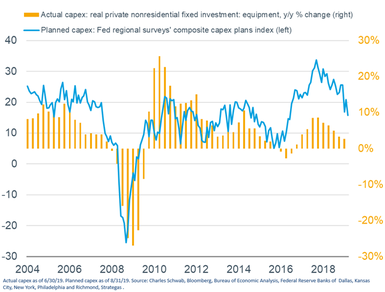

The survey highlighted firms’ continued concerns related to trade uncertainty. Unsurprisingly, apprehension over the trade dispute between the United States and China has brought down planned and actual capital expenditures. Absent a comprehensive deal and reigniting of corporate animal spirits, it is difficult to envision a near-term rebound in these measures.

Capex is also suffering

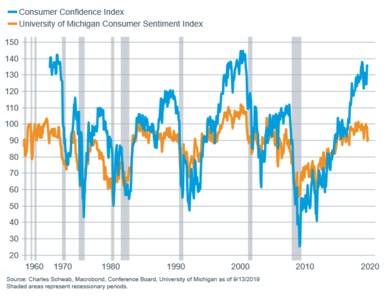

Manufacturing’s malaise has yet to spread to the larger services/consumer segments of the economy. Unlike manufacturing, services has strengthened of late, as the ISM Non-Manufacturing Index surprised to the upside in August, ticking up to 56.4. The labor market has also continued to show strength, as the four-week average for jobless claims recently moved down to 213k and the unemployment rate stayed at 3.7% in August (Department of Labor). Yet, last month’s addition of 130k jobs missed the 160k consensus; and revisions for the prior two months revealed a net loss of 20,000 jobs. Should payrolls start to weaken and jobless claims tick up, consumer confidence—as measured by The Conference Board—may start to weaken and catch down to The University of Michigan Consumer Sentiment Index. As you can see in the chart below, the two measures have maintained their divergence, with The Conference Board’s survey staying elevated. Important to note is the tendency for confidence to peak ahead of recessions, which is why cracks in the labor market and/or consumer are worth paying attention to.

Consumer indicators experience rare divergence

Monetary Policy Rethink?

With trade uncertainty high, inflation sitting below the Fed’s 2% target (according to the core PCE although core CPI posted a 2.4% y/y gain), and global interest rates remaining extremely low, investors continue to price in numerous rate cuts over the next six months. While we fully expect a 25bp cut at next week’s meeting, the outlook for the remainder of the year is clouded. Fed Chairman Jerome Powell has downplayed expectations of a rate-cutting cycle, calling the July cut a “mid-cycle adjustment;” and some Fed Presidents, such as Eric Rosengren, have pointed to gradual increases in wages and prices to justify holding rates steady. Doing so could disappoint investors and result in increased volatility. Regardless, we still have doubts that rate cuts are the elixir for what ails the economy. As other central banks have continued to engage in easier monetary policy, some global rates have fallen into negative territory— but the effectiveness of such moves are now being questioned with incoming ECB President Christine Largarde saying when asked about negative interest rates, that while the effect “continues to be positive, we need to be mindful about their potential side effects, and we have to take the concerns of people seriously.” We’ll have to wait to see how things actually develop, but a rethink of monetary policy would likely cause some consternation among investors as they adjust to a new potential new reality.

European Central Bank makes a big move

For now, the story remains the same in the Eurozone, as the ECB recently announced a major stimulus package—lowering rates and restarting quantitative easing (QE) bond purchases (Wall Street Journal). In turn, current President Mario Draghi has preserved some ammunition for his successor, Christine Lagarde, who may face a “no deal” Brexit or even a recession.

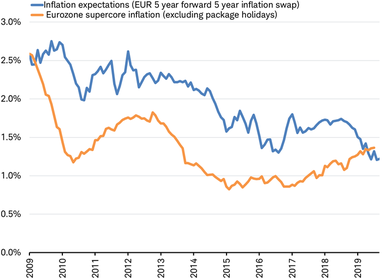

The ECB has sought to bolster inflation expectations, which have broken down amid weak global growth, trade uncertainty, a prolonged manufacturing downturn, and little upward movement in wages despite a tight labor market. Investors seem to have lost confidence that the pace of inflation will rise at all in the next five years. Market-based inflation expectations are now below the current rate of Eurozone “supercore” (inflation calculated by the ECB) inflation for the first time since the global financial crisis.

Inflation expectations fall below supercore inflation for first time in 10 years

Source: Charles Schwab, Bloomberg data as of 9/11/2019.

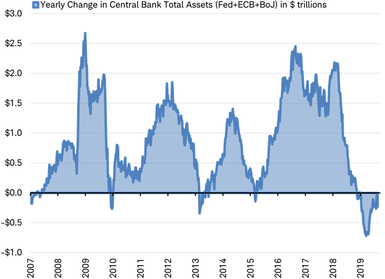

The main elements of the ECB package include a 10 bp cut in the policy rate and a restart of QE, leading to another rebound in the growth of central bank assets, as you can see in the chart below.

Ready for a rebound?

Fed = Federal Reserve, ECB = European Central Bank, BoJ = Bank of Japan. Source: Charles Schwab. Bloomberg data as of 9/11/2019.

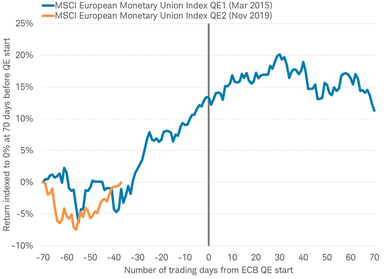

If the reintroduction of QE with changes allows the ECB to lower yields and support banks across the Eurozone, it may help lift stocks in Europe. European stocks rallied in the months leading up to the start of the ECB’s QE program in March 2015, but the below chart shows that the gains soon stalled after implementation.

Source: Charles Schwab, Factset data as of 9/11/2019. Past performance is no guarantee of future results.

Help for banks in the form of a tiered system for applying negative rates could likely be the key to a more durable rally than the one during the last QE program. Stocks stagnated soon after QE began in 2015—partially because of profit concerns in financials (representing 16% of the MSCI European Monetary Union Index)—as negative rates penalize banks for holding excess reserves. The ECB has proposed different levels, or tiers, to which negative rates are applied, which could reduce the adverse effects on bank income statements; while QE supports the bonds on the banks’ balance sheets.

The interest rate cut puts the policy rate at -0.50%. While there may still be room for another cut, the policy rate may be nearing the effective lower bound before depositors begin to opt in greater numbers for stashing cash in vaults (or mattresses) outside the financial system.

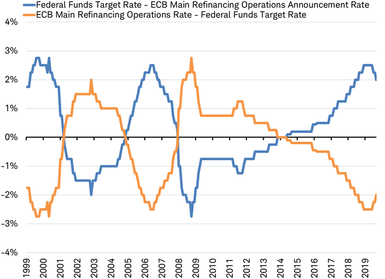

The gap between the Fed’s and ECB’s policy rates has started to close again, after widening out to the typical peak of around 250 bps. The pattern has oscillated between the central banks, trading places over the past 20 years, as you can see in the chart below. The current gap reached its maximum 250 bps spread at the start of this year, and may be reduced by as much as 100 bps this year. This narrowing gap, driven by the potential for more rate cuts by the Fed relative to the ECB, may limit the downside in the euro.

Policy rate gap beginning to close once again

Source: Charles Schwab, Bloomberg data as of 9/12/2019.

While the ECB’s policy moves may be effective in reviving inflation expectations, they would likely be amplified if paired with German fiscal stimulus. There has been more discussion in Germany toward suspending the “Black Zero” (or balanced budget) policy in the wake of budget surpluses, a slowing economy hit by the manufacturing downturn, and need for the ECB to have German bonds to buy for their QE program (Financial Times). However, it may take deeper economic pain for German policymakers to decide to act.

So what?

Stocks have climbed higher but we don’t recommend attempting to trade around short-term moves; rather, investors should remain disciplined and diversified, and use any volatility to rebalance as needed. The consumer continues to drive the economy, while weakness is mostly still concentrated in manufacturing. Yet, the potential for volatility remains, as a comprehensive trade deal is not in sight, tariffs on consumer goods are still set to kick in on December 15, and monetary policy’s ability to spur growth and inflation may be waning. We continue to favor large caps over small caps and are neutral to U.S. and global equities.