In today’s highly uncertain market environment, investors in US stocks are paying a premium for companies with high-dividend yields. But how much is too much—especially if interest rates stop declining? Stocks with resilient high-growth profiles deserve a closer look.

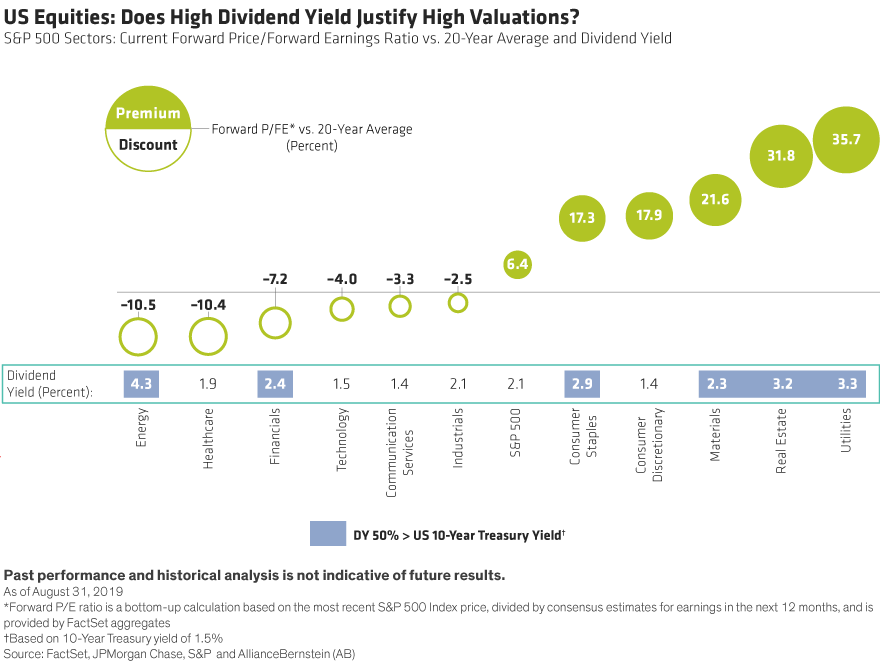

The hunt for yield continues to create market distortions. While the price/forward earnings (P/FE) ratio of the S&P 500 is close to its long-term average, sector valuations look imbalanced. Stocks that are sensitive to interest rates and yield are being pushed up as the 10-year US Treasury yield has dropped back down to 1.5%. At the end of August, most US sectors with dividend yields higher than the S&P 500 traded at a hefty premium to their long-term averages. In utilities and real estate, where investors can find juicy dividend yields above 3.2%, the sectors are at least 30% more expensive than the 20-year average of their P/FE ratios. Energy is the only outlier, as high-dividend yields have been buoyed by sharply falling shares amid a weak oil price.

On the other side of the spectrum, sectors like healthcare, technology and communication services trade at discounts to their long-term P/FE averages. Their dividend yields might not be as alluring, but are the fundamentals in these sectors really as weak as the discounts imply?