US state attorneys general recently stepped up their scrutiny of big tech’s business practices. With corporate mammoths likely to be in the crosshairs of regulators for some time, equity investors should consider looking beyond the titans for opportunities in the sector.

The battlefronts for big tech are multiplying: in addition to state attorney generals, the US Department of Justice, the House Judiciary Committee and the Federal Trade Commission are all pursuing inquiries. Corporate policies on competition, privacy and data sharing are under the microscope. Investors face more uncertainty if, beyond potential fines, new regulations threaten corporate business models or force the breakup of some companies. Restricting the ability of these companies to leverage user data across multiple platforms could deal a painful blow to their main business advantage.

Facing the FAANGover from Regulation

The answers to these concerns will come only at the end of a years-long process. Government agencies are like a black box for equity analysts, making it hard to get reliable information about where the process is headed. Regulatory uncertainty helps explain some of the recent volatility in big tech stocks and is likely to cloud the outlook for the foreseeable future.

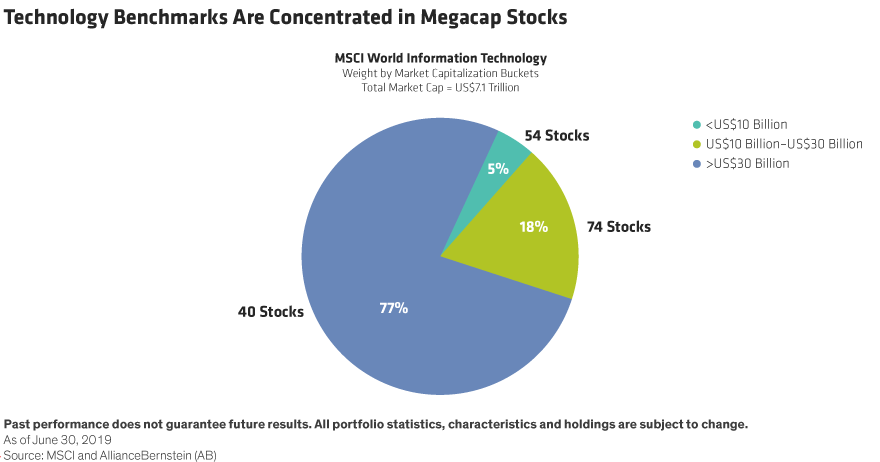

So, what to do? Given the uncertainty, we believe investors seeking to capitalize on the promise of technological growth should be wary of passive exchange-traded funds, whose baseline benchmark indices tend to be heavily weighted with tech giants and are backward-looking (Display).

Instead, investors need to take a proactive approach to the technology sector. Many investors have relied on Facebook, Amazon, Apple, Netflix and Google—the FAANGs—to capture technology-driven growth. But we believe that there are many compelling trends and companies in technology with potential to generate alpha, and with less regulatory risk than some of the larger players. Opportunities can be found not only in technology hubs like Silicon Valley, but around the world as well.

SMID-Caps: On the Cusp of Growth

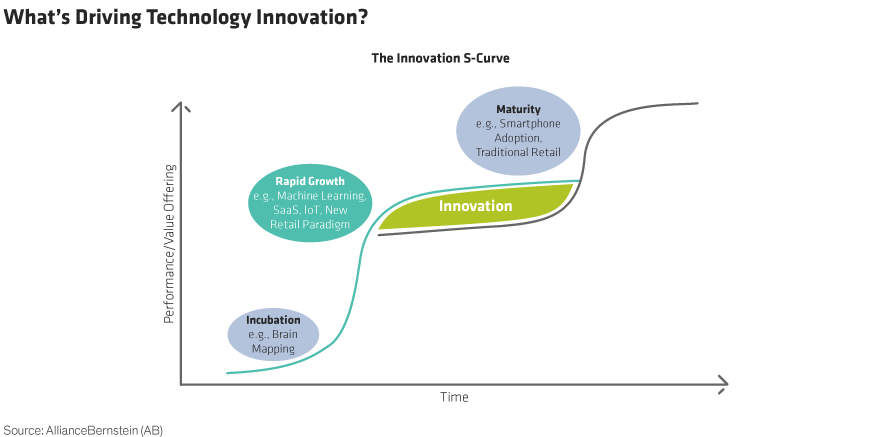

Beyond the FAANGs, small and mid-sized technology companies provide fertile ground for investors. Start-ups and venture capitalists refer to an initial public offering (IPO) as an “exit”—an opportunity to cash in on speculative seed investments. But in our view, an IPO is often just one milestone of a still-unfolding journey—an opportunity to raise capital to expand and realize growth potential. In our view, there’s still plenty of alpha to reap by identifying small- and mid-cap technology companies on the cusp of a rapid growth phase of innovation (Display).

Theme 1: The Start-Up Enablers

Many smaller technology companies are driving disruptive innovation. By developing the must-have tools used by new economy start-ups, their products are the engines of the unfolding technology revolution. With the increasing acceptance of pay-as-you-go cloud-based infrastructure and services offerings, barriers to entry for entrepreneurs have nose-dived. The average mobile app start-up needs just 5% of the capital that a dot-com–era start-up required, thanks to these enablers.

For example, Zendesk, a US company, offers a simple and affordable suite of products for businesses to communicate and serve customer support issues across channels that meets the evolving needs of enterprises in a digital and mobile world. Atlassian, based in Australia, provides collaborative software that improves productivity among teams within an organization. And Shopify of Canada provides a one-stop shop that enables start-ups and brick-and-mortar companies to set up an online storefront.

Theme 2: Empowering Digital Transformation

In an increasingly competitive climate, businesses that extract and understand data intelligence can gain an edge on competitors. Many companies are in the early stages of transitioning to digital manufacturing and automating their entire operations. Technology firms that provide the enterprise tools to harness information and drive improved productivity possess tremendous growth potential.

For example, French company Dassault Systèmes sees robust outlook in its product lifecycle management technology called 3D Systems, which helps companies reengineer their design and manufacturing processes digitally. ANSYS of the US makes software that expedites the development of autonomous driving systems by simulating millions of road conditions and improving computer learning. Semiconductor companies such as NVIDIA provide the supercomputing power to “train” computers to mimic human behavior, the first step in artificial intelligence.

Homework: Bottom-Up Analysis

While we are confident about the outlook for continued technology spending, identifying promising investment candidates is challenging. For many high-growth technology companies, valuations tend to be lofty, reflecting high-growth expectations for both revenue and earnings. The prevalence of cloud infrastructure and lowered entry barriers means the pace of innovation is accelerating. Only a limited number of companies with defensible and differentiated business models and a large addressable market will be able to deliver sustained growth toward profitability. This favors a selective approach and fundamental analysis, in our view.

Technology themes can also help point the way. In the era of big data, companies that provide cloud-based infrastructure and services functions to the broad economy seem poised to benefit. They’re like a power grid for the new economy—especially companies that provide tools to help enterprises gather, process, understand and utilize big data to improve productivity. Investors who find them can enjoy exposure to the power of technology growth trends with a degree of insulation from the regulatory risk hanging over the sector.

Lei Qiu is Portfolio Manager—International Technology Fund at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein