Year to date, the municipal market has posted exceptionally strong returns of more than 7%. Investors have shown munis the love, driving 39 consecutive weeks of inflows that reflect solid and sustained interest. Nevertheless, low yields and an aging US expansion continue to top investors’ concerns as we enter the home stretch of 2019.

If there’s one theme that unifies muni investors’ questions and concerns, it’s how to resolve the tension between risk and return in increasingly uncertain conditions. And if there’s one overarching investment takeaway, it’s that active and flexible strategies can effectively balance risk and reward when conditions are evolving and visibility is limited.

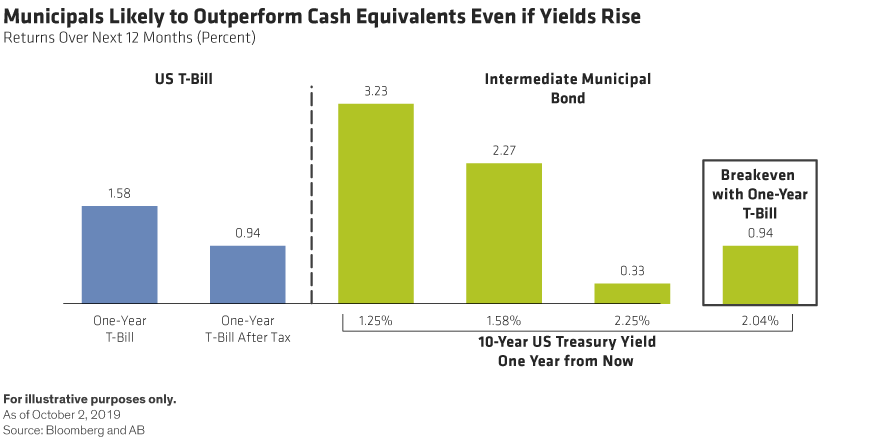

With municipal bond yields so low, aren’t I better off investing in cash equivalents?

Whether they’ve been sitting on the sidelines for months or are contemplating a quick exit, some investors believe that municipal yields are too low to warrant staying invested. Instead, they’re turning to cash equivalents to provide the ballast they’d otherwise expect from muni bonds.

However, looking forward, the range of possible outcomes—stable, falling or rising rates—strongly favors staying invested, despite low yields. In Display 1, we’ve used a one-year US Treasury bill yielding 0.94% after taxes as a proxy for the earnings on cash over the next 12 months.

For investors to be better off parking their money in cash, municipal bond yields would have to rise, and their prices would have to fall, by an amount consistent with a rise in 10-year Treasury yields to more than 2%. That prospect seems remote in an environment of easing monetary policy and heightened equity volatility.

In addition, municipal bonds will likely continue to experience supportive technical conditions. Although supply has begun to increase as issuers take advantage of the decline in interest rates, demand remains very strong. Combined with all the other ingredients that led to a strong run in municipals year to date and that remain in place today—low global yields, an expanding (albeit decelerating) economy and a volatile equity market—favorable supply/demand factors suggest stable municipal yields and prices in the fourth quarter.

Lastly, sitting out a period of low yields amounts to market timing. Successful market timing is virtually impossible, as history has repeatedly shown—even for professional money managers. That’s because no one can predict exactly when yields will rise. And in the meantime, sidelined investors concede the after-tax yield advantage that comes with being invested, as well as any potential price gains associated with further yield declines.

Indeed, muni investors who opted for cash positions in lieu of municipal debt at the start of 2019 saw their decision backfire as munis resoundingly beat one-year T-bills over the next three quarters as yields fell unexpectedly.

Bottom line? Stay invested.

Could we see negative municipal bond yields down the road?

Most market participants expected US yields to rise in 2019, but instead they declined. Slowing economic growth, low inflation and Fed policies that suggest rates will remain low for the foreseeable future have all contributed. Elsewhere in the world, the volume of outstanding debt that carries negative yields has ballooned to US$15 trillion under similar pressures. Could we see negative yields in the US as well?

We don’t think so. We expect US economic and inflation growth to hover around 2%, which effectively puts a bottom under yields. However, if investors have strong convictions that yields will continue to fall and even turn negative, they should invest in bonds now.

Are municipal fundamentals worrisome this late in the cycle?

Today’s expansion is the longest on record, and municipal governments have used the extended period of economic growth and rising employment levels to shore up their fundamentals.

State and local government tax receipts skyrocketed 18% year over year in the second quarter, according to the US Bureau of Labor Statistics. Even more telling, tax receipts in 2019 came in at $1.8 trillion, compared with $1.3 trillion in 2007.

State and local officials have been prudent managers of these growing revenues, as evidenced by strong growth in rainy-day reserve funds. Such funds climbed from less than 2% as a percentage of general fund spending in 2010 to more than 7% today. Reserves are now at their highest levels in 20 years. Rainy-day reserve funds provide a cushion in the event of an economic downturn or a recession.

Rating agencies have rewarded this fiscal discipline; for the past five years, upgrades have outpaced downgrades across the municipal market. During the second quarter of 2019, upgrades accounted for 71% of rating migration during the second quarter.

In short, municipal issuers are generally well positioned for a turn in the credit cycle.

How do I get more income without accepting too much risk?

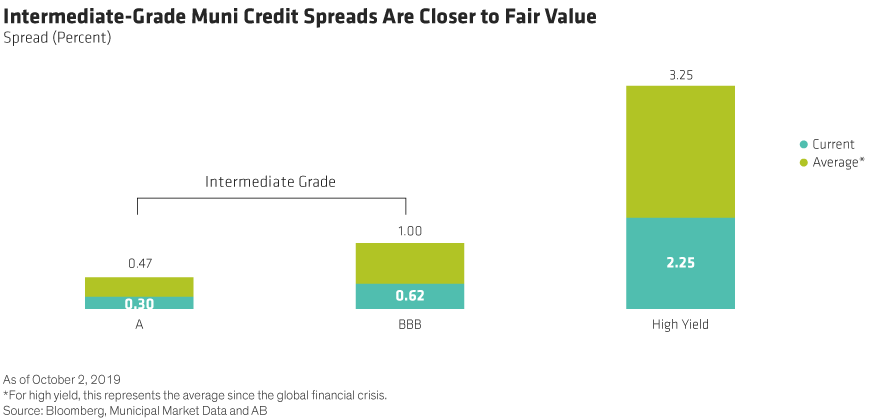

Yield-hungry investors have poured money into high-yield munis this year, driving high-yield spreads down to 2.25%, well below their post-2008 average of 3.25%. In our view, while today’s spreads don’t suggest a bubble, these narrower levels indicate that now may not be the time for municipal credit investors to invest enthusiastically in the high-yield part of the market.

This doesn’t mean that investors should ignore high-yield munis altogether. But it does call for a more selective approach to the sector. As investor enthusiasm has grown, so have the number of relatively risky deals featuring borrowers such as nursing homes or charter schools, which lack direct taxation power and don’t provide an essential service such as clean water or sewage treatment.

Meanwhile, income and opportunities exist elsewhere in muni credit. Spreads on both A-rated and triple-B-rated muni bonds are running closer to their long-term averages (Display 2), implying more room for spread tightening in these areas. Healthier financial conditions also bode well for these intermediate-grade issuers.

Both high-grade and high-yield investors that have the flexibility to move into other types of bonds when appropriate may benefit from a diversified position in intermediate-grade municipal bonds. Investors should focus on careful selection that maximizes opportunity and minimizes risk.

Be Responsive to Market Conditions

Active muni managers with flexible approaches have more tools and strategies at hand for navigating the challenges that dynamic markets present. Investors who keep their hands on the wheel will be better positioned to respond to the potential pitfalls or opportunities that may be around the bend.

Daryl Clements is Portfolio Manager—Municipal Bonds at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein