As economic cycles enter their later stages, investors sometimes find that they’re taking too much risk to generate income. There’s a strategy that can help—and we think now is the time to use it.

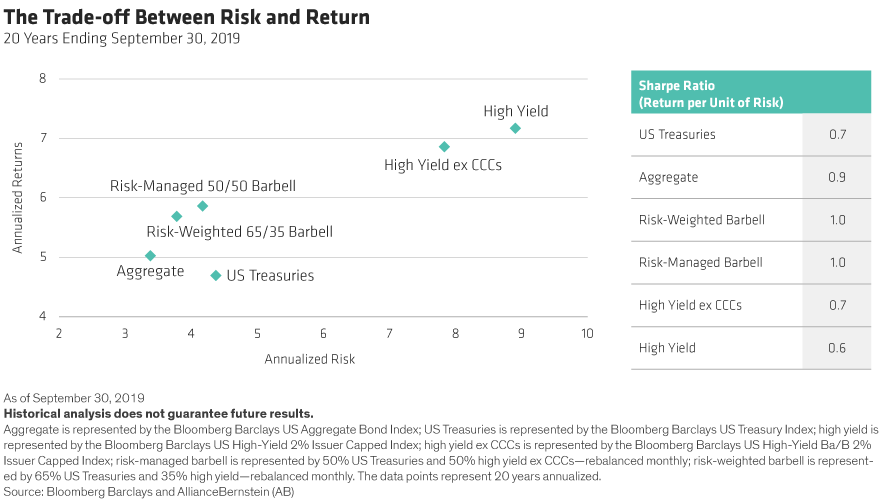

Pairing high-yield corporate bonds and other credit assets with high-quality government debt in a dynamic “barbell” strategy has been a good way to generate income while limiting downside risk. This is mainly because the return streams tend to be negatively correlated; one does well when the other struggles, and a manager can alter the weightings as valuations and conditions change.

A barbell approach can work at any time in a market cycle, but we think conditions today are especially ideal for it—in particular, for investors who want to limit their downside risk without giving up too much income. Here are three reasons to lift a barbell today:

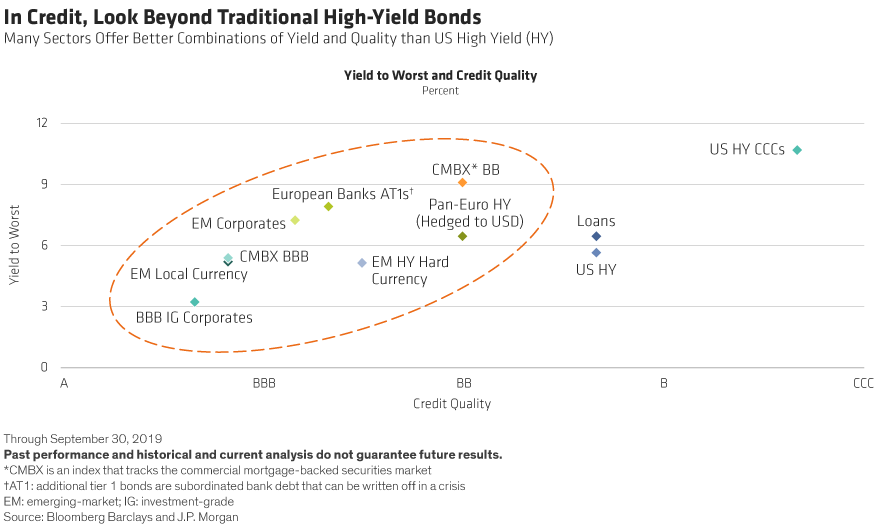

1. You’re not being paid to take all that credit risk. Most credit assets are expensive today. Take the US high-yield market. The average yield spread—the extra yield over comparable government bonds—has averaged 3.94% over the first nine months of the year. That’s well below the long-run average (dating back to January 1, 1994) of 5.46%.

This should be a concern for investors who reduced duration—a measure of interest-rate sensitivity—when interest rates were rising and overallocated to credit. That was a common strategy in 2018 as the US Federal Reserve (the Fed) delivered four interest-rate increases and economic growth was strong.

Here’s the problem: both actions reduce the defensive nature of a bond portfolio in a risk-off environment. At 10 years and counting, the US credit cycle is one of the longest on record. At some point, the expansionary period will end and the downturn phase will begin. We’re not quite there yet, but we think we’re getting closer—and so does the Fed, which has already cut rates twice this year.

With trade volume collapsing, we expect 2020 to be the worst year in a decade for the world economy. And while we don’t expect a US recession, we do think the economy will slow, and we’re watching to see if a manufacturing slowdown starts to affect consumer spending. That likely would mean more Fed rate cuts to come and, if necessary, even more aggressive easing.

All of this tells us two things. First, investors who are overweight credit aren’t being properly compensated for the risk. Second, there’s no reason to fear duration. The possibility of slower growth ahead means interest-rate exposure should help to cushion your portfolio against volatility and drawdown risk.

2. US yield curves are flat. This happens when long-term yields aren’t as high as they normally are relative to shorter and intermediate yields. Why does this matter? Because when the curve is flat, returns tend to be stronger in higher-quality securities and lower in some of the bond market’s riskiest segments.

With a barbell, a manager can rebalance investors’ portfolios as the curve flattens by tilting toward higher-quality, interest-rate-sensitive securities at the expense of the riskiest sectors of the credit market. This makes a portfolio more liquid. Should credit markets sell off, investors can sell their outperforming US Treasuries and other highly liquid quality assets and rebalance toward higher-risk assets at more attractive prices.

When it comes to the credit side of the barbell, flat curves make higher-quality, intermediate maturity bonds more attractive than longer ones because they deliver more yield per unit of duration, with the sweet spot somewhere between three and five years.