US value stocks staged a strong recovery in September after an extended period of underperformance. While value slipped again in early October, we’re monitoring four signals that might indicate whether we’re on the cusp of a bigger value rebound.

Since 2017, US growth stocks relentlessly powered ahead of value stocks. Ultralow interest rates and fears of a weak macroeconomic growth recovery have suppressed stocks with attractive valuations, which tend to be more sensitive to the economic cycle. At the same time, the ever-increasing popularity of mega-cap technology and new media names captured the imagination of investors who seek to tap sources of growth in a low-growth world.

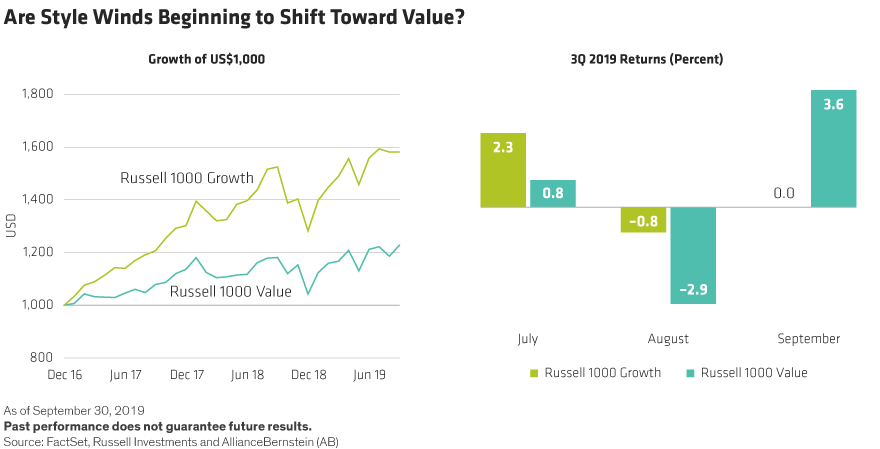

Growth-Value Gap Looks Stretched

But in September, change was in the air. The Russell 1000 Value Index advanced by 3.6%, outpacing the Russell 1000 Growth Index, which was flat (Display). In early October, the style winds turned against value once again. Still, several trends suggest that the preference for growth over value stocks may have run its course.

The S&P 500 Index has come through an extended period during which growth-style stocks outperformed their value-style peers. By some estimates, the current extreme difference between growth and value performance matches that experienced prior to 2000 and 2009. Both of those years proved to be the beginning of multiyear periods of great returns for value stocks. As a result, sector valuations look distorted: the price/forward earnings of US technology stocks is 9% above its long-term average since 1990, while financials are trading at a 9% discount to their long-term average.

Of course, these trends don’t guarantee that value stocks will come charging back. However, some key signals could help identify whether value stocks are poised for a longer-term recovery.

-

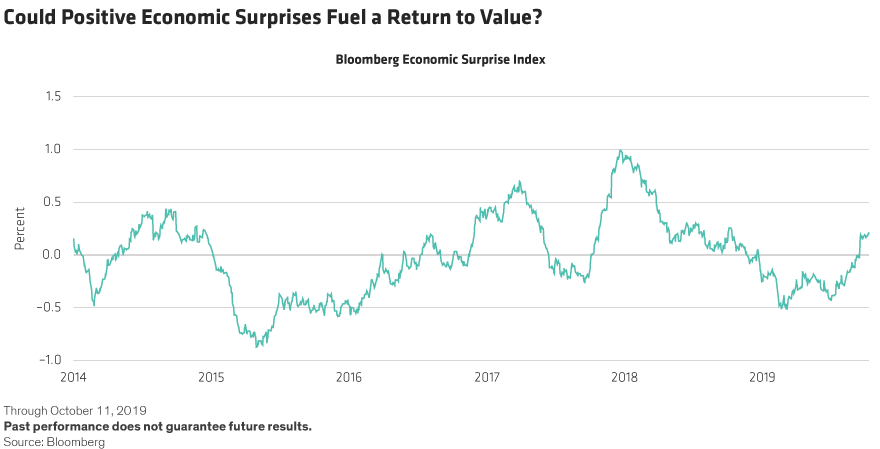

Stabilizing or improving economic trends: For several quarters, pessimism over economic growth has become pervasive among investors. In 2019, consensus expectations for economic growth and Fed policy have turned around. Just 12 months ago, the 10-year Treasury yield was 3.2% and consensus expectations called for additional Fed rate hikes and more balance-sheet shrinkage. By quarter-end, the 10-year Treasury was at 1.67%, while the US Federal Reserve has cut interest rates twice. Meanwhile, the trade war with China and the inverted yield curve have added to recession fears. These concerns are understandable, but may be overdone. We believe that if we begin to see positive economic surprises, this may counter the current pessimism and could lead to better performance for economically sensitive stocks. In fact, the Bloomberg Economic Surprise Index reached an 11-month high in September (Display).

-

Reduced demand for sovereign debt: The growth megatrend has mirrored the move down in rates. A little bit of risk awareness in bonds could lead to much less risk aversion in stocks that could benefit value stocks, which tend to have riskier profiles.

-

Disruption for the disruptors: The world is experiencing a historic wave of productivity improvement as technology fuels widespread disruption of traditional businesses. Consumers are benefiting from a combination of lower prices, more convenience and better experiences across a range of industries, including online shopping, ride-sharing and music apps. Yet from a corporate perspective, the path to profits isn’t always clear. Signs that the disrupters are having trouble making money could prompt a shift in investor sentiment. For example, the recent low price point for Apple’s new subscription streaming service triggered panic selling in Netflix.

-

IPO weakness and venture capital losses: Investors have closely watched the recent flops of IPOs for high-profile unicorns, private companies worth at least $1 billion. After shares of Uber and Lyft plummeted since they went public, WeWork’s offering was withdrawn in September. The failed IPOs may signal scepticism toward companies with fantastic growth projections. After a period of record fundraising for venture capital firms, potential venture capital losses might make investors rethink the quest for growth at any cost and refocus on companies with resilient business models and earnings backed by sustainable cash flows. We believe that improving economic data, paired with a renewed focus on diligent investments in companies with solid fundamentals and low valuations, could energize value stocks.

Banks Poised to Rebound

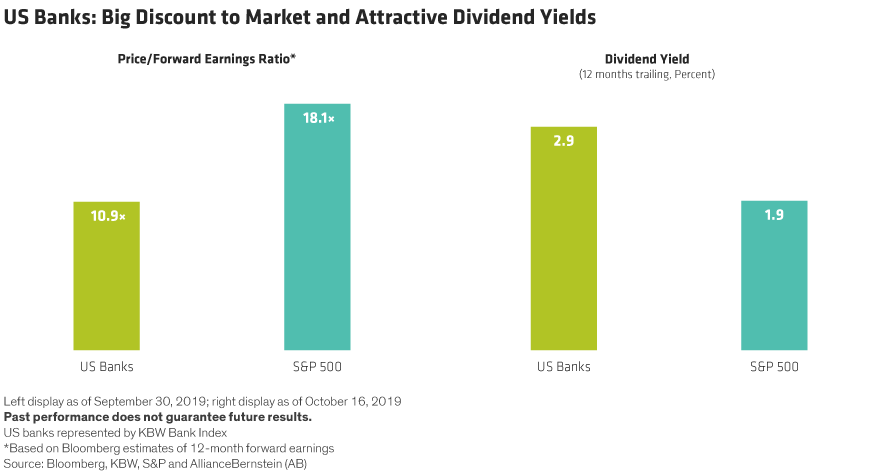

If value enjoys a renaissance, we would expect cheap stocks to gain even on modest downward revisions. Banks are a case in point, as they have very low P/E ratios even after outperforming in 2019 to date (Display). In aggregate, lenders are growing earnings faster than the S&P 500 even in a challenging operating environment. And our research suggests that their capital returns (dividends plus buybacks) are the best of any sector.

It’s still too soon to say whether the value comeback will continue. But we believe that after such an extreme flight from value in recent years, there are early signs of a shift that suggest a style turn toward attractively valued stocks is in the making.

Kurt Feuerman is Chief Investment Officer—Select US Equity Portfolios at AllianceBernstein

Robert Milano is Product Specialist—US Equity Portfolios at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein