Third-quarter earnings season is in full swing, and surprises at the sector level have been overwhelmingly to the upside. The ebb and flow of geopolitical risks, along with mixed signals from the economic data (and the markets), are making it difficult to commit to either a defensive or pro-cyclical stance on equity sectors from a top-down perspective.

However, the bottom-up fundamentals of the sectors not only tell us what’s driving overall S&P 500® earnings growth, but also help inform our decisions on sector ratings.

Topsy-turvy economic and market messages

The path of the economy is somewhat of a mystery right now. Are we emerging from a mid-cycle slowdown or on the precipice of a recession? Economic data has been quite bifurcated, and although recession fears have ebbed recently, the ongoing flood of policy-changing tweets out of Washington means we cannot give an all-clear—particularly as the election season heats up.

While consumer sentiment and spending have remained strong amid a strong job market, business confidence and investment have dropped within the context of sharp weakness in the manufacturing space. After cutting short-term interest rates for the third time this year in October, the Federal Reserve is also apparently uncertain, as it signaled that it may stand pat until it can determine the impact of the smoldering risks.

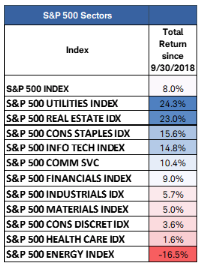

At times, relative sector performance can provide confirmation of the economic landscape. And perhaps it has—it’s mixed! As you can see in the table below, both cyclical and defensive sectors have outperformed at the same time the market sets new highs. None of this is particularly decisive in terms of making our sector calls.

Both cyclical and defensive sectors have outperformed during the past year

Source: Schwab Center for Financial Research, Bloomberg, as of 11/4/2019. Past performance is no guarantee of future results.

How we read the tea leaves

As you may be aware, we in large part look though a top-down (macroeconomic) lens when formulating our equity sector views, starting with the overall economy and driving down to industry level. In the last installment of Sector Views, we delved into the impact interest rates have on relative sector performance. We also focus on trends that are specific to individual industries—whether it be secular changes in demographics or burgeoning technologies. While we don’t do analysis on individual companies, we do analyze their fundamentals and valuations as they are rolled up to the sector level.

Earnings season shakers and movers

Given that we’re heading into the final innings of earnings season—let’s take a look at the quarterly sector data and how it is affecting the overall market’s earnings landscape.

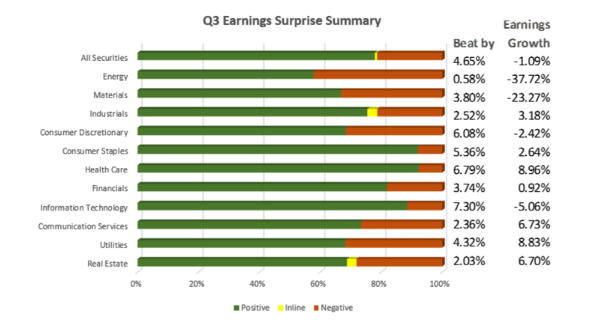

So far, Q3 earnings generally have surprised to the upside

Source: Schwab Center for Financial Research, Bloomberg, as of 11/06/2019. Quarterly earnings estimates are based on consensus forecasts according to Bloomberg Earnings Estimates (BEst) of the consistent stocks. Horizontal axis shows the percentage of companies in each sector that have reported earnings that were either more positive, in line or more negative than the consensus estimate for the company’s earnings. “Beat by” is the percentage by which reported earnings have surpassed the consensus estimate for the sector. Earnings growth is based on a year-over-year comparison with Q3 2018.

As the chart above shows, the vast majority of companies reporting so far have beat estimates—led by the Consumer Discretionary, Health Care and Technology sectors. Yet earnings growth of the S&P 500 (top row, right column) is reflecting retrenchment for Q3 2019 compared to the same quarter last year. Energy, Materials and Technology are the culprits. However, it’s important to consider that year-ago earnings overall were particularly strong on the heels of the 2017 tax legislation and jump in economic growth in 2017-2018. So it was a relatively high hurdle that is weighing on the year-over-year comparison, as can be seen below.

Year-over-year earnings growth faces a high bar vs. 2017 and 2018

Source: Schwab Center for Financial Research, Bloomberg, S&P 500 Index, as of 11/04/2019. Quarterly forward earnings estimates are based on consensus forecast according to Bloomberg Earnings Estimates (BEst) of the consistent stocks.

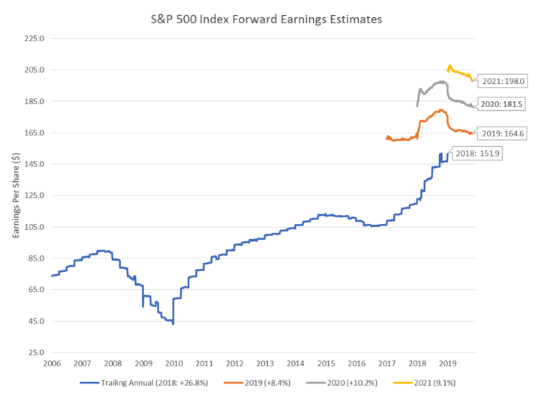

In reality, the trend in earnings growth for the S&P 500 index actually remains strong, as can be seen in the quarterly estimated growth trend in the chart above, as well as in the annual forward earnings trend below, with calendar years 2019-2021 earnings expected to continue to climb. It is important to note, however, that those estimates have been coming down. While this is the typical pattern for consensus estimates, as excessive optimism merges with reality, we are keeping a close eye on the sharper drop off in longer-term earnings growth expectations that may be signaling that a cyclical peak in earnings is near.

Earnings are expected to continue to climb in 2019 through 2021

Source: Schwab Center for Financial Research, Bloomberg, as of 10/28/2019 Annual forward earnings estimates are based on the consensus forecasts according to Bloomberg Earnings Estimates (BEst) of the consistent stocks.

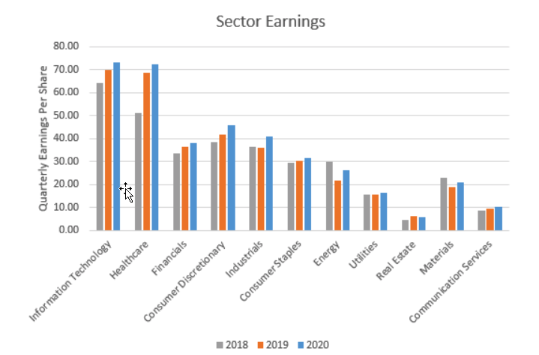

Bringing it back to the individual sectors, the trend in annual earnings is generally positive over the next two years. While the Energy and Materials sectors still face the usual volatility common to the commodity-intensive sectors, the growth in forward earnings estimates for the other sectors are supportive of continued gains expected for the overall S&P 500 Index.

Source: Schwab Center for Financial Research, Bloomberg, as of 11/04/2019. Yearly earnings are estimates for 2019 and 2020, and are based on consensus forecasts according to Bloomberg Earnings Estimates (BEst) of the consistent stocks.

How does this shape our views?

As we stated above, the mix of signals at the macroeconomic level makes it difficult to pin down strong views on most of the sectors. So, we must rely more heavily on long-term industry trends and fundamentals to provide more clarity into the sectors that are less affected by the macro environment.

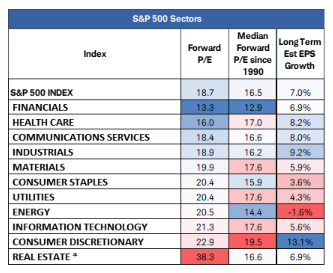

The Health Care sector is currently the only sector we expect to outperform the broad market over the next three to six months. While there is considerable political risk as the presidential election season heats up and candidates discuss health-care system reform ideas (such as “Medicare for all”), long-term demographic trends, strong balance sheets and the potential for increased dividends provide a tailwind for the sector. Additionally, the Health Care sector is poised to see the strongest growth in earnings this year.

While the Health Care sector’s long-term earnings growth projection is average, it sports the second-best valuations of the S&P 500 sectors—and is currently the only one with a price-earnings (P/E) ratio below its long-term median. Finally, just in case the economy slips toward recession, it is after all a historically defensive sector.

* National Association of Real Estate Investment Trusts (NAREIT Total Average Price to Funds From Operations REIT EquitySource: Schwab Center for Financial Research, Bloomberg as of 11/4/2019. Forward earnings estimates are based on consensus 12-month forecasts according to Bloomberg Earnings Estimates (BEst) of the consistent stocks. Long Term earnings estimates are based on consensus five-year forecasts according to Bloomberg Earnings Estimates (BEst) of the consistent stocks.

A final word

Keep in mind, no matter what our view is on any of the sectors, remaining diversified is very important. Concentrating in too few sectors can dramatically affect the risk profile and performance of your portfolio. So if you do make any sector tilts in your portfolio, keeping them small is a good way to maintain appropriate diversification and potentially enhance performance of your portfolio.

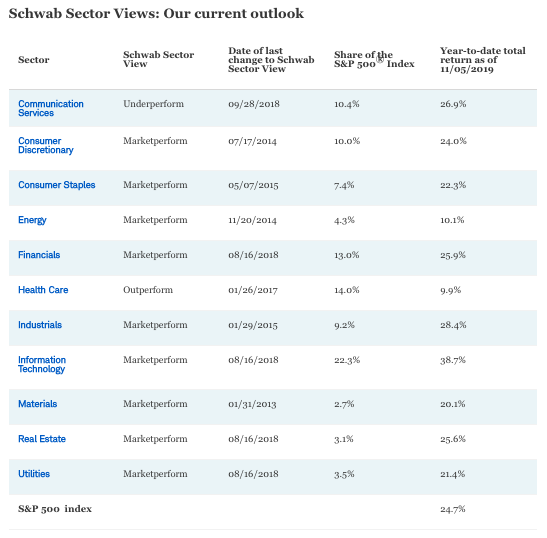

Source: Schwab Center for Financial Research, FactSet (for YTD total returns) and S&P Dow Jones Indices (for S&P 500 sector weightings). Sector performance data is based on total return for each S&P 500 sector subindex (see “Important Disclosures” for index definitions). Sector weighting data is as of 09/30/2019; data is rounded to the nearest tenth of a percent, so the aggregate weights for the index may not equal 100%.

Past performance is no guarantee of future results.