Halloween brought more treats than tricks as November brought the first real S&P 500 break out of its long and volatile trading range dating back to January 2018. Hopes for a United States-China trade deal and ample liquidity courtesy of the Federal Reserve have been in focus; although economic data is not confirming the market’s latest advance. Bulls are saying the market is right and economic data will imminently (or eventually?) catch up; bears are saying the economy is right and the market has gotten ahead of itself.

In the middle of the debate

With a tactical recommendation of “neutral” as it relates to overall U.S. equity exposure (but an overweight to large cap stocks at the expense of small cap stocks), I would put myself squarely in the middle of that debate. But if I were a betting gal (I hate gambling), I’d place a small wager on the bear’s case that the market may have gotten a little ahead of itself. That brings up the topic of this report: an update on investor sentiment and positioning and what they might say about the near-term direction of the market.

As most readers know I keep an eye on myriad sentiment indicators—both of the attitudinal and behavioral variety. The chart below shows the popular Crowd Sentiment Poll (CSP) calculated by Ned Davis Research (NDR). It’s an amalgamation of seven distinct sentiment indicators—including the attitudinal survey from the American Association of Individual Investors (AAII) and the behavioral put/call ratio.

Extreme optimism

As you can see in the chart below, the CSP shows sentiment as having poked its head out of neutral into the “extreme optimism” zone, albeit at the bottom rungs. In the accompanying table, you can see that stock market performance in this zone has generated the weakest annualized returns.

Optimism Back (Slightly) Into Extreme Zone

Source: Charles Schwab, Copyright 2019 Ned Davis Research, Inc, as of 11/12/2019. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

Two of the components of NDR’s CSP are below. AAII’s sentiment survey shows bulls near their prior highs of this year; however, well below the spike in bulls that ushered in 2018. The CBOE equity put/call ratio is at its lowest level so far this year; but not quite as low as what was experienced during last year’s extreme December volatility. [The put/call ratio—created by my first boss/mentor, the late-great Marty Zweig—is an indicator of investor sentiment, where a large proportion of puts to calls indicates bearish sentiment, and vice versa.]

Investors Responding Bullishly Again

Source: Charles Schwab, Bloomberg, as of 11/14/2019.

Options Traders at Optimistic Extreme

Source: Charles Schwab, Bloomberg, as of 11/15/2019.

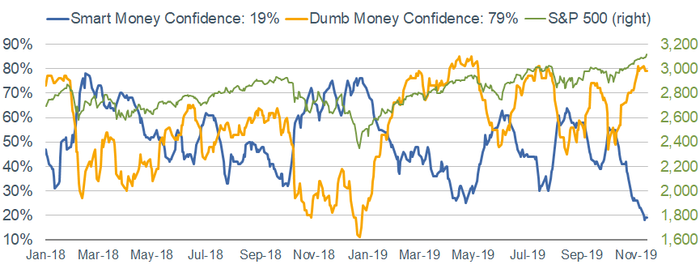

Smart vs. dumb money

Finally, one of my favorite sentiment indicators—and one of the most popular ones I show in my writings or in client presentations—is constructed by SentimenTrader (ST) on a daily basis. The Smart Money and Dumb Money Confidence indices are a unique innovation that show what the “good” market timers are doing with their money compared to what “bad” market timers are doing.

ST’s Confidence indices use mostly real-time gauges—there are few opinions involved in them. Generally, you want to follow the Smart Money traders when they reach an extreme and do the opposite of what the Dumb Money traders are doing when they are at an extreme.

Examples of some Smart Money indicators include the OEX put/call and open interest ratios, commercial hedger positions in the equity index futures and the current relationship between stocks and bonds. Examples of some Dumb Money indicators include the equity-only put/call ratio (like shown above), the flow into and out of the Rydex series of index mutual funds, and small speculators in equity index futures contracts.

Because the “dumb money” follows trends, and the “smart money” generally goes against trends, the “dumb money” is usually correct during the meat of the trend. However, when it becomes too positive, and sentiment has reached an extreme, stocks typically run into trouble. That has historically typically happened when Dumb Money Confidence rose above 60% and Smart Money Confidence has fallen below 40%.

Well, see below. Clearly, we are at one of those historical extremes. As of Friday, the five-day average of the Smart Money/Dumb Money Confidence spread has moved below -60%. In the past decade, this happened on 55 days, leading to further gains for the S&P 500 over the next two months after only 20 of them (a low 36% “win rate”), with a median return of -3.0%.

“Dumb Money” & “Smart Money” at Opposite Extremes

Source: Charles Schwab, SentimenTrader, as of 11/15/2019.

In sum

For the past near-two years we have been pointing out the confluence of uncertainties that have meant the market could “go either way”—including most obviously trade/tariffs, but also the related economic trajectory, Fed policy and geopolitical/political uncertainty. It has led to a wide trading range—the peaks and valleys of which have been driven as much by extremes in sentiment as they have by the changing dynamics of the underlying fundamentals. In light of that, and the extremes of sentiment we are witnessing again, investors should not view the market’s latest high with rose-colored glasses.

© Charles Schwab

Read more commentaries by Charles Schwab