The coronavirus outbreak in China unnerved investors in January, leading to a sharp (but short) U.S. stock market drop. Although stocks quickly resumed their rally toward new highs, the reaction highlighted stocks’ near-term vulnerability. At the same time, divergences and weak spots have become apparent in global economic data. Here’s what we’re watching.

U.S. stocks and economy

Although the U.S. economy ended 2019 on solid footing, certain weak spots were clearly developing by the end of the year. The coronavirus outbreak in January further exposed stocks’ vulnerability in the short term. Here are some of the cautionary signs we’re seeing.

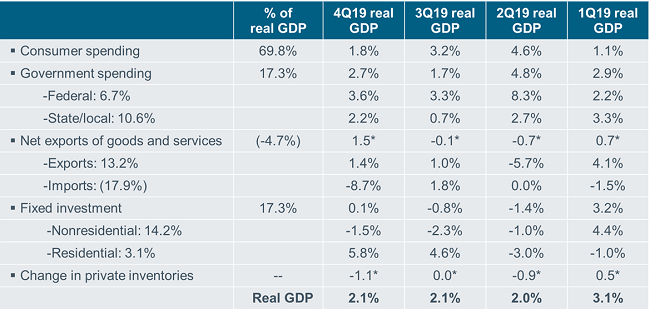

1. Gaps between headline and underlying data: Despite weakness in both manufacturing and business investment, U.S. gross domestic product (GDP) growth, at 2.1%, managed to beat expectations in the fourth quarter, chugging along at the same pace as in the third quarter.

However, rough patches are apparent in underlying data. Business investment remained considerably weak through the end of the year. Imports plunged by the most since 2009, highlighting a significant decline in both consumer and corporate demand. As imports dropped, exports became a much bigger contributor to the 2.1% overall GDP growth. Meanwhile, consumer spending was still positive, although weaker than in prior quarters, highlighting the split between stronger consumption and weaker business investment.

GDP growth was unchanged from 3Q 2019, but was lifted considerably by net exports

Source: Charles Schwab, Bureau of Economic Analysis, as of 12/31/2019. *Represents contribution to percent change in real GDP. Numbers may not add up to 100% due to rounding. Real GDP based on annualized Q/Q % change.

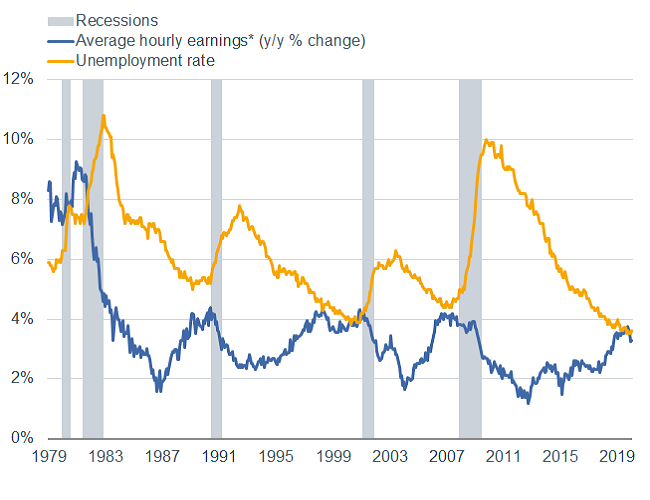

2. Lackluster job and wage growth: Meanwhile, job growth was tepid in 2019. The 175,000 average monthly job gain was the slowest since 2011, although the unemployment rate remains low at 3.6% and nonfarm payroll gains have beaten expectations lately. Average hourly earnings for production/nonsupervisory workers grew 3.3% year over year in January—also lukewarm.

Average hourly earnings growth and the unemployment rate have converged, a phenomenon that is typical in the latter stages of the economic cycle. You can see from the chart below that in the past three cycles, these convergences typically occurred shortly before recessions (with the exception of mid-1998, where convergence preceded a recession that didn’t begin until 2001).

Wage growth and the unemployment rate have converged

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics, as of 1/31/2020. *Average hourly earnings for production and nonsupervisory workers, which excludes the supervisory group.

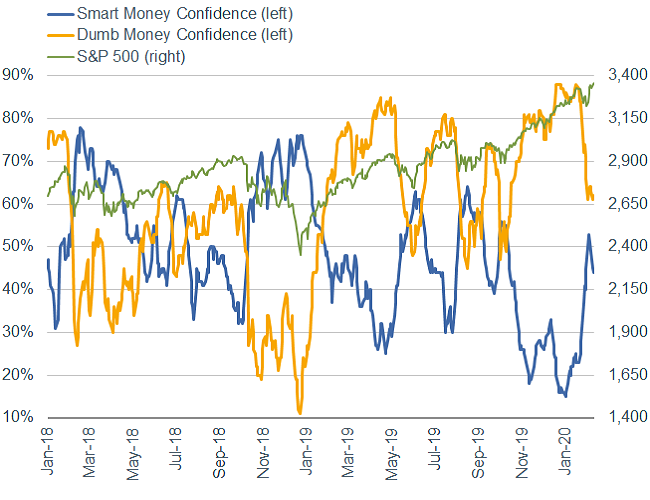

3. Rapid convergence between “smart” and “dumb” money confidence: As the coronavirus outbreak worsened in January and began spreading to countries outside China, fears rose about its potential global economic impact.

Investor sentiment shifted quickly. You can see this in the chart below, which shows the rapid convergence between “dumb money” confidence (“dumb” is SentimenTrader’s shorthand term for short-term speculators, inclusive of retail investors and odd-lot traders, who typically follow market trends) and “smart money” (long-term investors including commercial hedgers and institutions). Since December, the gap between SentimenTrader’s Smart Money/Dumb Money Confidence Indexes has been extremely wide, but it narrowed swiftly in late January as the coronavirus outbreak emerged. At the same time, stocks became more volatile.

Both “smart” and “dumb” money confidence converged rapidly amid coronavirus concerns

Source: Charles Schwab, SentimenTrader, as of 2/11/2020. Confidence Indexes are presented on a scale of 10% to 90%. Past performance is no guarantee of future results.

Historically, “smart” money has typically been correct at extremes, although it has obviously not been correct for much of the market’s recent rally. The reaction to the coronavirus outbreak suggests that extreme sentiment alone doesn’t necessarily mean a market pullback is imminent, but rather that stocks are more vulnerable to shocks in the near term—which in this case is the outbreak’s threat to global economic growth.

Global stocks and economy

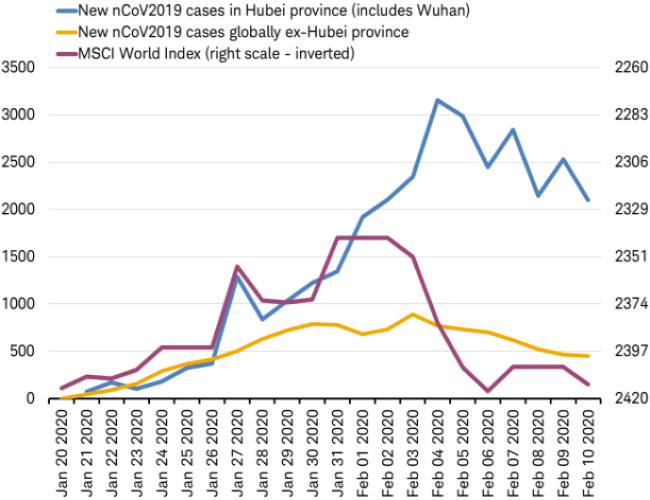

Coronavirus has dealt a setback to the emerging global economic recovery. Although extended workplace shutdowns in China associated with the coronavirus outbreak have reverberated throughout the global economy, much of China’s production may soon come back on line—likely delaying, but not derailing, the growth recovery.

The coronavirus continues to rage in Hubei (the province that contains the epicenter of Wuhan) and reports of new cases there may be underreported by the health commission. However, the growth rate of new cases everywhere else in China and around the world seems to have peaked, helping to reverse the stock market decline. Hubei is not the core of China’s manufacturing, accounting for only 1% of China’s integrated circuits and TVs and just 2% of mobile phones. Workers outside of Hubei are set to return to work soon, encouraged by evidence that the outbreak may be contained.

Growth in new coronavirus cases outside of Hubei may have peaked

Source: Charles Schwab, World Health Organization, Health Commission of Hubei province, data as of 2/10/2020.

If production soon comes back online, what impact will the coronavirus have on economic data? Our analysis of 13 global pandemics over the past 50 years (Will the Coronavirus Outbreak Lead to a Market Breakdown?) shows that once the number of newly identified cases start to decline, economic activity and the stock market tend to quickly rebound.

As the recent coronavirus outbreak was barely evident in the January economic data, we expect a sharp, but temporary, hit to February economic data. The first report where this may show up is in the preliminary February manufacturing purchasing managers’ indexes (PMI), due February 21st for many countries. However, China’s PMI won’t be available until March 1st. Because it’s the second largest country weight in the global PMI, the factory shutdowns in China may cause the global manufacturing PMI, which has signaled expansion for the past three months, to slide back below 50 (the threshold between expansion and contraction).

The potential drop in the PMIs would follow a broad recovery seen through January:

- The percentage of countries with PMIs in expansion rose above 50% in January to an eight-month high.

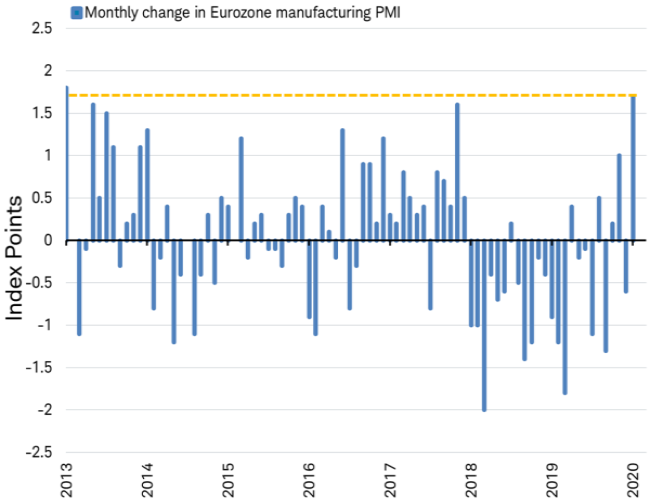

- The PMI for the Eurozone jumped 1.7 points in January, the largest gain in seven years, with every country posting a monthly gain for the first time since November 2017 (for more on Europe’s recovery see: Will Europe Lead In 2020 As 2019 Risks Fade?).

- Fading Brexit concerns helped to lift the January U.K. PMI out of contraction for the first time since April 2019.

- The emerging market PMI saw its seventh month in a row of expansion in January. For the past 12 months, the emerging market PMI exceeded the developed market PMI, something not seen for 10 years.

Eurozone PMI rose the most in seven years in January

Source: Charles Schwab, Bloomberg data as of 2/7/2020.

Although there’s still uncertainty over the spread of the coronavirus, if the growth rate of new cases is contained, then the impact may be limited and short-term.

Fixed income

The coronavirus outbreak in China has upended the outlook for the bond market. Prior to the news of the epidemic, the global economic outlook was improving. The U.S. economy was growing at a steady 2% rate, Europe appeared poised to rebound from its manufacturing slump, and emerging-market countries were benefiting from easing trade tensions between the United States and China and a slightly weaker dollar. Against that backdrop, we were expecting the Federal Reserve to keep short-term rates near the 1.5% level while intermediate and long-term rates would drift higher, resulting in a modestly steeper yield curve.

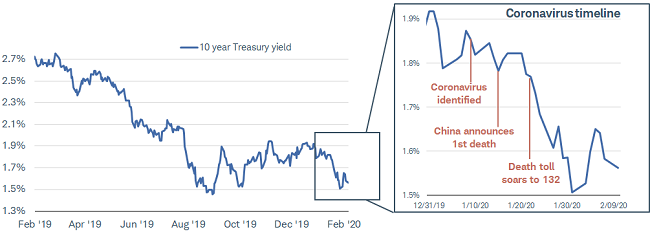

However, uncertainty about the extent of economic damage that the coronavirus will have on the global economy has roiled markets and will likely mean that government bond yields will remain low. Since news of the outbreak emerged, 10-year Treasury yields dropped sharply, while volatility has picked up.

10-year Treasury yields are still well below pre-coronavirus levels

Source: Bloomberg. Daily data as of 2/10/2020.

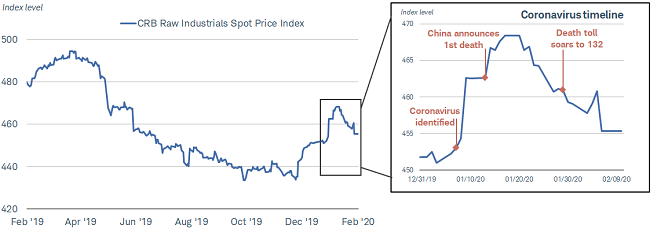

The impact of the coronavirus is likely to have a larger and longer-lasting negative effect than similar events such as SARS in 2003. China is now the world’s second-largest economy, and given its business closures, the drop in movement of people and goods throughout the region, and the decline in world trade, the negative impact to global growth is likely to be significant. It is also disinflationary, as China is the world’s largest importer of many raw materials like industrial metals and oil. Since the news of coronavirus hit, commodity prices have plummeted, putting downward pressure on inflation.

Coronavirus outbreak has had an impact on the global economy

Note: Commodity Research Bureau (CRB) Index is an index that measures the overall direction of commodity sectors. The CRB was designed to isolate and reveal the directional movement of prices in overall commodity trades.

Source: Bloomberg. Daily data as of 2/10/2020.

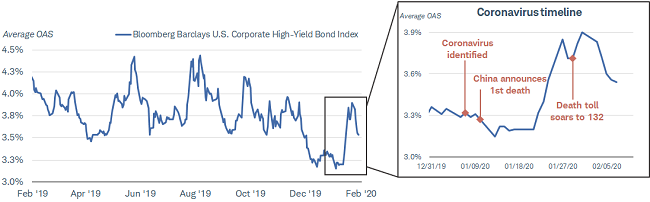

Riskier segments of the bond market, like high-yield and emerging-market bonds, are likely to underperform Treasuries because they tend to be more dependent on rising economic growth, trade and commodity prices. About 12% of the Bloomberg Barclays High Yield Corporate Bond Index is composed of energy companies. We expect the yield spread between high-yield bonds and Treasuries to increase as these risks are discounted. Prior to the coronavirus news, the yield spread was near its lowest level since October 2018, providing little reward relative to the risks.

High-yield spreads rose sharply on the initial threat of the coronavirus, but are back down to 3.5%

Source: Bloomberg, using daily data as of 2/10/2020. Option-adjusted spreads (OAS) are quoted as a fixed spread, or differential, over U.S. Treasury issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan.

Even after the worst of the outbreak has passed and recovery begins, central banks are likely to keep interest rates low to help support economies. China’s central bank has already taken steps to ease the pressure on the economy by lowering interest rates and easing lending terms. Europe and Japan have less scope to ease, because policy rates are already zero or negative in those regions.

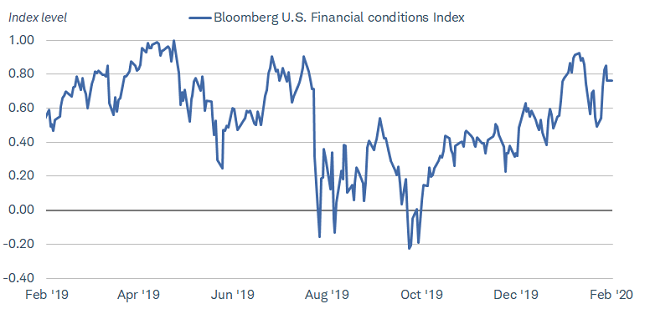

In the United States, markets are pricing in one or two rate cuts by the Federal Reserve by the end of the year—not an unreasonable expectation, but far from certain. In our view, the Fed will be watching to see if financial conditions tighten and/or inflation begins to drop as key signals to act. For financial conditions, the indicators to watch are the U.S. dollar, credit spreads (the yield difference between corporate bonds and Treasuries), and the slope of the yield curve. So far, financial conditions have tightened a bit, but are still at levels that are considered easy.

Financial conditions have tightened somewhat

Note: The Bloomberg U.S. Financial Conditions Index tracks the overall level of financial stress in the U.S. money, bond, and equity markets to help assess the availability and cost of credit. A positive value indicates accommodative financial conditions, while a negative value indicates tighter financial conditions.

Source: Bloomberg. Bloomberg U.S. Financial Conditions Index (BFCIUS Index), daily data as of 2/10/2020.

What to consider now

Historically, epidemics have had relatively minimal long-term effects on stocks. Will the coronavirus be different? It’s hard to say. Investors may have little need to take action in the near-term if their portfolios are diversified and aligned with their long-term plan. We continue to recommend that investors remain at their long-term strategic equity allocations—but use swings in either direction to rebalance back toward those targets, if necessary.

We suggest fixed income investors brace for continued volatility and low interest rates in the first half of 2020. Our outlook calls for 10-year Treasury yields to remain in a range of about 1.35% to 2%, barring a recession. We also suggest underweighting high-yield bonds and being cautious when investing in emerging-market bonds.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

SentimenTrader’s “smart money/dumb money” Confidence Indexes compare “dumb money” (generally, retail investors) indicators with “smart money” (institutional accounts) indicators.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

©2019 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

More Alternative Investments Topics >