Key Points

-

The potential for a delayed, but not derailed, manufacturing recovery in the coming quarters could fuel a rebound in commodity demand and relative outperformance by emerging market stocks.

-

Copper and oil seem to be pricing in a substantial hit to world GDP, which seems unlikely given that most of China’s workers have returned and official data shows that the spread of the virus may now be contained.

-

If growth turns out to be less negatively impacted than feared, commodities and emerging market stocks may be poised to rebound.

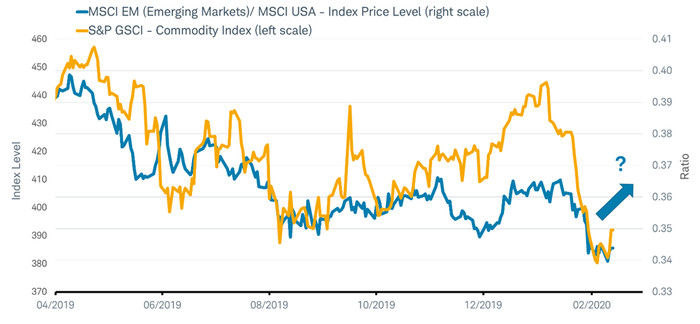

As a recovery in global manufacturing began to take hold in the fourth quarter of last year, commodity prices rose dramatically. Yet, emerging market (EM) stocks failed to see the similarly strong outperformance of U.S. stocks that typically accompanies rising commodity prices. EM stocks and commodities both demonstrate heightened sensitivity to the pace of global economic growth. EM stocks also have greater exposure to commodity producers.

A large gap developed in the fourth quarter between the trend in commodity prices and the relative performance of EM stocks. That gap closed rapidly in early 2020 as the emergence of the novel coronavirus in China was feared to wipe out manufacturing demand for materials and travel demand for oil, as you can see in the chart below. The potential for a delayed, but not derailed, manufacturing recovery in the coming quarters could fuel a rebound in commodity demand and the relative outperformance by EM stocks.

Readying for a rebound?

Source: Charles Schwab, Factset data as of 2/13/2020

The markets are split on the economic impact of the coronavirus. In general, stock markets around the world have posted gains this year. In contrast, global commodity prices have plunged and remain near lows.

- Copper fell about 13% from the start of the year. The metal’s widespread use in everything from homes to computers makes it very sensitive to the pace of growth in the global economy, and earned it the nickname “Dr. Copper.” This recent fall in copper prices set a record, sliding for 13 days in a row, to below last summer’s bottom, when U.S. trade tensions with China were escalating.

- The global benchmark for oil, Brent crude, has fallen more than 20%, plunging from $69 per barrel in early January to $54. The U.S. benchmark, West Texas Intermediate, fell below $50 per barrel. The virus outbreak threatens to curb global crude demand growth by as much as 400,000 barrels a day, according to an analysis by OPEC. At these prices, we might expect supply cuts from both OPEC and U.S. shale producers.

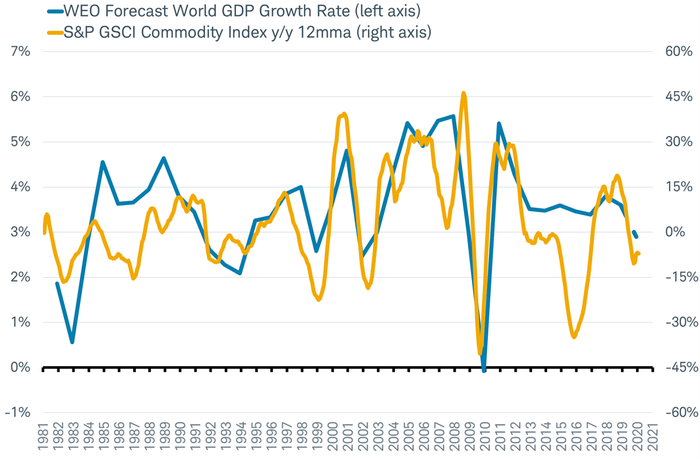

Commodities pricing in further downside to world GDP growth

Source: Charles Schwab, Factset data as of 2/14/2020.

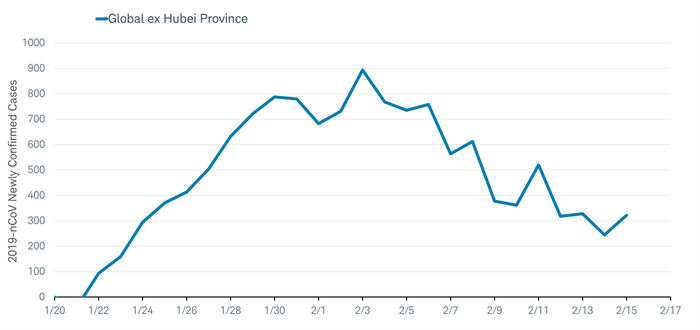

Copper and oil seem to be pricing in a further slowdown by about 0.5% of world GDP, based on similar price moves in the past, which could cause stock prices to suffer. However, such a material slowdown in global GDP seems unlikely, unless the pace of infection climbs exponentially and spreads globally. At this time, the growth of new cases around the world outside of Hubei (home to the virus epicenter of Wuhan), seems to be contained, as you can see in the chart below

Signs of stabilization in daily new coronavirus cases outside the epicenter of Hubei

Source: Charles Schwab, World Health Organization data as of 2/17/2020

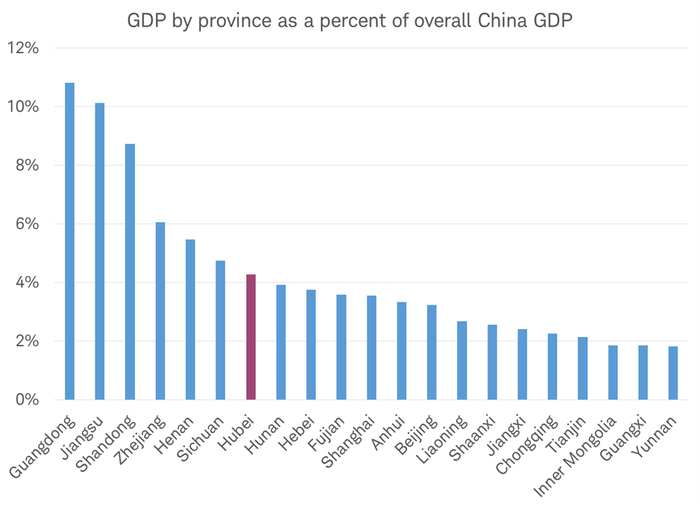

Travel bans are having a substantial impact on near-term demand for crude oil, but those could be lifted soon, leading to a potential rebound in fuel demand. Manufacturing demand for materials, including copper, may rebound quickly, with most of China’s workers having returned following about a one week extension of the Lunar New Year holiday. The return to production may be slower in Hubei province, the viral epicenter where the vast majority of infections have been reported. However, Hubei is not the center of China’s manufacturing, representing less than 5% of China’s overall GDP, as seen in the chart below. Manufacturing in Hubei accounts for just 1% of China’s mobile phone and TV production, 2% of integrated circuits and about 4% of China’s computer equipment, according to China’s National Statistics Bureau. This suggests the impact of China’s shutdowns on global supply chains may be limited.

GDP by province in China

Source: Bloomberg, individual provincial and municipal government statistic bureaus. Represents first nine months of 2019 GDP. Excludes Special Administrative Regions of Hong Kong and Macau. Data as of 2/14/2020.

There are still a lot of unknowns, and the extent of the near-term impact on economic data has yet to be assessed. The earliest data likely to show the impact of the viral outbreak are the preliminary February manufacturing purchasing managers’ indexes, due out on February 21. Dire predictions may have driven commodity prices to over-react to the downside; and now they may be poised to partially rebound, accompanied by EM stock outperformance, if growth is less negatively impacted than feared.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Commodity-related products, including futures, carry a high level of risk and are not suitable for all investors. Commodity related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations and economic conditions regardless of the length of time shares are held.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

©2019 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

More Alternative Investments Topics >