Schwab Sector Views: Coronavirus Changes Our Views

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSchwab Sector Views is our three- to six-month outlook for 11 stock sectors, which represent broad sectors of the economy. It is designed for investors looking for tactical ideas. We typically update our views every month.

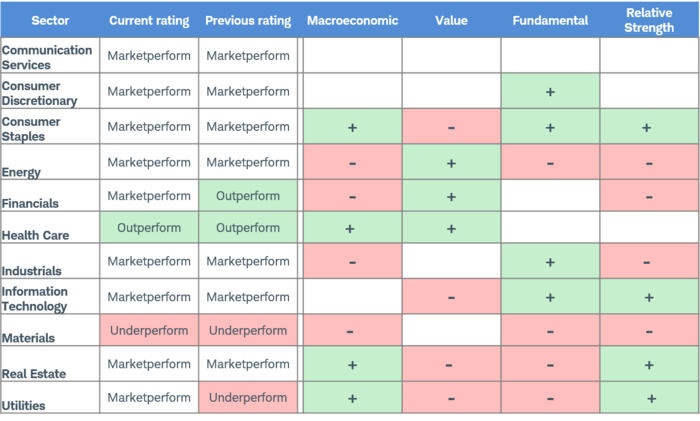

In light of recent events, we’re changing our ratings on certain equity sectors—specifically, we’re downgrading Financials and upgrading Utilities. Here are our current ratings and our views of the sectors’ underlying fundamentals.

Sector overview

Note: Each of the sector lenses shown above—Macroeconomic, Value, Fundamental and Relative Strength—is both intuitive and evidenced-based in nature. Within each, there are a varying number of factors. The Macroeconomic lens includes sector sensitivities to interest rates, stocks and the value of the U.S. dollar; the outlook for each of these is determined by the Schwab Center for Financial Research (SCFR)’s Asset Allocation Working Group, which uses a mosaic approach of quantitative and qualitative considerations. Value includes six different valuation metrics that provide a holistic perspective on current valuations relative to each of the sectors’ own historical valuations, as well as relative to the other sectors. Fundamental provides insight as to how efficiently the companies within each sector use invested capital to produce earnings; this historically has been informative as to future relative performance of the sectors. Finally, Relative Strength measures momentum of the individual sectors against all of the other sectors. We also consider the data in the context of factors outside the scope of these indicators—for example, geopolitical risk or central bank policy changes.

Source: Charles Schwab, as of 3/4/2020

Why the change in our sector views?

Last month, we wrote that the coronavirus outbreak and the Democratic primary had created uncertainty that was beginning to affect certain equity sectors. At that point, we were monitoring the situation, but hadn’t changed our sector calls.

Well, things have changed—quickly. As the COVID-19 virus has spread around the world, including to the U.S., the market impact has become more pronounced. We’re seeing signs that the direct impact on supply chains out of China is having an increasing influence on U.S. company earnings. Many industries also are showing signs that demand has been affected.

Governments and central banks are reacting, but there’s only so much they can do to fix global supply chains or keep consumers spending. Central banks in China, Australia and Mexico have cut interest rates recently, while targeted fiscal measures have been announced in countries including Italy and Hong Kong. The Federal Reserve on March 3rd cut the benchmark federal funds rate by a half-percentage point, citing “evolving risks” to the U.S. economy related to the coronavirus. The S&P 500 index rose briefly on the rate cut, but then pulled back sharply amid fears that the Fed knows something more than investors as a whole. While we don’t know whether that’s the case, we do know that more liquidity in the financial markets is better than less during time of stressed financial conditions.

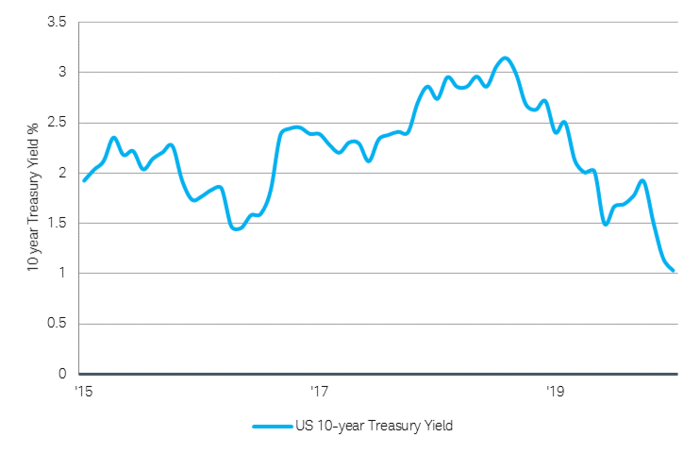

Given the highly uncertain environment, it’s impossible to know whether the injection of liquidity will be enough to prop up stocks this time, as it has several times in this nearly 11-year bull market. However, we have more conviction on the potential impact on interest rates, which we believe will continue to come under pressure in the near term.

The 10-year Treasury bond yield has dropped sharply

Source: Schwab Center for Financial Research, Bloomberg, as of 03/04/2020.

Downgrading Financials

This brings us to our first sector rating change—downgrading Financials to marketperform from outperform.

Some background: Interest rates have been a major driving force for many sectors, particularly Financials, Utilities and Real Estate (which comprises real estate investment trusts, or REITs).

When long-term interest rates fall, the Financials sector tends to underperform the broader market. This is partly because banks and financial services companies typically borrow at short-term rates and lend at longer-term rates, so lower long-term rates can affect revenue. Also, lower long-term interest rates often occur during periods of general economic slowdown, which usually leads to lower loan demand from consumers and businesses.

Meanwhile, Real Estate and Utilities sectors typically outperform—in the first case, because REITs are relatively heavy borrowers, and in the latter case because Utilities tend to pay relatively high dividends, which investors find especially attractive when interest rates are low.

At the start of 2020, investors were hopeful amid signs of global economic stabilization, which suggested ongoing strength in the U.S. economy and continued consumer lending. At the time, the yield curve was steepening, as long-term rates were rising faster than short-term rates. This was a tailwind for banks.

However, the coronavirus epidemic changed all of that, and there is now a risk that the secondary impact could imperil not only the global economy, but also the stalwart U.S. economy. The surprise drop in short-term rates—along with a downward shift along the entire yield curve—already has taken a toll on financial stocks. While a near-term bounce would not be surprising, over the longer term we think a continued fall in rates will remain a headwind for Financials, and that would argue for an underperform rating. That said, even with an expected decline in earnings growth, we believe that attractive relative valuations could offset some of the negative impact from falling yields.

Taken all together, we have decided to downgrade the financial sector to marketperform.

Upgrading Utilities

Consistent with our evolving view on rates, we are upgrading rating on the Utilities sector from underperform to marketperform. The lower-rate environment has drawn investors to the sector’s typically stable earnings and higher dividend yields. However, we’re holding off on a full move to outperform, despite expected continued support from lower rates, because of the sector’s high valuations. This may be in part why Utilities didn’t provide much cushion during February’s sharp sell-off, when it declined by about the same degree as the overall market despite its historically low correlation1 to the broader S&P 500 index.

Health Care: Still at outperform

Meanwhile, we’re maintaining our outperform rating on Health Care. The upcoming U.S. presidential election has increased risk for the sector, amid calls for pharmaceutical pricing controls and a single-payer health-care system. However, the former is likely already priced in, as it has some bipartisan support. Single payer proposals have been a hot topic among Democratic primary candidates, but we believe a Democratic sweep of the White House and both houses of Congress is unlikely—and even if it were to occur, there currently isn’t broad-based support for a single-payer system even within the Democratic Party. That said, we’re still seeing swings in the relative performance of the Health Care sector consistent with the spread between polling numbers for moderate versus liberal Democratic primary candidates.

Additionally, the sector does sport very attractive relative valuations and solid fundamentals, which has helped it maintain its more non-cyclical properties amid the heightened volatility.

Materials: Still likely to underperform

We are also maintaining our underperform view on the Materials sector. While we think the U.S. dollar could continue to come under pressure as interest rates fall relative to other developed international rates, the dollar’s safe-haven status likely will stem any significant decline. A weaker dollar can support commodity prices, underpinning mining companies. However, declining global demand for chemicals and metals is likely to more than offset modest dollar weakness. Adding below-average valuations, poor fundamentals and negative relative momentum to the mix only reinforces our underperform rating.

Watching the virus’ impact on earnings

Analysts have been cutting earnings forecast for many industries, as a growing number of companies have issued cautionary statements about the impact that COVID-19 may have on their revenues. This could affect relative valuations of the various sectors, and we are closely monitoring these rapidly shifting developments.

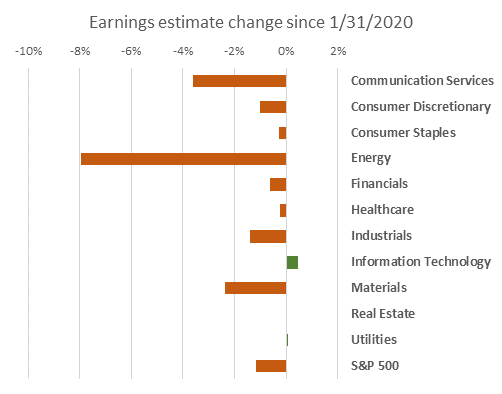

Since January 31, consensus 2020 earnings estimates have been cut in most sectors

Source: Schwab Center for Financial Research, Bloomberg. Reflects change in analyst consensus 2020 earnings estimates since 01/31/2020. Data as of 3/04/2020.

Some of the more globally focused sectors, such as Consumer Discretionary, Information Technology and Industrials, have cited coronavirus as a potential impact to earnings. The warnings by Consumer Discretionary and Consumer Staples companies suggest that coronavirus is becoming a broader demand issue, potentially affecting consumer spending.

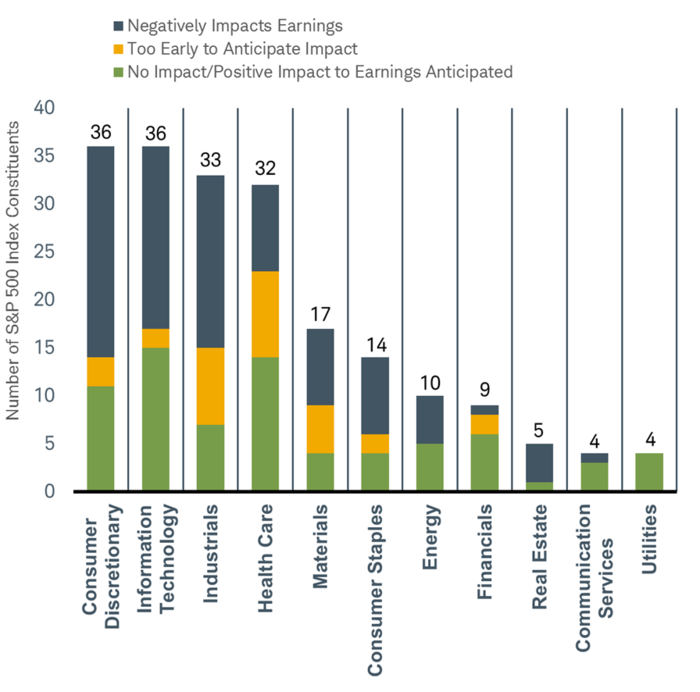

A number of companies have mentioned coronavirus as a potential impact to earnings

Source: Schwab Center for Financial Research, FactSet. Number of mentions and characterization of the impact from COVID-19 in company press releases by sector, as of 03/04/2020.

A final word

Keep in mind that no matter what our view is on any of the sectors, remaining diversified is very important. Concentrating in too few sectors can dramatically affect the risk profile and performance of your portfolio. So if you do make any sector tilts in your portfolio, keeping them small is a good way to maintain appropriate diversification and potentially enhance the performance of your portfolio.

1 Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated.

Schwab Sector Views: Our current outlook

|

Sector |

Schwab Sector View |

Date of last change to Schwab Sector View |

Share of the |

Year-to-date total return as of 03/05/2020 |

|---|---|---|---|---|

| Communication Services | Marketperform | 01/23/2020 | 10.7% | -5.58% |

|

Marketperform |

07/17/2014 |

9.9% |

-6.37% |

|

|

Marketperform |

05/07/2015 |

7.2% |

-1.18% |

|

|

Marketperform |

11/20/2014 |

3.6% |

-25.31% |

|

|

Marketperform |

03/05/2020 |

12.2% |

-14.15% |

|

|

Outperform |

01/26/2017 |

14.0% |

-4.20% |

|

|

Marketperform |

01/29/2015 |

8.9% |

-10.36% |

|

|

Marketperform |

08/16/2018 |

24.4% |

-1.04% |

|

|

Underperform |

01/23/2020 |

2.5% |

-10.43% |

|

|

Marketperform |

08/16/2018 |

3.1% |

1.25% |

|

|

Marketperform |

03/05/2020 |

3.5% |

4.58% | |

|

S&P 500 index |

-6.08% |

Source: Schwab Center for Financial Research, Bloomberg (for YTD total returns) and S&P Dow Jones Indices (for S&P 500 sector weightings). Sector performance data is based on total return for each S&P 500 sector subindex (see “Important Disclosures” for index definitions). Sector weighting data is as of 2/28/2020; data is rounded to the nearest tenth of a percent, so the aggregate weights for the index may not equal 100%.

Past performance is no guarantee of future results.

What do the ratings mean?

The sectors we analyze are from the widely recognized Global Industry Classification Standard (GICS®) groupings. After a review of risks and opportunities, we give each stock sector one of the following ratings:

- Outperform: likely to perform better than the broader stock market*

- Underperform: likely to perform worse than the broader stock market

- Marketperform: likely to track the broader stock market

*As represented by the S&P 500 index

How should I use Schwab Sector Views?

Investors should generally be well-diversified across all stock market sectors. You can use the Standard & Poor's 500® Index allocations to each sector, listed in the chart above, as a guideline.

Investors who want to make tactical shifts in their portfolios can use Schwab Sector Views' outperform, underperform and marketperform ratings as a resource. These ratings can be helpful in evaluating and monitoring the domestic equity portion of your portfolio.

Schwab Sector Views can also be useful in identifying stocks by sector for potential purchase or sale. Schwab clients can use the Portfolio Checkup tool to help them review and manage their sector allocations. When it's time to make adjustments, clients can use the Stock Screener or Mutual Fund Screener to help identify buy or sell candidates in particular sectors. Schwab Equity Ratings also can provide an objective and powerful approach for helping you select and monitor stocks.

Important Disclosures:

Schwab Sector Views do not represent a personalized recommendation of a particular investment strategy to you. You should not buy or sell an investment without first considering whether it is appropriate for you and your portfolio. Additionally, you should review and consider any recent market news. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to change without notice in reaction to shifting market or other conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and asset allocation do not ensure a profit and do not protect against losses in declining markets.

Market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Risks of the REITs are similar to those associated with direct ownership of real estate, such as changes in real estate values and property taxes, interest rates, cash flow of underlying real estate assets, supply and demand, and the management skill and credit worthiness of the issuer.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

The Schwab Center for Financial Research (SCFR) is a division of Charles Schwab & Co., Inc.

(0320-0UY5)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All