Schwab Market Perspective: Coronavirus Hits Markets Hard

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsStocks have plummeted this month as investors struggled to assess what impact the COVID-19 coronavirus may have on the economy. A U.S. recession is looking increasingly likely, although it’s not clear how deep or long-lasting it might be—if it happens. As of Thursday’s (March 12th) close, the S&P 500 was down 26.7% from its recent peak, firmly putting stocks in a bear market (generally defined as a drop of 20% or more).

The number of new COVID-19 cases has continued to rise outside mainland China, prompting some countries to embrace ever-stricter containment efforts—Italy, for example, imposed a nationwide lockdown this past week. In the U.S., authorities in some communities have urged residents to avoid crowded areas, work remotely, self-quarantine, and other measures aimed at containing the virus—all of which could reduce demand in many industries, starting with travel, hospitality and leisure.

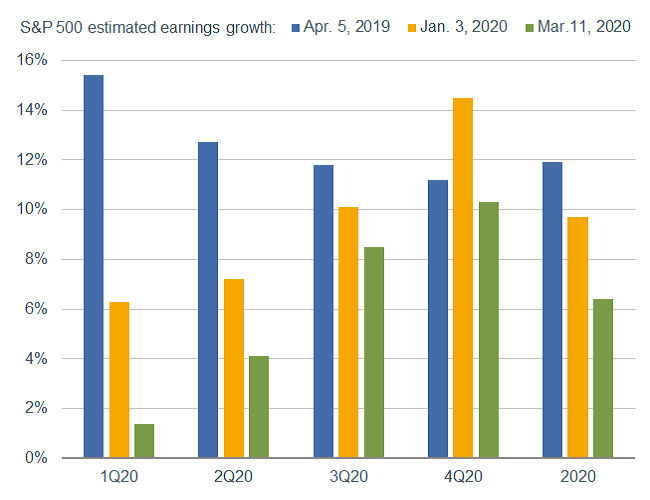

This has already pressured not only current share prices, but also companies’ future earnings guidance. You can see from the chart below that consensus estimates for growth this year have been reduced.

Estimated earnings growth has been cut

Source: Charles Schwab, I/B/E/S data from Refinitiv, as of 03/11/2020.

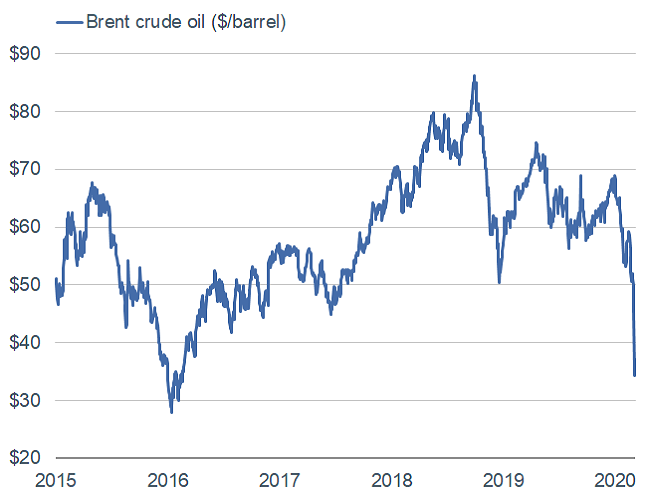

Meanwhile, crude oil prices dropped sharply this past week after Saudi Arabia cut its official oil price and boosted production, a move that will flood the market with cheap oil. Brent crude prices tumbled on the news, as you can see in the chart below.

Brent crude oil prices tumbled after Saudi Arabia cut prices and raised production

Source: Charles Schwab, Bloomberg, as of 3/11/2020.

The oil price decline poses a major threat to the energy industry. Earnings estimates for energy companies—as well as jobs—may be cut, despite the benefit to consumers at the gasoline pump. Also worth noting: Even though the sector holds a relatively small (3%) weighting in the S&P 500 index, energy companies issue a significant amount of debt, and the sector is a much bigger 11%-12% of the high-yield (or “junk”) bond market. Should the plunge in oil prices continue, many companies will not be able to service their debt, likely causing corporate bond downgrades and defaults that could further weigh on the market and economy.

Because of all the unknowns, corporate management and Wall Street analysts’ lenses are just as blurry as everyone else’s. Many companies have simply withdrawn full-year guidance altogether. With both the “E” (earnings) and the “P” (price) in the price-to-earnings (P/E) ratio both dropping, assessing stocks’ valuations has become nearly impossible.

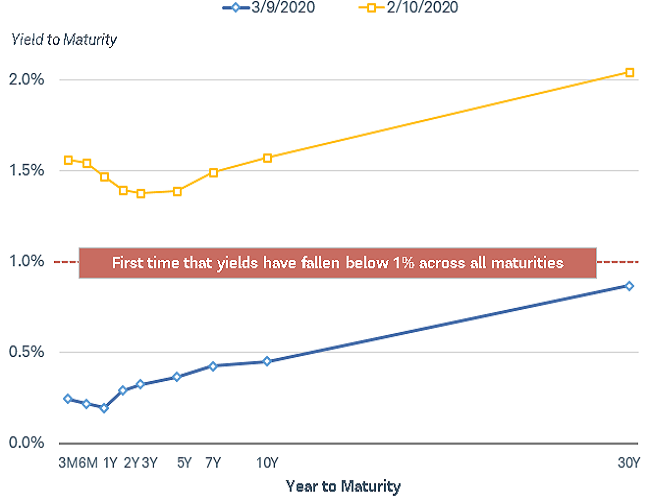

Treasury yields have fallen to record lows

Treasury yields have continued to plumb lower as investors seek a safe haven. Yields for all U.S. Treasuries on March 9th dipped below 1%—an unprecedented level—and have stabilized since.

The Treasury yield curve earlier this week, versus one month prior

Source: Bloomberg, data as of 3/9/2020 and 2/10/2020. Past performance is no guarantee of future results.

We expect central banks and governments to step up efforts to cushion the potential economic blow. The Federal Reserve already cut its benchmark short-term interest rate, the federal funds rate target, by a half-percentage point on March 3rd. However, it is likely to reduce the rate even further—perhaps down to zero—over the next few months.

The Fed may also increase the amount of liquidity in the financial system by encouraging foreign banks to use swap lines to make sure there is an ample supply of dollars, possibly while also increasing its holdings of short-term Treasury bills to provide liquidity to the domestic markets (by buying Treasury securities, the Fed injects cash into markets). These steps can help keep the financial system functioning. If the economy goes into a decline, it would not be surprising to see the Fed restart its quantitative easing program, buying longer-duration bonds.

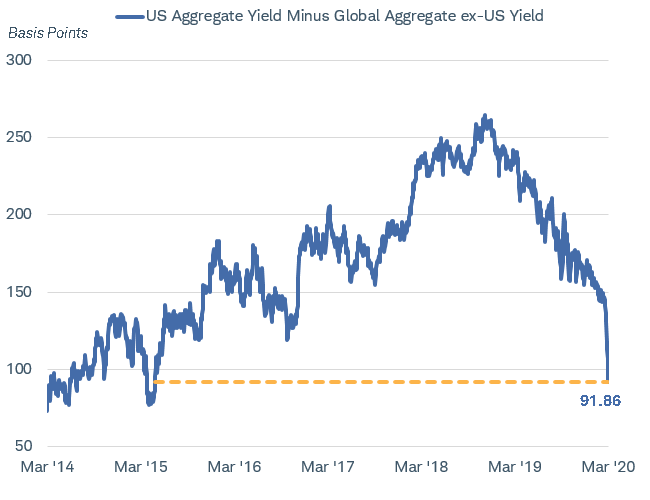

However, yields may continue to fall. Compared to other major countries, U.S. Treasury yields are still relatively high.

The yield difference between U.S. bonds and global bonds is at its lowest level since mid-2015

Source: Bloomberg, using daily data as of 3/6/2020. U.S. bond yield is represented by the yield on the Bloomberg Barclays U.S. Aggregate Bond Index, and global bond yield is represented by the yield on the Bloomberg Barclays Global Aggregate ex-U.S. Bond Index.

These steps can help mitigate the impact of the expected downturn in the economy this year, but central banks can only do so much. Government intervention in the form of tax cuts and targeted lending to hard-hit industries may also be needed.

Global recession risk has risen

Although it’s possible we are entering a global recession, it’s too early to predict the magnitude. In response to the threat posed by COVID-19, the Organization for Economic Cooperation and Development (OECD) lowered its global gross domestic product (GDP) growth forecast recently by a half percentage point, to 2.4% for 2020. Generally speaking, global growth below 2.5% is recessionary.

However, the OECD seems to have anticipated only a temporary hit to global growth. It raised its 2021 outlook by 0.3%, with a forecasted rebound beginning in the second half of 2020 and extending into next year (for how this recession compares to the 2008-09 global financial crisis, read: Q&A on COVID-19: The Economy, Markets and What Investors Should Do).

Any rebound in global economic activity could be helped by a flood of fiscal and monetary stimulus. Central banks in the U.S., China, Australia, and Mexico have already cut interest rates. Fiscal stimulus has been added in Italy, Japan, South Korea, and the U.S. More is likely on the way.

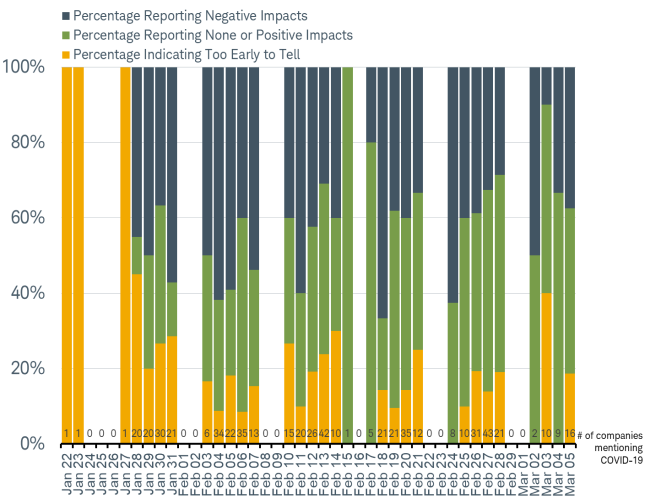

We have little data so far to gauge the size of the virus’s economic impact, given the short amount of time since the start of the outbreak, as well as the lags in measurement and reporting of economic data. However, we have heard from a lot of companies on the potential impact to earnings. Hundreds have mentioned the impact of the coronavirus in communications with investors since January 20th, when the World Health Organization (WHO) began to track cases of the virus.

Initially, the comments by business leaders were primarily that it was too early to tell what the impact on earnings may be. As time has gone on, those comments have been increasingly replaced by downward or upward guidance, as you can see in the chart below.

Business leaders on the coronavirus impact on earnings by day

Source: Charles Schwab, FactSet. Number of mentions and characterization of the impact from COVID-19 in company press releases, as of 03/06/2020.

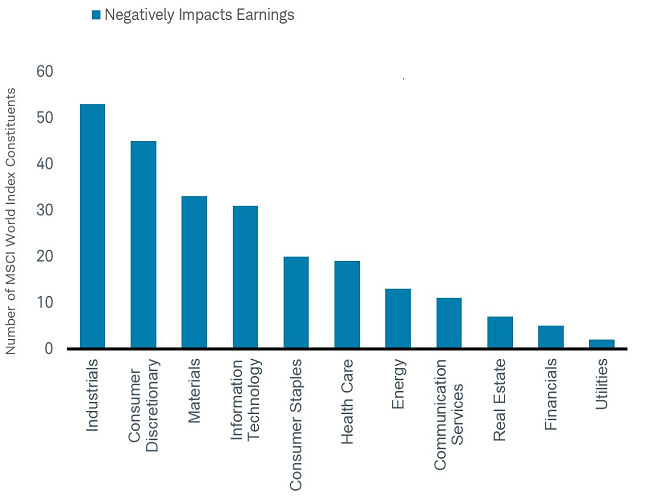

While those issuing downward earnings guidance outnumber those raising estimates, it is noteworthy that not all impact has been negative. Downward guidance has been concentrated in the sectors with supply chains linked to Asia: Industrials, Consumer Discretionary, Materials and Information Technology. The Financials and Energy sectors also may begin to see increasing downward guidance, following the Fed rate cut and the plunge in oil prices.

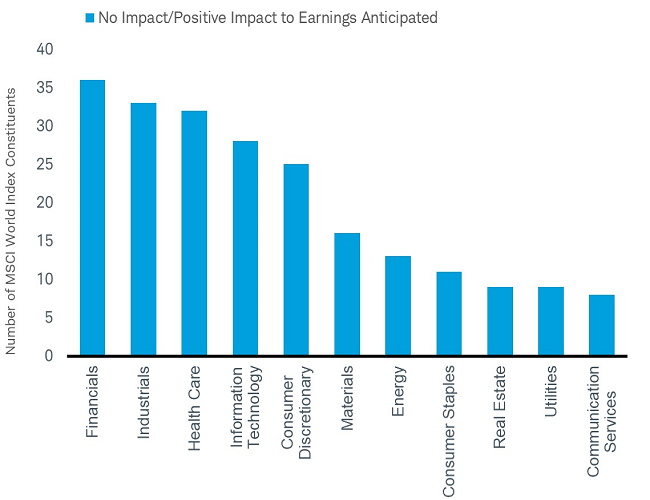

Meanwhile, the number of companies citing a positive impact on earnings, or citing no material impact at all (which seems like a positive in this environment), has been highest in the Health Care, Industrials and Financials sectors—although the latter may soon see more downward revisions, as noted above.

Companies issuing downward earnings guidance in response to COVID-19

Source: Charles Schwab, FactSet. Number of mentions and characterization of the impact from COVID-19 in company press releases by sector, as of 03/06/2020.

Companies issuing positive earnings guidance or citing no impact in response to COVID-19

Source: Charles Schwab, FactSet. Number of mentions and characterization of the impact from COVID-19 in company press releases by sector, as of 03/06/2020.

What to do

There is no one-size-fits-all answer for how to respond to an event such as coronavirus. If you’re a younger investor who is saving and investing for a distant goal, such as retirement, the best action to take may be no action at all. If you’ve built a portfolio that matches your time horizon and risk tolerance, and you don’t expect to need money from it anytime soon, it’s usually best to stick to the investing plan you developed when markets were calm.

We continue to recommend appropriate portfolio diversification among various asset classes, including stocks and bonds. It’s also a good idea to rebalance your portfolio periodically, to bring it back to your original asset allocation targets (Schwab clients can log in to their accounts and use the Schwab Portfolio Checkup tool to check whether their asset allocation has drifted away from original targets).

However, if you’re in a position where you must sell stocks—for instance, if you’re retired and relying on your portfolio to fund your lifestyle right now—there are steps you can take to minimize the negative impact of selling in a down market, including rebalancing and tax-loss harvesting.

Meanwhile, if you’re nearing retirement, having a financial plan is more important than ever. It’s vital at this stage to understand how much risk you can stomach, both emotionally and financially, in any market environment.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Diversification, asset allocation and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0320-0ECZ)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All