Crisis Dashboard: Big Data Helps Paint the Big Picture

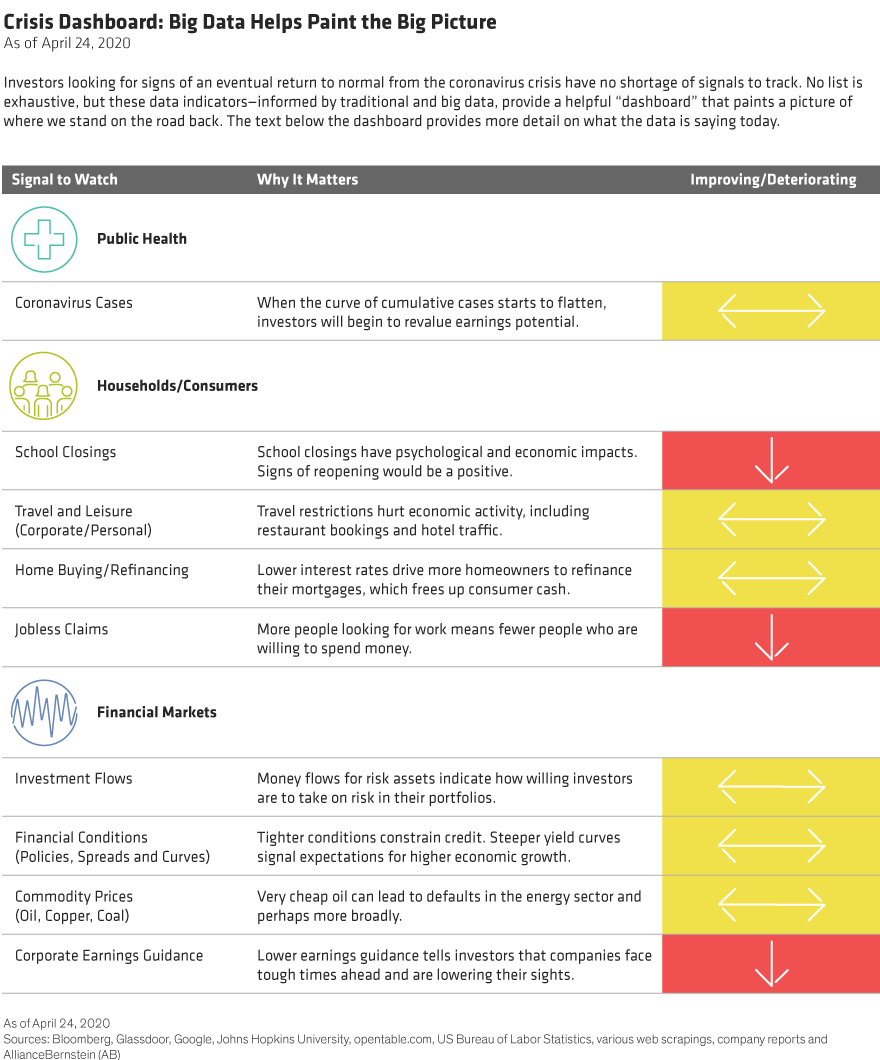

Our crisis dashboard includes signals from three areas: 1) public health, 2) the consumer sector and 3) financial markets. By pulling big data from traditional sources (earnings growth and GDP, for example) and nontraditional sources (Google Trends and Glassdoor), we can create a better mosaic of the road back. Public health is key: until there’s a vaccine, the cascading impact of the virus may continue.

The dashboard color codes (red, yellow or green) indicate the current state of each signal, while the arrows indicate the trend (improving, deteriorating or static).

We’ll continue to update this data as we move forward. Here’s the latest.

Public Health

Globally, the number of coronavirus cases continues to rise—it’s currently about 2.5 million. Cases are still rising in the US, especially in a number of hot spots, but the increase is decelerating. We’re seeing improvement in Europe and Asia. The R0, which tracks the number of cases spread by one person, is declining, and case estimates from Johns Hopkins University are slowing.

Households/Consumers

School Closings: More schools globally have shut their doors, and closings could last longer than expected. This includes closures for the rest of the current school year.

Travel and Leisure: Travel restrictions are widespread, but we’re not necessarily seeing wholesale lockdowns. Open tables are commonplace at restaurants, and subway ridership is still at all-time lows. Google search trends for “vacation idea” have dropped everywhere except Asia.

Home Buying/Refinancing: Declines in interest rates have created a surge in mortgage refinancing activity. While refinancing activity remains weak, it is showing signs of improvement.

Jobless Claims: US jobless claims are skyrocketing: more than 26 million have been filed. Nearly 60 million jobs across the European Union and UK are at risk. Unemployment rates across the Asia-Pacific region could rise by well over three percentage points—twice as high as during the average recession. Credit card spending data is still pointing to major weakness due to business closures.

Financial Markets

Investment Flows: Globally, massive outflows continue from all risk assets, with only money funds and cash benefiting. We’re starting to see some money flow back into “risk assets” this week.

Financial Conditions: Despite sizable rescue packages, conditions still seem tight. Credit spreads are above average, but have pulled back from their highs. A rise in defaults is certainly coming. If the yield curve continues to steepen, it would be viewed positively.

Commodity Prices: West Texas Intermediate and Brent oil prices both fell significantly (and are negative in some spots), but copper prices are slowly rebounding from their lows. Coal consumption in China is slowly picking up again.

Corporate Earnings Guidance: Global earnings are being revised much lower, (another 140+ S&P companies are reporting this week). Glassdoor trends in employee attitudes highlight a disparity between companies that prepared well for work-from-home scenarios and those that didn’t.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.