The COVID-19 shutdown has prompted an unprecedented number of US companies to suspend earnings guidance. Equity investors should focus fundamental research on a wider range of outcomes instead of the overly precise game of predicting short-term estimates—especially during a period of heightened uncertainty.

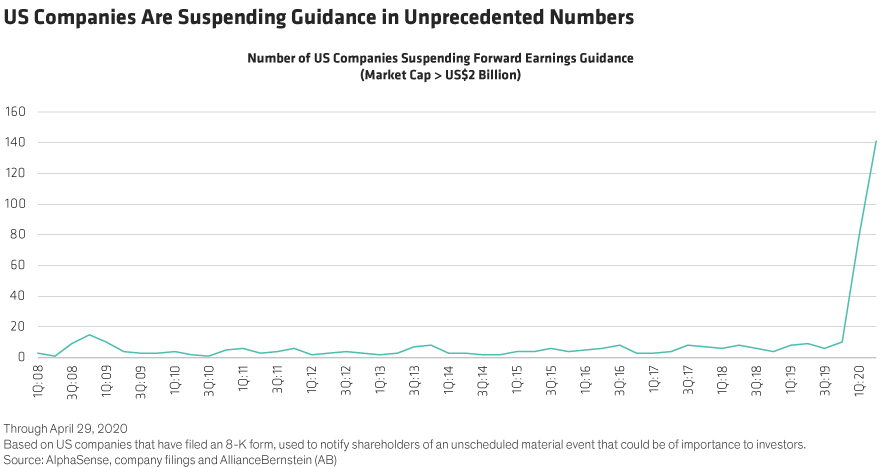

Companies are withdrawing guidance on a massive scale as the first-quarter earnings season unfolds. By April 29, 141 US companies with market capitalizations greater than $2 billion had suspended guidance (Display), way beyond anything seen in the worst moments of the global financial crisis. Visibility of business conditions has never been hazier across every sector and industry.

This creates a problem for many market participants. It’s common practice for investors to ground their profit forecasts with company guidance, which tends to anchor their evaluation horizon to shorter-term periods. While investors often talk about focusing on the long term, earnings expectations models typically are calibrated for the next quarter through the current fiscal year.

These models strive for precision with incredible detail. Why? Given the regularity of quarterly earnings, perhaps projections with such short feedback loops provide a sense of control and precision regarding the investment outcome. Regardless of the motivations, companies play into this endeavor by setting guidance they aim to meet and even exceed; how else can you explain that 70% of US companies have beaten quarterly expectations on average since the second quarter of 2013, according to our research. Companies with visibility into their near-term operations feed the predictability of sell-side and buy-side expectations.

Short-Term Projections Have Been Shattered

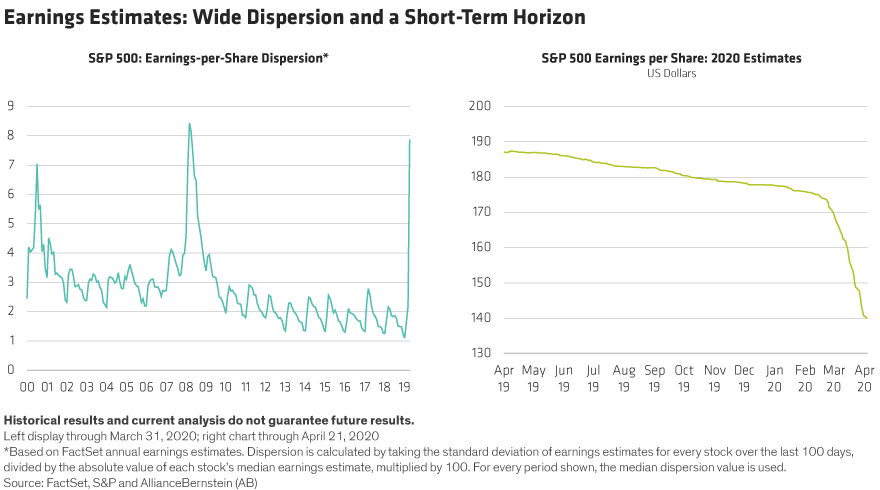

Today, the pretense of precision is gone. While earnings consistency usually breaks down in recessions, the exogenous shock of the coronavirus—and the scale of the fallout—has shattered any attempt to predict the near future. Since the extent of current guidance withdrawals is so broad, we anticipate an even greater dispersion of earnings expectations than we have already witnessed (Display below, left).

Even if we had more certainty about the near-term outlook, we think relying on short-term measures like next quarter’s earnings per share (EPS) provides false assurance. In fact, measuring a company’s profit potential with only a single point estimate is arbitrary, in our view.

Rethinking Approaches to Earnings Forecasts

This chaotic moment provides a good opportunity to take a step back and reevaluate the efficacy of forecasting EPS and valuing stocks based on price/earnings (P/E) ratios. Even with today’s market conditions, estimation error isn’t the only problem. Because even if we could forecast the S&P 500’s 2020 EPS, any reasonable investor would argue that this year’s profits (Display above, right) aren’t representative of the market’s long-term potential and should be normalized. In other words, the accuracy of estimates doesn’t prove their validity.

Nobody can say whether 2021 will be normal. However, shifting out the forecast horizon by several years reduces near-term variability and noise. It also anchors your perception of the worth of a business to its long-term fundamental success. We believe that it’s more appropriate to ground evaluation scenarios by assessing a company’s profit potential over the next 10 years.

Precisely Imprecise: Modeling Certainty to Cope with Uncertainty

Of course, this approach raises other uncertainties. Long-term investors shouldn’t pretend to be precise. Given the inherent unknowns over such a distant horizon, we think several probable paths of asset growth and profitability should be explored to underpin valuation estimates—in both good and bad times. This exercise not only informs a company’s ultimate profit potential but provides insight into the drivers of today’s profit model that must be rigorously monitored.

That doesn’t mean investors should ignore current operating performance and challenges. However, it means that investors don’t need to accurately forecast near-term results to maintain a fundamental thesis and confidence.

By looking further into the future, investors gain latitude to act differently amid heightened uncertainty. Greater dispersion in EPS is bound to create greater volatility, especially when many companies are suspending guidance or offering projections of questionable validity. These are great conditions for stock pickers. When short-term-minded investors panic and run for the lifeboats, long-term active investors can step in, taking advantage of the weakness as buyers of attractively valued long-term assets with return potential rooted in real businesses rather than spurious expectations.

Frank Caruso is Chief Investment Officer of US Growth Equities at AB

John Fogarty is Portfolio Manager of US Growth Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein L.P.

© AllianceBernstein

More Volatility/Downside Protection Topics >