Small-cap stocks were hit harder than large-caps in the coronavirus sell-off. But given the extreme market dislocations, select smaller companies with innovative advantages could offer investors a surprising source of diversification for the uncertain times ahead.

Investors in small-cap stocks have had a particularly rough ride since the pandemic began. Even after recovering from a late-March trough, the Russell 2000 Index of US small-cap stocks was down 24% since the beginning of the year through May 15, while the Russell 1000 Index of US large-cap stocks has fallen by 11%. When investors panic, they shun smaller stocks, which are widely perceived as riskier than are larger peers.

Are Smaller Stocks Really Riskier?

But is the perception accurate? Not necessarily. Smaller companies are considered riskier because they are believed to have less funding access, financial stability and managerial depth than are larger firms. They’re often seen as less diversified, which can make revenues vulnerable in a downturn. And about 25% of Russell 2000 companies aren’t profitable, versus 6% of Russell 1000 companies (Display, left).

Yet many smaller companies don’t fit the stereotype. In fact, US small-caps have lower debt levels than US large-caps (Display above, right). Smaller companies often have access to venture capital and convertible debt funding—even in a crunch. In many cases, smaller companies are unprofitable by choice because they’re investing in research and development (R&D) to fuel future growth. For example, early-stage biotech companies make up 13% of the Russell 2000 and account for most of the unprofitable companies in the benchmark; many have no revenues or earnings because they’re focused exclusively on developing new therapeutics for future growth.

These characteristics have prevailed in market recoveries. While small-caps are often hit harder in downturns, such as the dot-com bubble or the global financial crisis, they tend to outperform large-caps in a rebound (Display). It’s too soon to say what will happen in the coronavirus recovery. Still, small-caps outperformed large-caps slightly in April as US markets bounced back from the trough.

Even before the current crisis, investors weren’t enthused by small-caps. In fact, the Russell 2000 has trailed the Russell 1000 for the past five years. The continued underperformance is creating opportunities in smaller stocks that have been unjustifiably punished in the recent downturn.

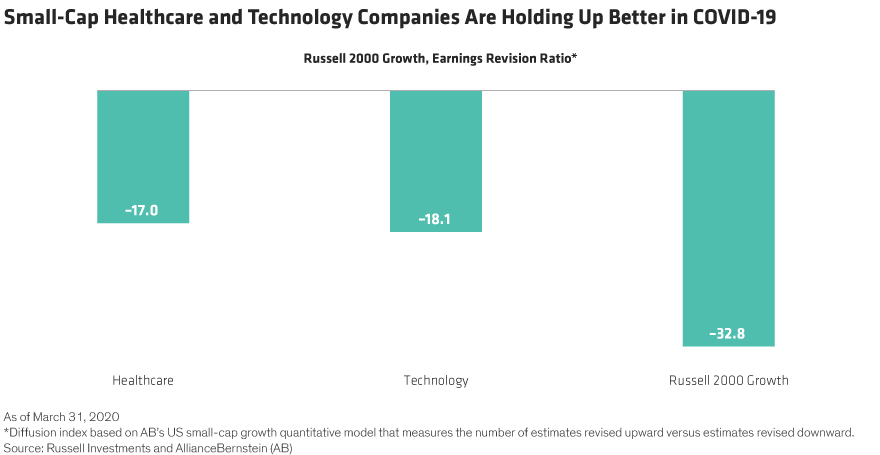

Innovation Can Make the Difference

Companies with an innovative edge deserve particular attention. Their advantages may be overlooked because smaller companies often are not understood by the market. Most aren’t household names, and small-caps typically get much less analyst coverage than do larger-cap peers. So it’s easy to miss a minnow that’s poised to take market share from large incumbents that are slow to react to new competition.

Innovative businesses also have better shock absorbers for a recession. Since they generally don’t depend on macroeconomic growth to begin with, they’re more resistant to economic downturns, in our view. Indeed, our research indicates that earnings estimates for small-cap healthcare and technology companies, which tend to have strong innovation profiles, have held up much better than the broader market; a much smaller percentage of these sectors have revised down earnings versus the broader growth benchmark (Display). As the recession bites, we think investors should look for companies with truly innovative products, services or business models.

R&D spending is a good indicator of innovation. By searching for companies that invest a high percentage of their revenues on R&D, investors can identify innovative businesses in industries that can maintain resilient revenues to generate growth through a tough environment.

Technology and healthcare are fertile ground for smaller companies with big ideas. For example, the acceleration of remote-working trends is speeding up the migration of IT infrastructure to the cloud. That’s good news for companies like Five9, a small-cap software outfit, which enables remote call centers. In healthcare, patients are increasingly consulting doctors remotely to avoid medical clinics and hospitals. Teladoc, which provides remote medical services, is emphasizing the benefits of virtual healthcare in the COVID-19 crisis. In other sectors, innovative retailers like Wayfair, an online furniture outlet, are well placed for an era of social distancing as consumers stay away from stores.

Looking Beyond Near-Term Earnings

For many innovators, we believe the long-term earnings potential hasn’t changed, even if near-term visibility is cloudier than usual. As a result, today’s valuations should be assessed relative to long-term earnings power. Before the crisis, growth stocks seemed relatively expensive. Now, with share prices beaten down, investors who develop fundamental projections that look beyond the crisis can identify attractively valued small-cap stocks.

Valuations are also attractive in today’s low-interest-rate environment. Since small-cap growth companies tend to generate cash flows in the more distant future, lower discount rates make the valuation of those cash-flow streams more attractive today and point to stronger returns tomorrow. As a recovery unfolds, we believe investors will eventually gain comfort in the ability of companies that don’t depend on a macroeconomic growth to deliver stronger cash revenue and earnings growth than more cyclical peers.

Capturing Pent-Up Potential

Finding innovative smaller companies in a thorny market and macro environment is no easy task. Investors who seek to capture the small-cap opportunity through a passive portfolio will be buying every name in the index—including companies experiencing severe business challenges that may persist beyond the crisis. Active managers can sift out select companies that will potentially come out from this downturn even stronger and more resilient.

The recent weakness of smaller stocks isn’t surprising. In a risk-off market, indiscriminate selling often fuels share price volatility that’s disconnected from underlying company fundamentals. But these conditions are also creating opportunities for investors to capture the pent-up potential of innovative smaller companies to disrupt businesses, benefit from evolving sources of demand and deliver outsize returns in a challenging market.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

Samantha S. Lau is Co-Chief Investment Officer of Small and SMID Cap Growth Equities

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein