As fixed-income markets have started to recover following the massive selloff and liquidity crunch in March, credit risk-transfer securities (CRTs)―agency mortgage securities not guaranteed by Fannie Mae and Freddie Mac―have been slower to do so. Investors are wondering: Where do CRTs go from here?

To answer this question, we believe it’s important to look at the reasons for CRTs’ larger underperformance in March. Initially, the drawdown was driven by concerns about housing-market fundamentals, as investors feared that unemployment caused by the economic lockdown to slow the spread of COVID-19 would lead to a spike in mortgage delinquencies and defaults.

The selloff was exacerbated by the fact that many investors—such as mortgage REITs and hedge funds—who were attracted by CRTs’ strong underlying quality had levered their exposure. As bond prices fell and the repo markets came under pressure, these investors became subject to margin calls, forcing them to sell. This created a perfect storm for CRTs.

While CRT prices have started to recover, spreads are still multiple times their pre-crisis levels, more than compensating investors for increased risk associated with COVID-19. The current environment is certain to impact many of the mortgage borrowers and to increase the credit risk in the underlying mortgage pools. However, there are many reasons why we continue to favour this sector. In fact, CRTs continue to offer solid fundamentals at a time when corporate credit metrics look stretched.

Before diving deeper into the fundamental picture, it is helpful to understand how CRTs are structured.

WHAT ARE CRTs

CRTs are typically issued by government-sponsored housing agencies Fannie Mae and Freddie Mac. Like typical agency bonds, CRTs pool thousands of different mortgages into a single security, and investors receive regular payments based on the performance of the underlying loans. But there’s a key difference: CRTs carry no government guarantee. Investors could absorb losses if a large number of the loans default.

CRTs are issued in tranches. Lower-tiered bonds absorb losses first, followed by higher-rated tranches if losses are more severe (with the most senior tranches receiving prepayments first). GSEs retain a share of the risk for each security they issue—that’s why the securities are referred to as risk-sharing bonds.

The underlying mortgages are the same ones included in the agency mortgage pass-through pools, with strong-credit borrowers that conform to the GSE’s standards.

HOUSING MARKET IS ON SOLID FOOTING

One of the key fundamentals supporting our outlook for CRTs is that the underwriting standards are much higher than those that prevailed before 2008. For example, most borrowers in CRT pools have FICO scores above 750. At the peak of the housing boom, there was a much higher preponderance of borrowers in the 600‒700 bracket. FICO scores are borrower credit-risk scores that range from 300 to 850, with scores above 650 indicating a very good credit history.

Another positive effect flowing from the improved underwriting standards has been the sharp drop in risk-layering, which is the inclusion of multiple high-risk metrics―such as poor loan-to-value ratios together with low FICO scores and high debt-to-income ratios―in individual loans.

The practice was responsible for the large credit losses on many underlying loans in non-agency securities during the housing crisis. CRTs typically do not layer risk, and the decline in the practice has helped to improve the quality of the overall market of which CRTs are a part.

Finally, the housing market today is supported by very strong technicals. Compared to the state of the housing market before the 2008 crash, inventory levels today are very tight (Display), as we have not seen speculative building.

This coincides with demand from, for example, millennials who are starting families. Demand for homes is quickly reverting to pre-COVID levels as measured by rising purchase mortgage applications. That’s part of the reason why home prices have held up well recently and even increased in some instances amid the pandemic. While we expect home prices to decline by 5%–10% as the recession continues, larger price movement is unlikely due to these favorable technicals.

ACTIONS BY POLICYMAKERS SHOULD LIMIT POTENTIAL DEFAULTS

Government actions and low interest rates are also helping to reduce default risk.

Under the CARES Act signed into law in March, borrowers facing economic hardship as a result of COVID-19 are eligible for mortgage forbearance, or the right to delay mortgage repayments, for up to 12 months, without it counting as a default or having an impact on their credit score. This should limit defaults in the CRT pools.

This should also help keep distressed home sales off the market. The scale and speed of policymakers’ response (the forbearance program was announced in a matter of weeks) should help to limit downward pressure on home prices.

During the last crisis, forbearance measures were not announced until 2010―two years after the market collapsed, and after home prices had declined by around 20%. By that stage, many borrowers had seen the equity in their homes turn negative, so it made more sense for them to default on their loans and surrender their properties than to delay repayments.

Today, many borrowers have enough equity in their homes to provide an incentive to sell rather than default, should their economic circumstances deteriorate.

At the same time, low interest rates are helping to reduce default risk by making it easier for homeowners to refinance. When these borrowers refinance their mortgages, their loans are taken out of the CRT pools. This leaves fewer investors in the mortgage pools who can potentially default if their economic situation worsens.

Refinancing and forbearance help to reduce potential defaults, but they have additional implications for CRT investors, as they potentially affect the pay-off profile of the securities.

For example, the prepayment that occurs when a refinancing takes place would shorten the life of a CRT, while forbearance would lengthen it. (When a larger number of borrowers request forbearance, the investors continue to receive coupon payments, but the principal payments get delayed.) Overall, we expect the life of these bonds to be shorter relative to our expectations earlier in the year. Since CRTs trade at a discount to par, this will potentially allow their prices to rise more quickly, boosting near-term returns.

VALUATIONS ATTRACTIVE, DESPITE TOUGHER ASSUMPTIONS

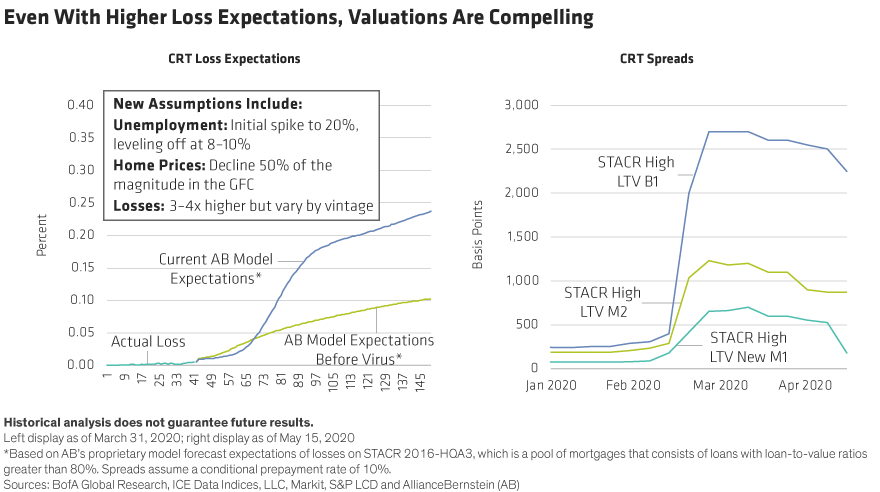

Still, given the current environment, we have revised our assumptions about the outlook to account for more conservative settings. We have factored in a three- to four-fold increase in losses on the underlying mortgage pools (varying by vintage) based on an initial 20% spike in unemployment (levelling off at 8%‒10%) and a decline in home prices to 50% of that experienced during the Great Recession.

These higher loss expectations are not only more than reflected in current valuations (Display), they are also well covered by credit enhancements on many CRTs, especially older ones, where the properties represented by the underlying mortgage pools have appreciated in value over time.

As already noted, the sector has shown some recovery since the selloff in March, helped by the inclusion of investment-grade CRTs in the Federal Reserve’s Primary Dealer Credit Facility program.

The rally started with the less subordinated, investment-grade tranches but has eventually become more broad-based and even started to include the more seasoned equity tranches as investors have looked to take advantage of spreads that are still several times their pre-crisis levels.

More recently, the bonds benefited from a GSE announcement that borrowers who have requested forbearance but continue to make mortgage payments (approximately 30%–40% of those in the forbearance program) will be eligible for refinancing.

Despite its recent rebound, the sector’s recovery continues to trail a sharp bounce back of other markets, like corporate high-yield bonds. To us, this suggests that CRTs have more upside potential. That’s an important factor for those who are looking for opportunities that capitalize on the continued rebound in the markets.

Indeed, current CRT valuations have begun to attract a broader range of investors, including crossover buyers (opportunistic investors from other bond-market sectors), insurance companies and private equity firms. This could be a sign that CRTs may not lag the broad market recovery for much longer.

Janaki Rao is Portfolio Manager and Head of Agency Mortgage-Backed Securities Research and Monika Carlson is Senior Investment Strategist—Fixed Income at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein