When the COVID-19 crisis shook markets in March, the Federal Reserve moved early and aggressively to help increase liquidity in financial markets. As part of that effort, the Fed introduced bond-buying facilities to purchase investment-grade corporate bonds. Those facilities began making purchases on May 12th.

Given its unprecedented nature, this has led to many questions about the logistics of the facilities, what it means for the markets, and what it means for investors. Below are some of the most frequently asked questions:

What are the corporate bond-buying facilities?

The Fed announced two facilities on March 23rd:

- Primary Market Corporate Credit Facility (PMCCF)

- Secondary Market Corporate Credit Facility (SMCCF)

The PMCCF will purchase bonds in the primary market, meaning when the bonds are initially issued.

The SMCCF will purchase corporate bonds and corporate bond exchange-traded funds (ETFs) in the secondary market. The secondary market is where bonds are bought and sold after their initial issuance.

Both of these facilities will operate as special purpose vehicles (SPVs). The Federal Reserve itself is not able to purchase corporate bonds, so it will lend to the newly created SPVs, which will then buy bonds and lend to corporations.

Why did the Fed launch these facilities?

Beginning in early March, corporate bond spreads began to rise. A credit spread is the additional yield a corporate bond offers above the yield offered on a Treasury security with a comparable maturity. It’s meant to compensate for the extra risks investors take in owning corporate bonds, including the risk that the issuer may not be able to make debt payments.

When COVID-19 concerns really took hold in early and mid-March, many corporations were not able to issue new bonds in the primary market. Lenders were generally unwilling to lend to corporate borrowers, or the borrowing costs may have been prohibitive for some issuers. By launching these facilities, the Fed is helping support the corporate bond market, ultimately serving as a lender for eligible companies that need or want to issue debt.

The announcement of these corporate bond-buying facilities brought credit spreads down sharply, helping more corporations to issue new debt.

What bonds are eligible?

There are a number of conditions an issuer needs to satisfy to be eligible,1 but some of the key conditions include:

- Ratings of BBB+/Baa3 or above on or after March 22, 2020.2

- The business must be created or organized in the United States and a majority of its employees must be based in the United States.

- The issuer must not be an insured depository institution or depository institution holding company, as such terms are defined in the Dodd-Frank Act. In other words—no banks.

- Maturities of four years or less for the PMCCF or five years or less for the SMCCF.

How many corporate bonds and corporate bond ETFs can the facilities buy?

The PMCCF and SMCCF have a combined capacity of $750 billion. The U.S. Treasury will make a $75 billion equity investment in the facilities, and the Federal Reserve will use its borrowing power to increase the capacity to $750 billion.

The SMCCF became operational on May 12th, but with initial purchases of corporate bond ETFs only. For the week ending Wednesday, May 21, 2020, the SMCCF held $1.8 billion in corporate bond ETFs. The facility is expected to begin buying individual corporate bonds in the near future, but a specific date has not yet been announced. The PMCCF is expected to become operational in the near future, as well.

The corporate bond markets have relatively stabilized since the announcement of these facilities. As a result, we believe the Fed would prefer to use as little of its buying power as possible, and only serve as a lender of last resort. Barring a major flare-up in the corporate bond market, we believe the facilities will hold significantly less than the $750 billion capacity.

How many high-yield bonds will the Fed be buying?

Very few.

The only individual high-yield corporate bonds that the Fed may purchase are those that have been downgraded from investment-grade to “junk” on or after March 22, 2020. Bonds that have been downgraded from investment-grade to high-yield are called “fallen angels,” and only a handful of corporate bonds have become fallen angels since March 22nd.

The SMCCF is able to buy high-yield corporate bond ETFs, but has specified that it intends to limit those purchases. According to the SMCCF term sheet, the “preponderance of ETF holdings will be of ETFs whose primary investment objective is exposure to U.S. investment-grade corporate bonds, and the remainder will be in ETFs whose primary investment objective is exposure to U.S. high-yield corporate bonds.”

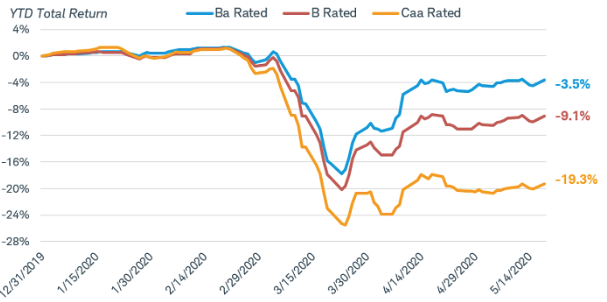

Despite headlines about the ability of these facilities to buy high-yield bonds, the number of high-yield bonds that are eligible for purchase is extremely limited. Based on our calculations, there’s less than $50 billion in eligible high-yield bonds to be purchased (mostly from one recent fallen angel), compared to the total amount outstanding of the Bloomberg Barclays U.S. Corporate High-Yield Bond Index of almost $1.4 trillion. There is a lot more direct support for the investment-grade market, and we still see risks to the high-yield market given the limited support from the Fed.

The lowest-rated parts of the high-yield market have not recovered as much

Source: Bloomberg. Indexes represented are the Bloomberg Barclays U.S. Corporate High-Yield Ba Rated Bond Index (BCBATRUU Index), Bloomberg Barclays U.S. Corporate High-Yield B Rated Bond Index (BCBHTRUU Index), and the Bloomberg Barclays U.S. Corporate High-Yield Caa Rated Bond Index (BCAUTRUU Index). Total returns from 12/31/2019 through 5/18/2020. Total returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no indication of future results.

I want to sell an eligible bond—will the Fed buy it from me?

No.

The SMCCF can purchase individual corporate bonds from “eligible sellers,” which initially will be primary dealers that meet the eligible seller criteria. However, knowing that the SMCCF will purchase eligible bonds from primary dealers should result in more potential buyers for your bond.

As the Fed is buying investment-grade bonds, does that make them safer than what the credit rating implies?

No.

The Fed is simply buying bonds—it’s not bailing out corporations. The bonds purchased still need to repaid by the issuers. These facilities do not suddenly convert a corporate bond to a grant that can be forgiven.

The Fed’s ability to purchase corporate bonds will not prevent further downgrades, nor will it prevent many corporations from defaulting. In fact, both Moody’s and S&P expect the default rate to surge to levels not seen since the 2008-2009 financial crisis, despite the Fed’s assistance. These facilities are bearing that credit risk, meaning it’s possible that the Treasury won’t get back its full $75 billion investment if many corporate bonds default. However, because the Fed will buy mostly investment-grade bonds, and defaults are most likely with the riskiest high-yield bonds, we don’t view that outcome as likely.

What impact have these facilities had on the market?

Following the announcement of the PMCCF and SMCCF, we’ve seen three key market changes:

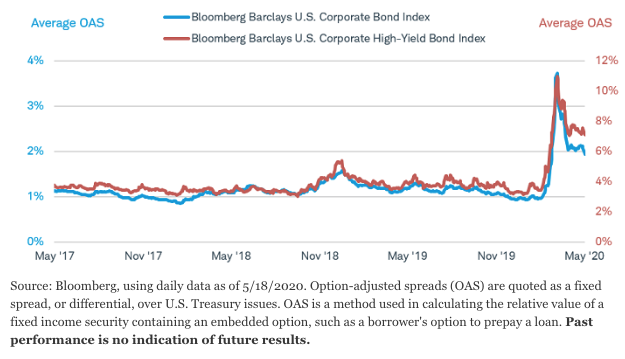

1. Lower credit spreads. Spreads surged in mid-March due to negative impact of fighting the coronavirus. With the economy slowing to a halt, corporate profits were likely to suffer, making it difficult for issuers to make timely interest and principal payments. Spreads rose as a result, as investors demanded higher yields to compensate for that increased risk. Spreads have declined sharply since the Fed’s corporate bond buying facilities were announced, but still remain above the pre-COVID-19 levels.

The drop in spreads means investors are earning relatively lower yields today compared to mid-March. However, we believe the presence of these corporate bond-buying facilities may prevent investment-grade spreads from rising back to those levels, meaning prices might not experience the sharp prices declines like those seen in March (remember that bond prices and yields move in opposite directions).

Spreads are off their highs, but are above pre-COVID-19 levels

Source: Bloomberg, using daily data as of 5/18/2020. Option-adjusted spreads (OAS) are quoted as a fixed spread, or differential, over U.S. Treasury issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan. Past performance is no indication of future results.

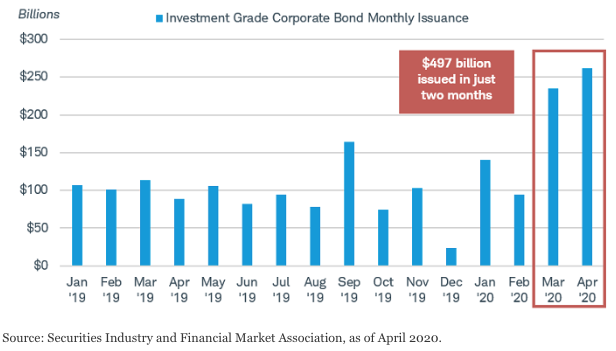

2. Record-breaking new issuance.The corporate new-issue market effectively shut down in early and mid-March. Investors generally were not interested in lending to corporations, given the increased risk, or the extra yield needed (the aforementioned spread) may have been prohibitive for many would-be borrowers.

That all changed after the announcement of the new facilities. Both March and April witnessed record-breaking new issuance in the investment-grade corporate bond market, while issuance continued to surge through the first few weeks of May. This increased issuance generally occurred before any purchases by the Fed’s facilities actually took place. It should help corporate issuers weather the storm, by helping them build up their cash reserves to offset the likely drop in revenues due to the effects of COVID-19. The increase in debt issuance does come with risks: a larger debt load to service over the long run.

Investment-grade corporate bond issuance has surged

Source: Securities Industry and Financial Market Association, as of April 2020.

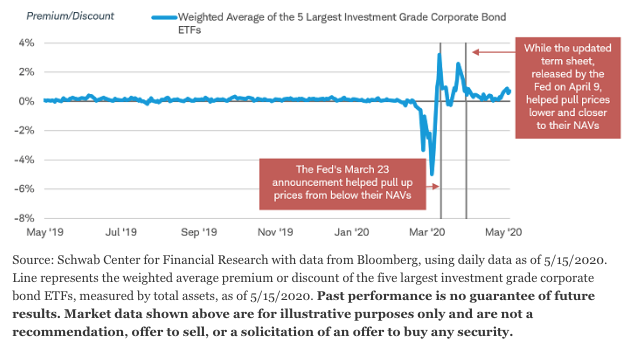

3. ETF prices are generally back in line with their net asset values (NAV). ETFs suffered in March, not only from the drop in the value of their assets, but as the prices of many ETFs dropped below their net asset values, meaning they were priced at a “discount.” In other words, at the trough, many ETFs posted total returns that were even worse than the value of their holdings would have indicated.

Once the Fed announced the SMCCF, the opposite happened—the prices of many corporate bond ETFs surged above the value of the underlying holdings, meaning they were priced at a “premium.”

With the launch of the SMCCF, the prices of most corporate bond ETFs are more in line with their NAVs. Considering the facility is meant to help provide liquidity in the corporate bond market, it appears that that goal had been achieved before any purchases even took place.

Prices of many investment-grade corporate bond ETFs are generally no longer at deep discounts

Source: Schwab Center for Financial Research with data from Bloomberg, using daily data as of 5/15/2020. Line represents the weighted average premium or discount of the five largest investment grade corporate bond ETFs, measured by total assets, as of 5/15/2020. Past performance is no guarantee of future results. Market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

What does this mean for investors?

-

Investment-grade corporate bonds appear relatively attractive given the direct support from the Fed’s corporate bond-buying facilities. The good news is that this should allow corporations to refinance their maturing bonds or issue new bonds to build up their cash balances. However, corporate profits should remain under pressure and this won’t necessarily prevent additional downgrades. With spreads above their long-term average, investment-grade corporate bonds appear attractive for investors willing to take on some additional risk compared to holding very high-quality investments like U.S. Treasuries. We’d caution that volatility could pick up if the outlook deteriorates, however. For those investors looking for very conservative investments and stability/low volatility, investment-grade corporate bonds are probably not appropriate.

-

High-yield bonds have less direct support and therefore we suggest investors cautiously consider adding them to portfolios, but only if you have a more moderate or aggressive risk tolerance to handle potential volatility. If the economic outlook deteriorates further or the stock market declines, high-yield bond prices may still fall sharply. For those who invest in individual high-yield corporate bonds, we favor those with “BB” ratings over those with ratings of single “B” or below, and reiterate that we expect defaults to pick up for those high-yield bonds at the low end of the rating spectrum. For investors who invest using bond funds, we prefer an actively managed fund that limits exposure to bonds with ratings of “CCC” or below, rather than a fund that takes a passive, index-tracking approach.

1 For the full term sheet and frequently asked questions, please visit the Federal Reserve Bank of New York’s website: FAQs: Primary Market Corporate Credit Facility and Secondary Market Corporate Credit Facility.

2 If rated by multiple rating agencies, the issuer must have had BBB+/Baa3 ratings or above by two or more agencies on March 22, 2020..Credit ratings by a nationally recognized statistical rating organization (NRSRO). Currently, the facilities will accept ratings from S&P Global Ratings, Moody’s Investors Services Inc., and Fitch Ratings, Inc., but they may consider additional NRSROs in the future.

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab