China’s stock markets have been remarkably resilient. As the world’s second-largest economy emerged first from the virus-induced shock, corporate earnings downgrades were relatively contained while government stimulus was preserved for future use.

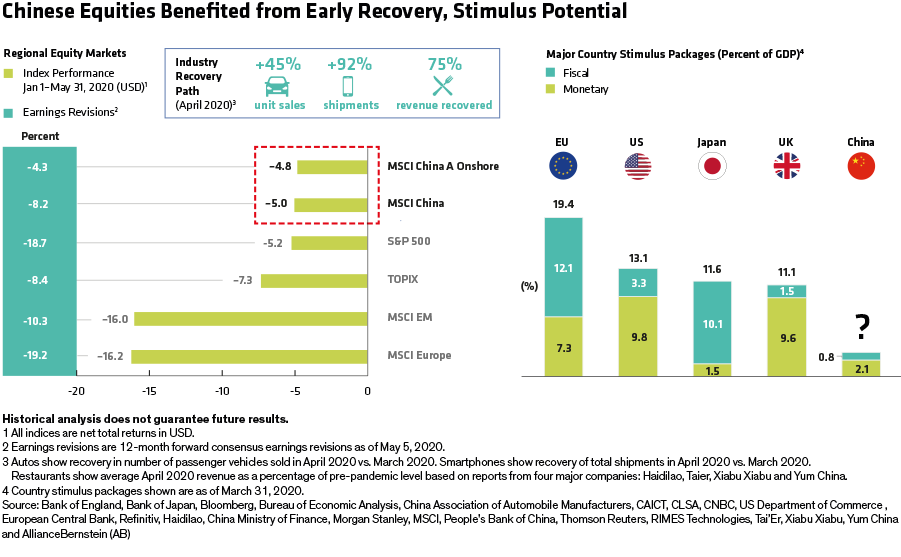

By May 31, the MSCI China Index, including onshore and offshore Chinese stocks, had fallen 5.0% since the beginning of the year in US dollar terms (Display, left, upper bars). The MSCI China A Onshore Index was down by 4.8% over the same period. Chinese stocks have done relatively well in the difficult environment for three reasons.

1. First Out, First Back

Since China was hit by the virus first, its economy has also recovered earlier. Of course, there’s a real risk of another wave of infections. Still, the earlier exit from the lockdown means businesses are getting back online and the economy is starting to rev up.

2. Industry Recoveries Curb Earnings Hit

Key industries are recovering sharply. Auto and smartphone sales have rebounded, while restaurants are filling tables again. To be sure, some sectors are still struggling, such as travel and leisure. However, as a whole, Chinese corporate fundamentals haven’t been hit as hard as other countries. As a result, earnings revisions in China have been relatively modest (Display, left, lower bars).

3. More Stimulus Potential

Chinese policymakers have introduced measures to support the hardest-hit parts of the economy. Yet the level of fiscal and monetary stimulus versus GDP is much lower in China than elsewhere (Display, right).

Policymakers, like investors, still vividly remember the hangover from the debt-financed stimulus in 2009–2010. And China’s domestic economy is much different than developed economies because employment-sensitive consumption and services sectors make up a smaller portion of the economy compared to the West. So the lockdown, which hit those sectors disproportionally, also had a milder impact on employment in China, meaning less government support was needed. However, now that overseas orders for Chinese factories are drying up, we expect policy stimulus measures to ramp up, and the Chinese government has plenty of firepower to do just that.

Before the new coronavirus hit, Chinese equity valuations were lower than major global peers amid concern about the ongoing US trade war and the pace of macroeconomic growth. Lower valuations may have also helped reduce the damage when the virus hit. Today, domestic Chinese shares trade at a price/earnings ratio of about 11.7×, based on 12-month forward earnings estimates. This is still lower than that of US and European stocks, which trade at 18.9× and 14.5× respectively, as of May 31. While near-term earnings visibility is still very cloudy, the direction is probably clearer than in other parts of the world. As a result, we believe investors who identify Chinese companies with solid businesses can find attractive positions for the next stage of the recovery.

John Lin is Portfolio Manager of China Equities at AllianceBernstein (AB).

Stuart Rae is Chief Investment Officer of Asia-Pacific Value Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein