Many have been confounded by the stock market’s surge since March 23rd amid less-than-rosy U.S. economic data. That disconnect narrowed on Thursday, as jitters about a potential second wave of COVID-19 infections—along with a grim economic outlook from the Federal Reserve—drove investors out of riskier assets and led to a 5.9% drop in the S&P 500® index.

Ongoing volatility underscores the precariousness of the recent rally. Even as the S&P 500 index rallied to recoup much of the losses made since its March 23rd low, we have cautioned that a second wave of coronavirus cases could upend investor confidence, raising the prospect of a fresh round of social-distancing restrictions or layoffs.

U.S. stocks and economy: Mixed signals

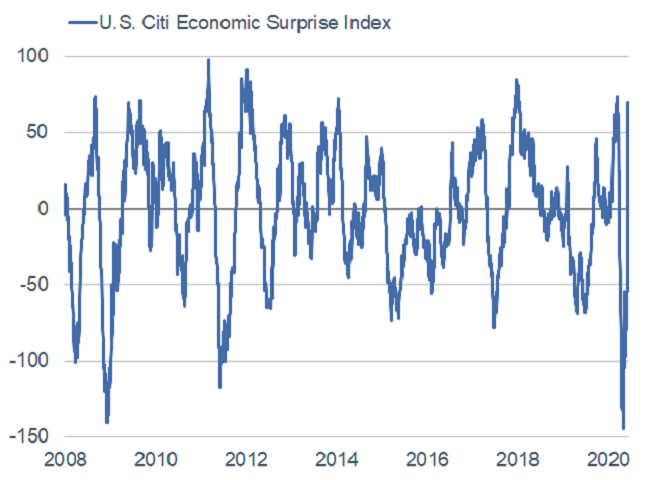

In recent weeks, the gap between economists’ estimates and actual May U.S. payroll gains caused Citi’s Economic Surprise Index to spike. The series, which measures data surprises relative to market expectations, has recovered from its deep plunge into negative territory, confirming that data in the past week have continued to come in better than anticipated—although remaining very weak in absolute terms.

The Citi Economic Surprise Index rose sharply recently

Source: Charles Schwab, Bloomberg, as of 6/10/2020.

The rub with the recent uptick is that the unexpectedly strong May jobs report—in which payrolls gained 2.5 million jobs and the unemployment rate declined to 13.3%—alone constituted most of the surge into positive territory. In other words, positive surprises reflected extremely low expectations, not a meaningful improvement in the growth rate of the economy. The hole from which the economy has to emerge—however narrow—is deep enough to suggest market-based enthusiasm about a sharp recovery may have been unfounded.

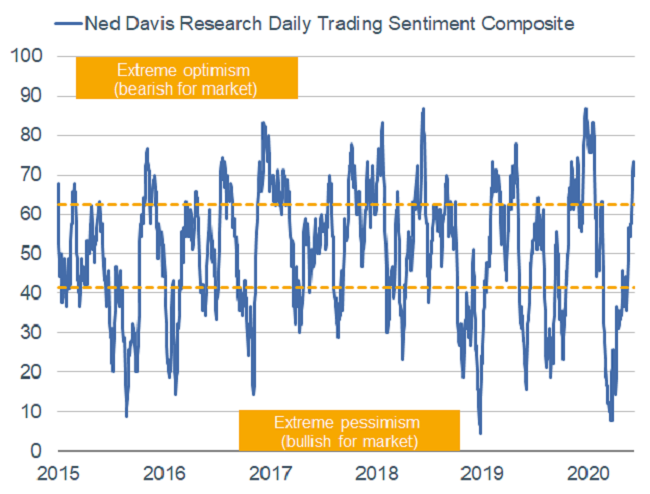

As U.S. stocks rallied off the March lows, measures of investor sentiment followed suit; with some behavioral measures showing signs of excessive optimism and even froth, and attitudinal measures starting to signal complacency.

As you can see in the chart below, Ned Davis Research’s Crowd Sentiment Poll—a reflection of various sentiment indicators—has emerged out of the “extreme pessimism” zone and, as of June 9th, climbed well into extreme optimism territory. Extremes were also seen in options trading (as per recent findings by SentimenTrader) and huge spikes in hyped-up bankruptcy stocks’ prices (as per Bloomberg).

We like to remind investors that sentiment at extremes doesn’t in and of itself suggest a near-term surge or pullback is imminent. Rather, it signals that stocks have become more vulnerable to negative catalysts, which could come in the form of downbeat economic- or virus-related developments—as was the case by Thursday.

Investor sentiment has moved into the “extreme optimism” zone

Source: Charles Schwab, ©Copyright 2020 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. Data as of 6/10/2020.

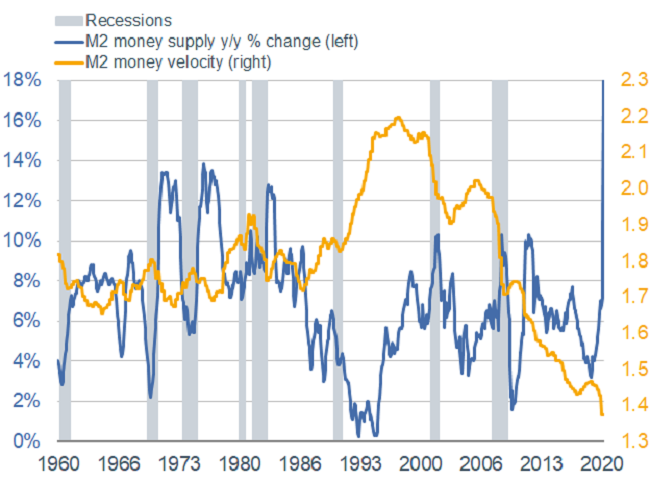

Much of the stock market’s recent rally can be attributed to the massive provisions of liquidity and income support from the Federal Reserve and Congress—providing relief measures equal to nearly 30% of the Congressional Budget Office’s 2020 estimated U.S. gross domestic product. Specifically on the monetary front, the Fed’s balance sheet has swelled to $7.2 trillion in an effort to ease financial system strains during the crisis.

The central bank’s large-scale asset purchases have stoked fears of impending inflation, but the risk appears low in the near term. As you can see in the chart below, while money supply has skyrocketed, the velocity of money has moved in the opposite direction. In order to produce inflation, money velocity typically increases as banks lend more; however, banks are currently accumulating assets on their balance sheets and thus keeping money out of circulation.

Money supply has increased, but money velocity has decreased

Source: Charles Schwab, Bloomberg, Federal Reserve Bank of St. Louis, as of 4/30/2020. M2 is a calculation of the money supply that includes cash and checking deposits, savings deposits, money market securities, mutual funds, and other time deposits. The velocity of money is the number of times one dollar is spent to buy goods and services per unit of time. If the velocity is increasing, then more transactions are occurring between individuals in an economy.

Global stocks and economy: Improving economy, deteriorating relationship

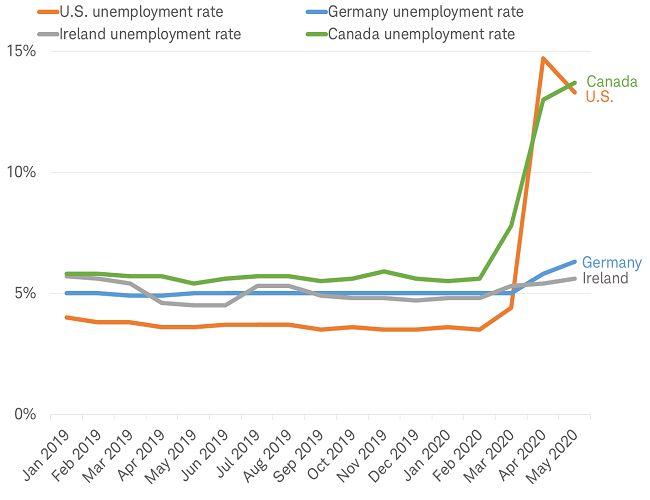

The United States was the only country to report a decline in its unemployment rate in May. However, from a global perspective, incoming real-time data have generally been much better than expected.

Unemployment usually lags the economic recovery

All countries reporting May unemployment rate as of 6/5/2020.

Source: Charles Schwab, Bloomberg data as of 6/5/2020.

The deterioration in U.S.-China relations may be a risk to otherwise-favorable economic news. U.S. President Donald Trump has announced a range of measures in response to recent Chinese actions, including the passage of a new security law for Hong Kong. Yet the specific policies were relatively narrow in scope. Notably, the focus of tensions in 2018 and 2019—the “phase one” trade agreement—was missing from the announcements. In response, global stock markets resumed their rally, led by emerging market stocks.

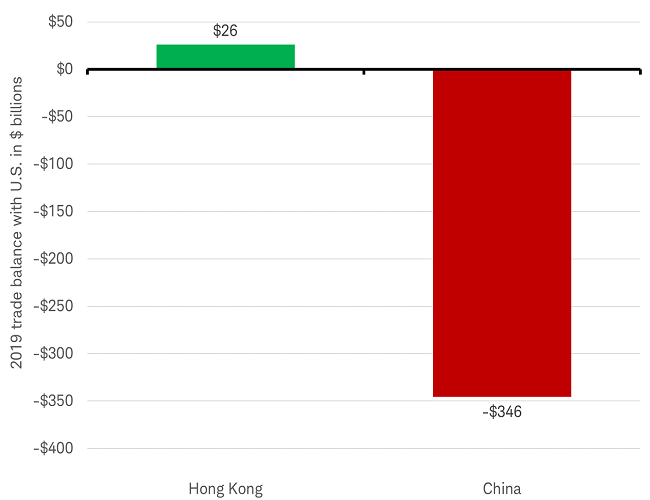

One concern is the potential U.S. revocation of Hong Kong’s zero tariff rate, which may spark retaliation from China and its subsequent lifting of Hong Kong’s rate on imports of U.S. goods. Contrary to its large trade deficit with mainland China, the United States has a trade surplus with Hong Kong, valued at $26 billion in 2019. Damaging this relationship would hurt the United States more than China, making it an unlikely course of action.

U.S. has a trade surplus with Hong Kong

Source: Charles Schwab, Bloomberg data as of 6/5/2020.

While we expect U.S. legislation related to the delisting of Chinese firms to become law, it would be at least four years before it would affect current listings. In that time, the Chinese Securities Regulatory Commission could change its rules and allow U.S. audits of Chinese companies, avoiding any delisting. It’s unlikely to be an issue for the companies themselves. Research has shown that Chinese American Depository Receipts (ADRs) are more likely to be associated with a Big 4 accounting firm and are less likely to restate prior period financial statements than ADRs from other countries.

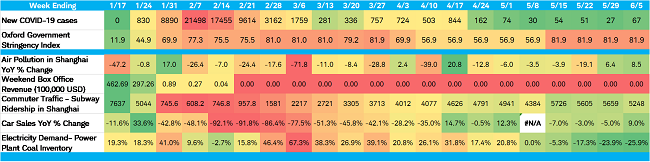

Despite the risks associated with increasing U.S.-China tensions, emerging market stocks seem to be focusing on China’s V-shaped economic recovery. China’s economy was both the first in and out in terms of imposing a lockdown. Weekly data we measure from independent sources (not from the Chinese government) are back in the green—reflecting the full recovery seen in China’s widely-watched purchasing managers’ index, as it rebounded above 50—the threshold between contraction and expansion—in May.

China recovery heat map as of June 6, 2020

Source: Charles Schwab, World Health Organization, United Nations, China Passenger Car Association, Bloomberg, Box Office MoJo, Macrobond data as of 6/5/2020.

We don’t believe the tensions between the United States and China are a reason to avoid emerging market stocks. Historically, they have tended to lead rebounds coming out of bear markets. Not to mention, they typically benefit when global growth is improving and cyclical stocks are outperforming, which has been the case in recent weeks.

Fixed income: Not much room to run from here

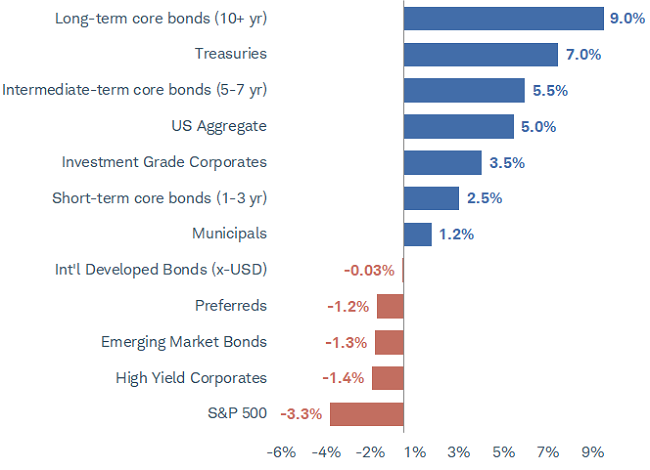

Federal Reserve policy has been the major driver behind returns in the fixed income markets over the past few months. Since the Fed stepped in to help provide liquidity to the markets in mid-March, the yield curve has steepened and bonds in riskier segments of the market have outperformed Treasury bonds—trends that are associated with an improving economy. We continue to be concerned that the markets have been too optimistic about a rapid economic recovery.

Fixed income asset class total returns, year-to-date

Source: Bloomberg. Returns from 12/31/2018 through 6/8/2020. Indexes representing the investment types are: US Aggregate = Bloomberg Barclays U.S. Aggregate Index; Short-term core = Bloomberg Barclays U.S. Aggregate 1-3 Years Bond Index; Intermediate-term core = Bloomberg Barclays U.S. Aggregate 5-7 Years Bond Index; Long-term core = Bloomberg Barclays U.S. Aggregate 10+ Years Bond Index; Treasuries = Bloomberg Barclays U.S. Treasury Index; Municipals = Bloomberg Barclays US Municipal Bond Index; IG Corporates = Bloomberg Barclays U.S. Corporate Bond Index; HY Corporates = Bloomberg Barclays US High Yield Very Liquid (VLI) Index; Preferreds = ICE BofA Merrill Lynch Fixed Rate Preferred Securities Index; Int. developed (x-US) = Bloomberg Barclays Global Aggregate ex-USD Bond Index; EM USD = Bloomberg Barclays Emerging Markets USD Aggregate Bond Index; S&P 500 = S&P 500 Total Return Index (SPXT). Returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

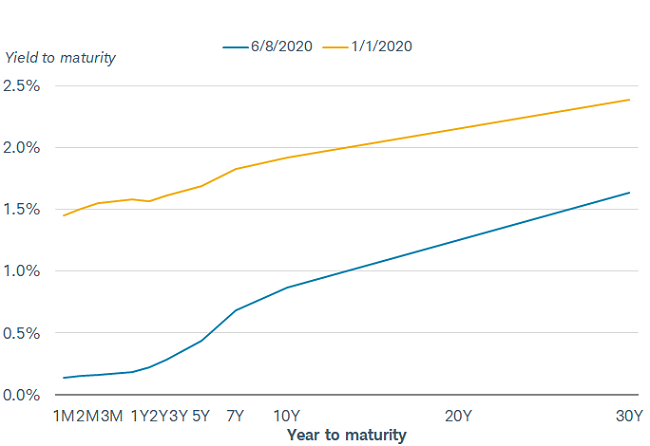

The Fed’s low-interest-rate policy and various facilities are providing support for the economy and liquidity to the markets. By lowering short-term interest rates to near zero and adding bonds to its balance sheet, the Fed managed to ease the panic in the markets that drove 10-year Treasury bond yields to all-time lows in March. As the outlook has brightened, investors have moved out of safe-haven Treasuries in search of higher yields in other markets. Yields for intermediate- to long-term Treasuries have moved up, while short-term yields remain anchored near zero by Fed policy, resulting in a steepening of the yield curve.

Treasury yield curve has steepened since January

Source: Bloomberg as of 6/8/2020 and 1/1/2020. Past performance is no guarantee of future results.

While we expect the economy to recover in the second half of the year, the move up in longer-term yields may be discounting a more robust recovery than is likely. Many states still have restrictions on business activity and it’s not clear how long it will take for consumer demand to rebound. Moreover, inflation is likely to remain low in light of very high unemployment, and excess capacity in many industries. We expect 10-year Treasury yields could rise to about 1% in the second half of the year, but not much higher unless growth exceeds our expectations. Consequently, although we expect the yield curve to stay positively sloped, we don’t look for much more of an increase in yields from current levels.

We continue to suggest investors keep the average durations in their portfolios somewhat below their benchmarks since interest rates are so low. However, we wouldn’t suggest moving all of a fixed income allocation to very short-term maturities, as we expect the Fed to keep short-term rates near zero until at least the end of 2021.

In the corporate bond market, we still expect to see more credit rating downgrades to highly leveraged companies in the investment-grade market and a wave of defaults in the high-yield market. After the sharp rally, there is less compensation in the form of extra yield in the market for those risks than just a few weeks ago. We suggest investors avoid too much exposure to lower-rated corporate bonds and focus on issuers with stronger balance sheets that can weather the ups and downs of the recovery.

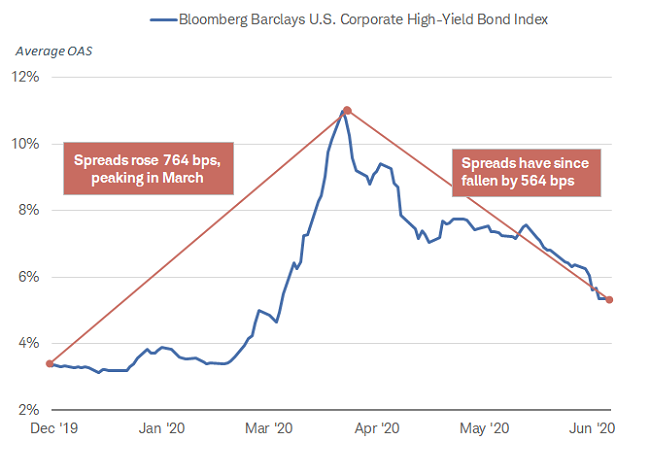

High-yield spreads are now only 200 basis points above the 2019 closing level

Source: Bloomberg, using weekly data as of 6/5/2020. Option-adjusted spreads (OAS) are quoted as a fixed spread, or differential, over U.S. Treasury issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan. Past performance is no indication of future results.

What investors can do now

Although stock markets have shown great resiliency in climbing back from recent lows, Thursday’s extreme drop is a reminder that investors should always be prepared for volatility. Here are a few things all investors should remember:

1. Resist the urge to react to daily market movements.Selling stocks when markets drop can make temporary losses permanent. Staying the course, while difficult emotionally, may be healthier for your portfolio. This doesn’t mean you should hold on blindly, but we suggest taking into account an investment’s future prospects and the role it plays in your portfolio, rather than being guided by short-term market movements.

If you need money in the next few weeks or months, then you may need to sell some assets to raise cash. Consider using tax-loss harvesting to lessen the impact of selling on your portfolio,

2. Make sure your portfolio is appropriately diversified. It’s always important to be diversified, but it’s crucial in rapidly changing markets. Having a mix of investments—including international as well as domestic stocks, fixed income securities, and a healthy equity sector mix—can help buffer a portfolio during market ups and downs.

3. Make sure your portfolio is consistent with your goals, risk tolerance, and preferences.If you’re uncomfortable with recent market volatility and your goals are short term, you may want to decrease your exposure to riskier assets and move that money to Treasuries or bank certificates of deposit (CDs) to reduce volatility.

If recent volatility has made you reevaluate your priorities, consider taking the time to rethink the key features of your financial life—whether it’s your budget or debt situation, or longer-term issues such as insurance and your estate plan.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Diversification and asset allocation strategies do not ensure a profit and cannot protect against losses in a declining market.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third-parties and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0620-0DUW)

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab