Key Points

- Although municipal bonds pay interest that is generally exempt from federal and state income taxes, it's not always free from all taxes.

- We identify some of the taxes that could apply if you buy municipal bonds and next steps you may want to consider.

Investors often think of municipal bonds, which are sold by local and state governments to fund public projects like building new schools and repairing city sewer systems, as being totally tax-free—but that’s not always the case.

While the interest payments on munis are usually exempt from federal income taxes, other taxes may apply. It’s important to know the rules, because municipal bonds are one of the few investments available to income-oriented investors looking to reduce their income tax bills. Here are seven types of taxes that could apply if you buy muni bonds.

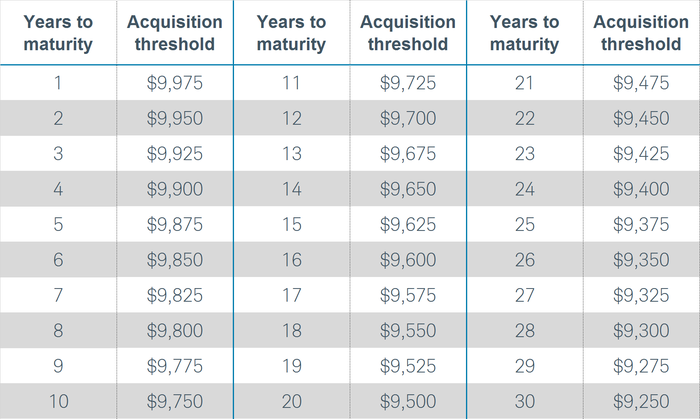

1. De minimis tax. The de minimis tax applies to munis that you acquired at a market discount. The de minimis rule says that for bonds purchased at a discount of more than 0.25% for each full year from the time of purchase to maturity, gains resulting from the discount are taxed as ordinary income rather than capital gains. The ordinary income tax rate is generally greater than the capital gains rate, which could result in a greater bite out of your yield.

For example, take a bond that matures in 10 years with a face value of 100. The de minimis “breakpoint” on this bond is 97.5 (100 – [0.25 × 10 years]). If you bought this bond for less than 97.5, you would be required to pay ordinary income tax on the discount.

De minimis thresholds for a $10,000 face value muni

Source: Schwab Center for Financial Research. The example is hypothetical and provided for illustrative purposes only.

What you can do: To avoid the de minimis tax rule, consider purchasing bonds priced at par or at a premium to their face value. Paying a premium may mean having to make adjustments to your tax filing, but the associated tax benefits more than offset the added complication, in our view. In addition, if a bond is selling at a premium, it’s likely because it is offering a high coupon rate.

2. Alternative minimum tax. There are two parallel income tax systems in the United States: ordinary income tax and alternative minimum tax (AMT), which disallows a number of deductions that are allowed in the ordinary income tax code. Taxpayers must calculate their tax under each system, then pay whichever is higher—ordinary or AMT.

Income from some municipal bonds—for example, those that fund stadiums, airports or more businesslike enterprises—might be subject to AMT. If you have to pay AMT and hold such a bond, your interest income would generally be taxed at the applicable AMT rate—which could be 26% or more, if you’re in the AMT exemption phase-out range. Effectively, that means the yield on a municipal bond paying 2.00% would drop to 1.48%. The 2017 tax law increased the phase-out thresholds for AMT to $1 million for joint filers, up from $160,900—meaning fewer filers will be subject to AMT under the new tax laws. The phase-out threshold is $1,036,800 for 2020 for married filing jointly.

What you can do: For bonds held at Schwab, you can find out if a municipal bond is subject to AMT by accessing the “Research” page after logging into schwab.com, searching for a municipal bond and viewing its “Security Description” page.

3. Increase in taxation of Social Security benefits. Although municipal bonds generally aren’t subject to federal taxes, the IRS does include income from such bonds in your modified adjusted gross income (MAGI) when determining how much of your Social Security benefit is taxable. If half of your Social Security benefit plus other income, including tax-exempt municipal bond interest, amounts to more than $44,000 for a joint return ($34,000 for individual), up to 85% of your Social Security benefits may be taxable.

What you can do: If you are receiving Social Security benefits, we suggest reviewing IRS Publication 915, “Social Security and Equivalent Railroad Retirement Benefits,” or this page from the Social Security Administration, which both discuss the taxation of retirement benefits, to determine how this might apply to your individual situation.

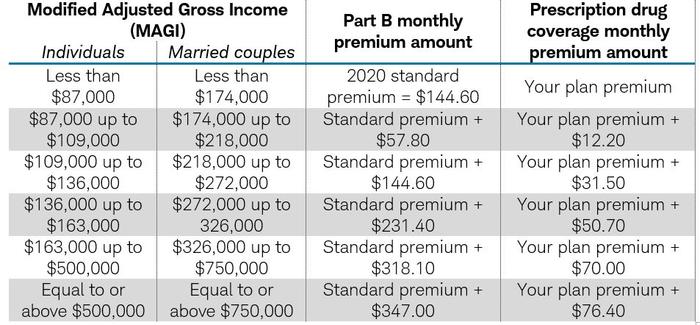

4. Increase in Medicare premiums. If you’re covered by Medicare, the federally tax-exempt interest from municipal bonds may increase the amount you pay for Medicare Part B or Medicare prescription drug coverage. If you’re married and filing jointly and your MAGI is more than $170,000 ($85,000 for single filers), you will be required to pay an additional amount for Medicare Part B and Medicare prescription drug coverage.

Income to determine monthly Medicare premiums may include municipal bond interest

Source: Social Security Administration. Data obtained on 6/8/2020

To determine your Medicare premiums, the Social Security Administration generally uses your most recent federal tax return. For example, to determine 2020 monthly adjustment amounts, the Social Security Administration would use your tax return filed in 2019 for tax year 2018. You can learn more about Medicare premiums in the Social Security Administration publication “Medicare Premiums: Rules For Higher-Income Beneficiaries.”

What you can do: We don’t believe paying an additional Medicare premium justifies not investing in municipal bonds. Given that your MAGI will also include income from other sources, such as dividend income and interest income from taxable bonds, avoiding municipal bonds will not necessarily allow you to avoid the increase in Medicare premiums. Also, investing in zero-coupon bonds likely won’t allow you to avoid paying higher premiums, because the part of the increase in the zero-coupon bonds’ value may be included in the calculation to determine your Medicare premiums.

5. Capital gains tax. We generally suggest individual investors hold a bond until maturity. However, if you need to sell earlier and you receive a price greater than your cost basis—your acquisition price after adjusting for any premiums paid or discounts received—the gain will be subject to capital gains tax.

What you can do: Determining cost basis for an individual bond can get complicated, as there are special reporting rules that govern the adjustments to a bond’s acquisition price. For bonds held at Schwab, you can find your adjusted cost basis on the “Positions” page after you log into schwab.com.

6. State income tax. If you purchase a bond from your home state, generally the interest payments you receive will be exempt from state income taxes. However, interest paid on bonds from outside of your home state typically will be subject to state income tax. Interest payments on some in-state munis may also be subject to state income taxes.

What you can do: If you live in a state with low tax rates or one that issues a minimal amount of municipal bonds, we would suggest looking outside your home state. The added benefits of diversification and potentially higher yields might make up for the hit you would take by paying state income taxes.

7. Taxable municipal bonds. Some munis are taxable. For example, interest paid on bonds issued to help fund an underfunded pension plan or bonds issued under the Build America Bonds (BABs) program is federally taxable. Taxable muni bonds generally yield more than tax-free bonds to make up for the difference.

What you can do: For investors in lower tax brackets and investing in taxable accounts, or those investing in either Roth or traditional IRA accounts, we believe taxable municipal bonds can make sense compared to other taxable bonds because, historically, munis have exhibited stronger credit characteristics than corporate bonds of comparable ratings.

The bottom line is that municipal bonds offer significant tax advantages and could make sense in the portfolios of many income-focused investors. However, the details matter. If you are highly tax-sensitive and would like to invest in these securities, you will want to make sure you understand how the tax traps mentioned above might affect your portfolio.

If you have questions about your portfolio, you could consult IRS Publication 550, “Investment Income and Expenses,” or check in with your tax advisor.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security’s tax-exempt status (federal and in-state) is obtained from third-parties and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice. Where specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax advisor, CPA, financial planner or investment manager.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0620-0A7Y)

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab