Key Points

-

A second wave of global COVID-19 is getting a lot of media attention, but the appearance of a global second wave of cases is primarily driven by the different timing of first waves across countries—rather than second waves within countries.

-

The falling trend in deaths may be the more important factor to watch since the trend in stocks and earnings expectations are more closely aligned with deaths than cases.

-

A second wave of deaths could lead to a second wave of declines for the economy, corporate earnings and the stock market.

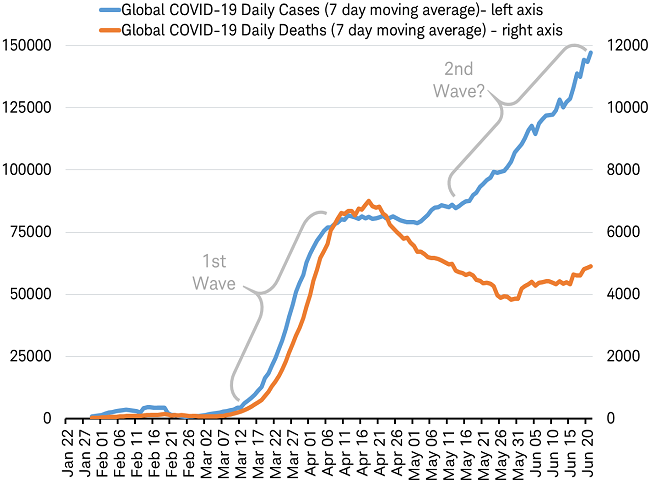

In the past couple of weeks, markets have been reacting negatively to rising new virus case data in some countries and U.S. states. This begs the question: is the world experiencing a second wave of COVID-19 cases? It may look that way in the chart below. But looks can be deceiving when it comes to the rise in new cases. More importantly, deaths have not seen the same rise. Let’s examine what might it all mean for the economy, earnings, and the stock market.

New COVID-19 cases and deaths

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

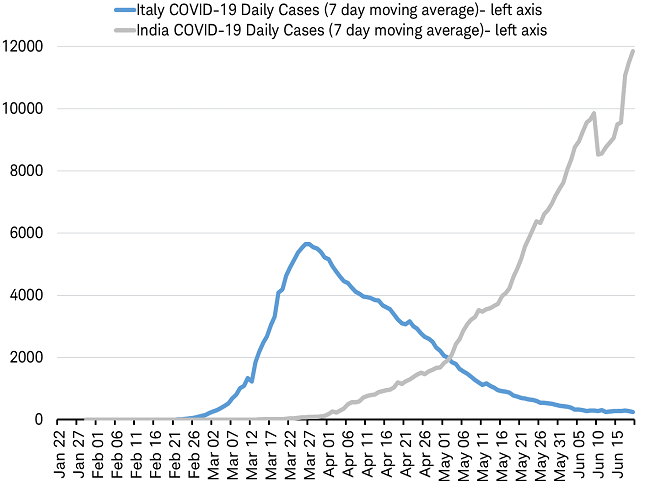

The appearance of the above chart clearly shows an uptick in new cases worldwide, but that is not the result of each country experiencing a second acceleration in new cases. Instead the pattern is caused by some countries experiencing their wave of cases later than others. This is illustrated in the chart below. Italy saw its wave peak in late March, while India saw its wave begin at that time. If we were to add these two countries together the pattern reflects the global trend in new cases in the chart above.

First waves, different timing: Italy and India

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

Second waves

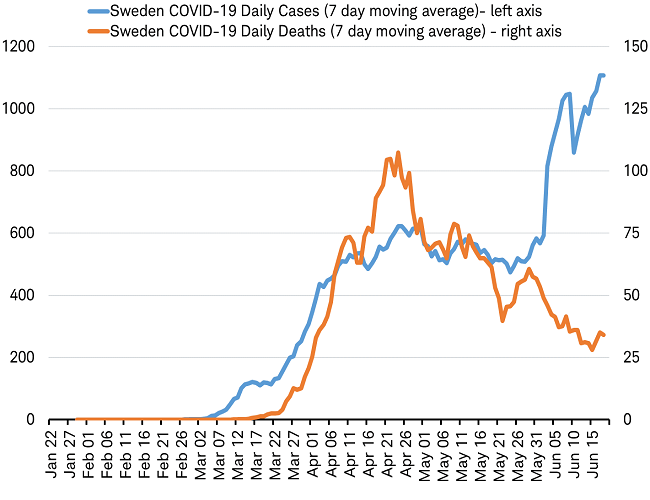

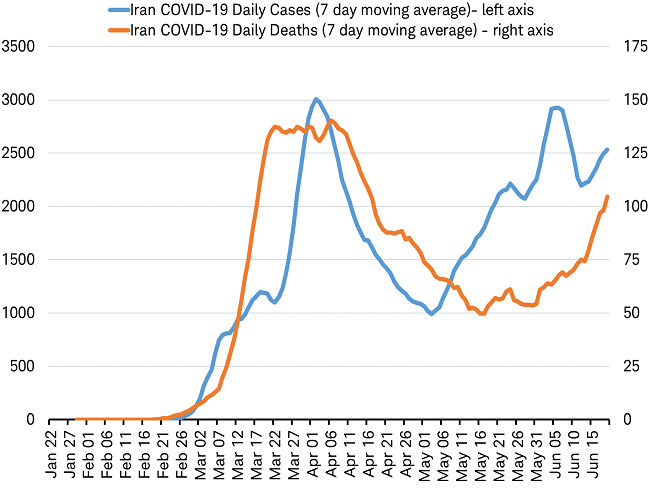

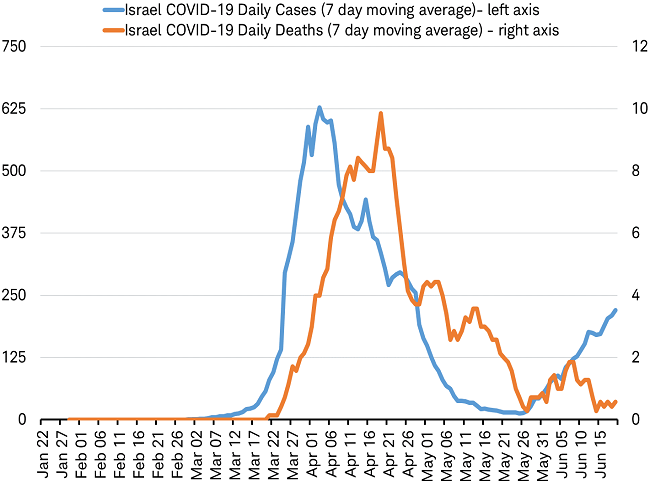

The global pattern of new cases is primarily driven by the different timing of first waves. However, there are some countries that are experiencing second waves, including Sweden, Iran, and potentially Israel. Even as the number of cases rises in these countries, the number of new deaths continues to fall (except in Iran). The trend in deaths may be the more important driver of how people and policymakers respond to a second wave.

Second wave: Sweden

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

Second wave: Iran

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

Second wave: Israel

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

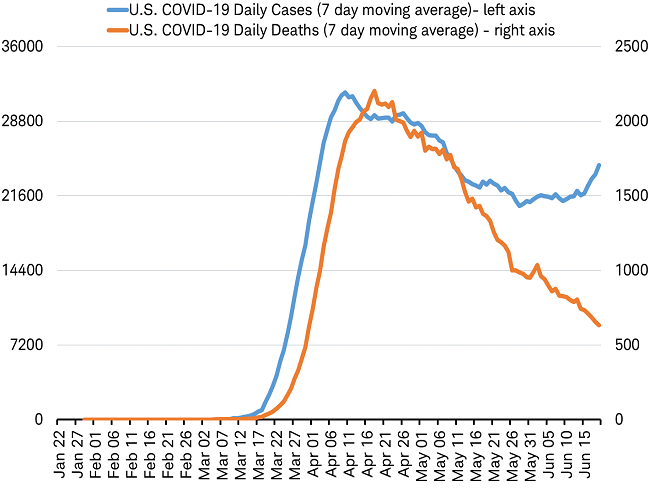

Notably, the chart of the U.S. does not seem to support an obvious second wave. Echoing the worldwide pattern, the wave of cases hit some U.S. states later than others, keeping the overall number of cases elevated. Importantly, the overall number of new deaths continues to decline.

Second wave: United States?

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

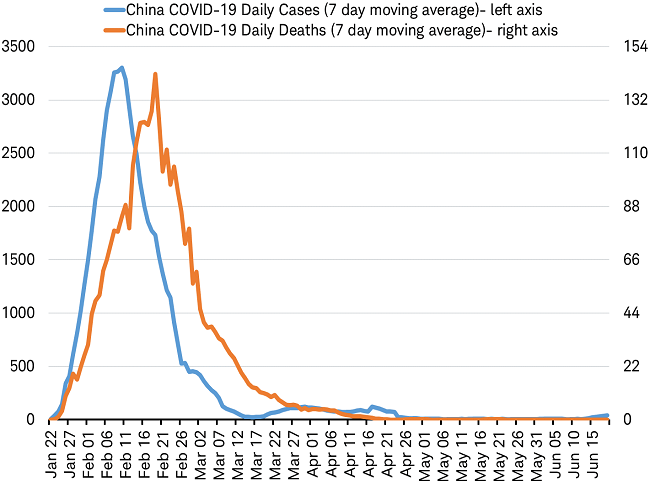

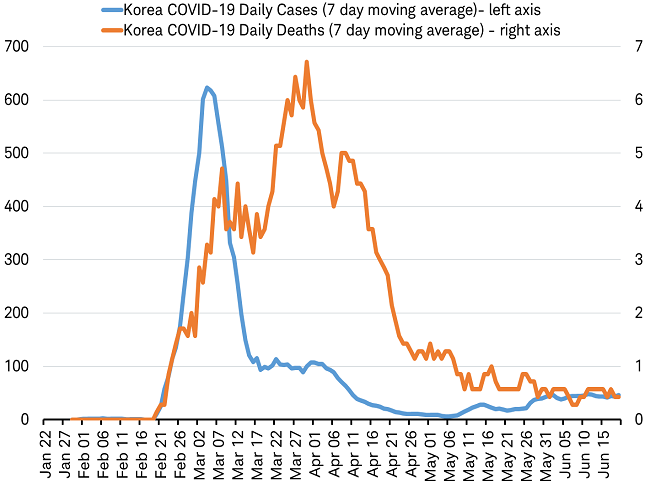

China and Korea, featured in news reports of a rise in new cases, seem to have only experienced ripples after the first wave. China in particular has taken a zero tolerance approach to any potential resurgence of the virus, instituting a second lockdown in some areas, despite the very small number of new cases.

Ripples: China

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

Ripples: South Korea

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

Impact on investors

The relatively stable pace of new deaths contrasts with the rising trend in new cases. In the U.S., demographic data from the Center for Disease Control shows that new cases in May and June are skewing towards those that are younger, rather than towards the older portion of population as seen back in April and in months prior. While daily stock market volatility in recent weeks may be influenced in part to the rising number of cases, the overall trend in stocks seems more closely aligned with deaths than new cases, as you can see in the chart below. This makes sense since it is the risk to human life that may result in a return to the economic paralysis of lockdowns or self-quarantines, rather than solely a rise in new cases.

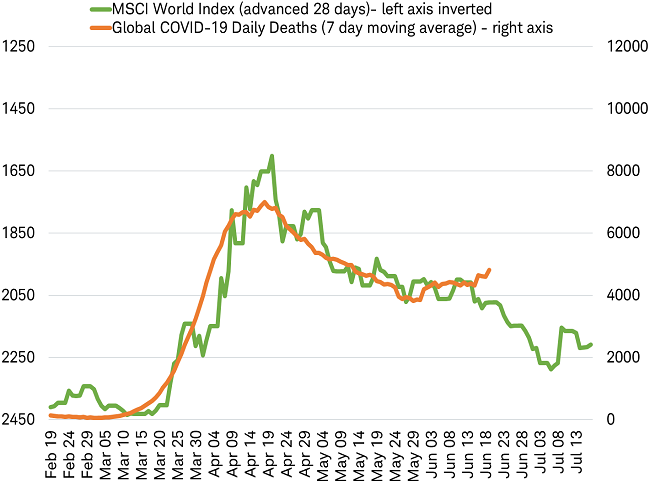

Stocks focused on deaths not cases

Source: Charles Schwab, Bloomberg data as of 6/20/2020.The MSCI World lndex is moved forward on the horizontal axis by 28 days.

Stocks seem to have been moving in advance of the trend in deaths (by about four weeks), perhaps anticipating the trend based on what was seen in countries that led the first wave of the virus (ex. China and South Korea). But this relationship is now at a critical point and poses a risk to stocks if deaths were to trend higher. Expectations of a further decline in deaths seems to be priced into stocks in recent weeks; any challenge to that expectation could trigger a sharp selloff. These concerns are not unwarranted. Signs of vulnerability in the stock market over the past two weeks include rising volatility tied to virus data. So watching the number of deaths, not new cases, may be critical in the weeks ahead.

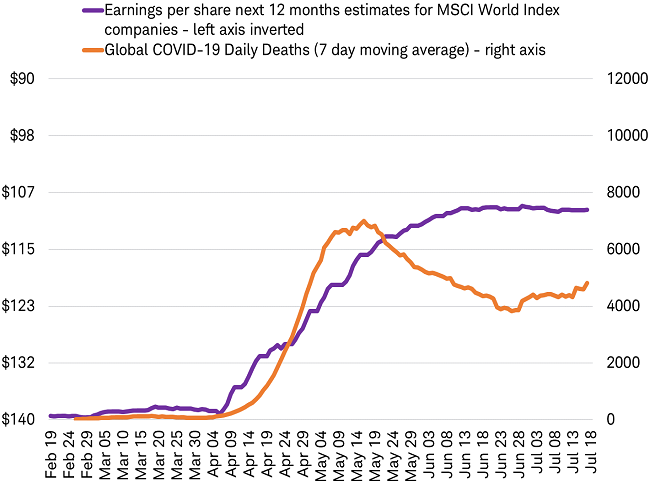

The potential impact of a second wave on corporate earnings is connected to the risk of another series of lockdowns (official or self-imposed) that would impact economic recovery. Apple’s decision last week to close stores in four states has weighed on sentiment, serving as a reminder that even in the absence of official lockdowns, closures by businesses are a risk to economic activity. Like stock price movements, analysts’ revisions to company earnings estimates seem to be focused on deaths, not new cases, as you can see in the chart below. If the number of daily deaths begin to rise to new highs, the prospects for another lockdown and the likelihood of further cuts to earnings estimates rise, as well.

Analysts’ earnings estimates stabilizing

Source: Charles Schwab, Bloomberg data as of 6/20/2020.

Although daily data on new COVID-19 cases seem to garner the most media attention, a second wave of deaths is a risk that could lead to a second wave of declines for the economy, corporate earnings and the stock market. Watching this trend in the coming weeks could be an important signal for investors.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

All corporate names and market data shown above are for illustrative purposes only and are not recommendations, offers to sell, or a solicitation of an offer to buy any security.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab