Key Points

-

Investment-grade corporate bonds: Consider focusing on average maturities of five to seven years. Credit rating downgrades are likely to continue, with the potential for some “triple B” bonds to be downgraded to junk.

-

High-yield corporate bonds: Focus on higher-rated issues, like those rated “BB/Ba” by Standard & Poor’s and Moody’s, respectively. Defaults are still likely for many of those rated “CCC/Caa” or below.

-

Preferred securities: They can still make sense for investors looking for higher income and yields, but volatility is likely to remain elevated. The risk of dividend suspension appears low for now.

-

Bank loans: Proceed with caution. We believe there is very little upside, but plenty of downside if the economic outlook deteriorates.

For the second half of 2020, we don’t expect a repeat of the first.

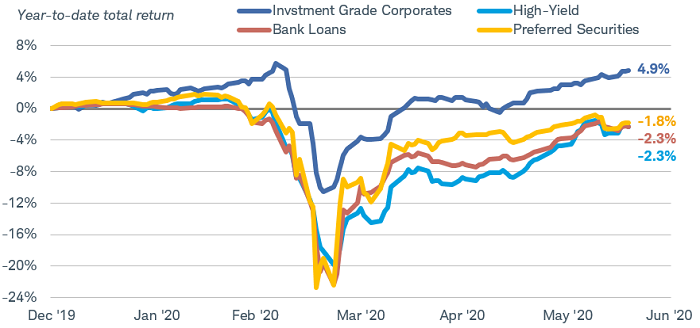

After plunging in February and March, the prices of corporate bond investments have rebounded sharply. Investment-grade corporate bonds have now delivered positive year-to-date total returns, while riskier investments like high-yield bonds, preferred securities, and bank loans are slowly clawing their way back toward zero. While total returns have been strong since the March lows, we don’t expect the strong pace to continue.

If the economic outlook holds steady or improves, corporate bond prices could move modestly higher, but the potential price appreciation likely will be limited. If the economic outlook deteriorates, however, prices could fall, but we believe that the decline would stop short of the mid-March lows due to support from the Federal Reserve. In this scenario, the lowest-rated parts of the markets would likely suffer the most.

After a steep plunge early in the year, prices have rebounded sharply

Source: Bloomberg. Total returns from 12/31/2019 through 6/18/2020. Indexes represented are the Bloomberg Barclays U.S. Corporate Bond Index, Bloomberg Barclays U.S. Corporate High-Yield Bond Index, ICE BofA Fixed Rate Preferred Securities Index, and the S&P/LSTA Leveraged Loan 100 Total Return Index. Total returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no indication of future results.

The broad view: near-term support, longer-term risks

Corporate bond prices began to tumble early in the year due to concerns about the economic impact of COVID-19. As the economy ground to a halt, the risk to corporate revenues and profits came front and center. With cash flows likely to plunge—making it more difficult for companies to make timely interest or principal payments—corporate bond prices plunged.

The main driver of the rebound was the swift and unprecedented actions from the Federal Reserve, in our view. On March 23rd, the Federal Reserve announced the launch of the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF), allowing it to buy up to $750 billion of corporate bonds and corporate bond exchange-traded funds (ETFs). The SMCCF officially began buying ETFs on May 12th and individual corporate bonds on June 16th.

After these facilities were announced, prices rose and yields dropped. Knowing that the Fed was going to purchase corporate bonds helped alleviate the concerns about companies failing to repay or refinance their debts. Before the announcement, investors were generally wary of lending to corporations given the uncertain outlook. In the weeks leading up to the decision, very few corporations were able to issue new debt (which would allow them to retire maturing debts). Since the March 23rd announcement, corporate bond issuance has boomed, with year-to-date investment-grade corporate bond new issuance already topping $1 trillion through May 2020, up 99% from the first five months of 2019.1

We believe the Fed’s support should help keep corporate bond prices supported, with some caveats:

- The investment-grade corporate bond market is receiving the most direct support from the Fed, as most of corporate bonds eligible for purchase are those rated investment grade.

- Very few high-yield corporate bonds are eligible to be purchased by the Fed—only those whose ratings were BBB-/Baa3 or higher on or after March 22nd and have since been downgraded to sub-investment grade are eligible. If a bond then gets downgraded below BB-/Ba3, it is no longer eligible to be purchased.

- Since very few high-yield corporate bonds can be purchased, we believe corporate defaults will continue to pile up. Despite the strong high-yield bond performance over the past few months, corporate defaults are rising at the fastest pace since the 2008-2009 financial crisis.

If the economic outlook deteriorates, the presence of the Fed’s corporate bond buying and commitment to helping keep the markets functioning smoothly should prevent prices from falling as sharply as they did in February and March.

While the Fed’s support has allowed corporations to issue more and more bonds, helping them shore up their balance sheets or refinance debt accordingly, it raises the risk profile of corporations over the long-run. As corporate debt grows faster than corporate profits, corporations may have a difficult time paying off their debts down the road. This has been a concern for the past few years, and the gap between corporate profit growth and corporate debt growth widened significantly in the first quarter.

The gap between corporate debt and profit growth grew even wider in the first quarter

Source: Bloomberg, using quarterly data as of 1Q 20120. FOF Corporate Business Corporate Profits Before Tax with IVA and CCadj (INCOCBCP Index) and FOF Nonfarm Nonfinancial Corp Business Credit Market Instruments Liability (CDNSCBIL Index).

Investment-grade corporate bonds

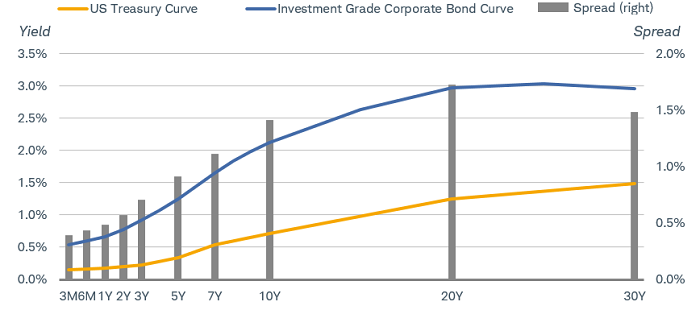

Investors should consider intermediate-term investment grade corporate bonds, preferably with average maturities in the five-to-seven-year range.

Intermediate-term corporate bonds offer a greater yield advantage over Treasuries than short-term corporate bonds. Credit spreads are the additional yields that corporate bonds offer above and beyond Treasuries with comparable maturities.

Intermediate-term investment grade corporate bonds offer higher spreads than short-term bonds

Source: Bloomberg, as of 6/18/2020. US Treasury Actives Curve and USD US Corporate IG BVAL Yield Curve (BVSC0076 Index). Past performance is no indication of future results.

Bonds with longer maturities do expose investors to more interest rate risk, or the risk that a bond’s price will fall if yields rise. However, the Federal Reserve is likely keeping interest rates near zero through the end of 2022, if not longer. That should prevent intermediate-term yields from rising much in the near-term, but it also means investors in short-term investments will likely be earning low yields for the next few years.

The Bloomberg Barclays U.S. Corporate 5-7 Year Bond Index offers a yield-to-worst of roughly 1.7%, while Treasuries with maturities of five years or less all offer yields of less than 0.4%.2 While we recognize that a sub 2% yield is likely not very attractive in absolute terms, we believe intermediate-term investment-grade corporate bonds can still make sense given the outlook for short-term interest rates to remain near zero for a few years or more.

We remain concerned about the number of “triple B” rated bonds, and believe that the credit rating agencies will likely continue to downgrade many corporations due to the challenging economic outlook. Bonds at the lowest rung of the investment-grade spectrum—those rated BBB-/Baa3 by Standard & Poor’s (S&P) and Moody’s, respectively—are the most likely to be downgraded and become “fallen angels.”

A fallen angel is a corporate bond that was initially rated investment grade but was downgraded to sub-investment grade, or “junk.” A junk bond has a greater likelihood of default and generally experiences more volatility than an investment-grade bond. Given that risk, investors with more conservative or moderate risk tolerances should reduce exposure to those bonds with low “triple B” ratings.

High-yield corporate bonds

Investors looking to take additional risks to earn higher yields may consider high-yield bonds, but we’d prefer those with relatively high credit ratings, like those rated in the BB/Ba range by S&P or Moody’s, respectively. One way to accomplish this is by investing in fallen angels.

While it may sound counterintuitive to suggest fallen angels, given that we are highlighting their risks for investment grade bond investors, we think they can make sense in the broader context of high-yield bond investing. In other words, if you’re considering high-yield bonds, fallen angels are worth a look.

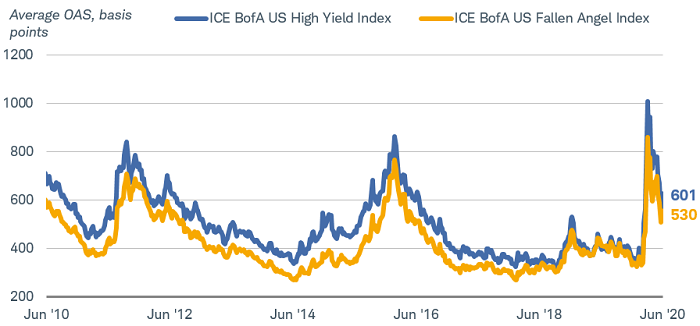

Fallen angels generally have higher credit ratings than the broad high-yield market. Over 90% of the ICE BofA US Fallen Angel High Yield Index is rated BB/Ba or higher, compared to just 55% for the ICE BofA US High Yield Index.3 Despite the large gap in credit quality, fallen angel credit spreads are not much lower than the broad market.

Fallen angel spreads are not much lower than the broad market, despite having higher average credit ratings

Source: Bloomberg, using weekly data as of 6/18/2020. Option-adjusted spreads (OAS) are quoted as a fixed spread, or differential, over U.S. Treasury issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan. Past performance is no indication of future results.

Historically, we found that the fallen angel index has generated higher annualized total returns than the broad high-yield index over the last 5-, 10- and 20-year periods. We believe this is due to a potential overreaction that occurs when a bond gets downgraded to junk—its price might drop more than warranted simply because it’s exiting the investment-grade universe and entering the high-yield universe. An index or fund that tracks fallen angels may therefore be able to invest at attractive prices relative to comparably rated high-yield bonds.

There are risks to investing in fallen angels. First and foremost, the outlook for fallen angels is likely challenging given the downgrade that led to its fallen angel status. It’s also a highly concentrated market, with the fallen angel index holding roughly 300 issues, compared to almost 2,000 issues for the broad high-yield index. If just one issuer in the fallen angel index inches closer and closer to default, for example, it will likely pull down the index more so than the broad high-yield index. Finally, while fallen angels have posted higher average annualized returns than the broad high-yield index, they’ve done so with more volatility and larger short-term drawdowns.

A key reason why we suggest high-yield investors move up in credit ratings, however, is that defaults are likely to continue. Both Moody’s and S&P are forecasting the trailing 12-month speculative grade default rates to rise to more than 12%.4 Bonds with the greatest likelihood of default are those with the lowest credit ratings—like those rated low single “B” or below, but especially those with “triple C” ratings.

Preferred securities

Preferred securities appear relatively attractive for those investors looking for higher income, but they should always be considered long-term, aggressive investments.

We don’t believe there’s much room for price appreciation, but the yields offered remain some of the highest within the fixed income universe.

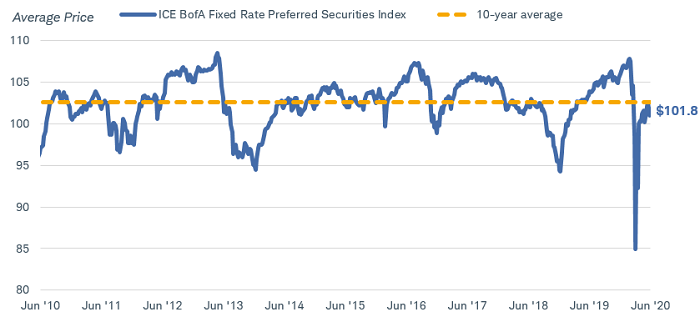

As the chart below illustrates, prices have rebounded sharply from the March lows, but are still just below the 10-year average. We believe the challenging economic outlook and low level of yields may prevent prices from rising back to pre-COVID-19 levels. Because preferreds have long maturities, or no maturity dates at all, they tend to be sensitive to fluctuations in long-term interest rates. While we don’t expect long-term Treasury yields to suddenly surge, we do believe they may move modestly higher in the second half of the year, potentially pulling preferred securities’ prices lower.

Preferred security prices are just below their 10-year average

Source: Bloomberg, using weekly data as of 6/18/2020. Past performance is no guarantee of future results.

We believe the risk of dividend suspension is low due to the strength of bank balance sheets and the likelihood that the worst of the economic downturn is behind us. Banks and other financial institutions are generally the largest issuers of preferreds. While bank profits are likely to remain challenged to the economic impact of COVID-19 and the low level of interest rates, their balance sheets are still in good shape due to tighter financial regulations put in place after the global financial crisis.

Bank loans

We see very little room for bank loan prices to rise, and their coupon payments have generally dropped as a result of the Fed’s near-zero interest rates. While investors may consider bank loan as a complement to a well-diversified fixed income portfolio, risks remain that could lead to potential price declines or heightened volatility.

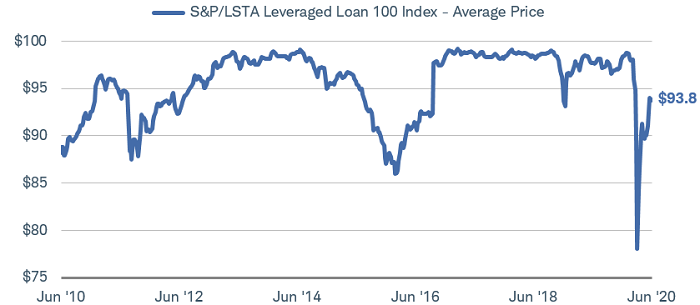

Bank loan prices have rebounded sharply from the March lows. As the chart below illustrates, the average price of the S&P/LSTA Leveraged Loan Index generally peaks at around $99, meaning there’s not much room for prices to rise, even with a rosy outlook. With the challenging economic outlook today and likelihood that defaults continue to rise, bank loan prices may be stuck in a range or may modestly fall as defaults pick up. Keep in mind that bank loans are sub-investment grade, aggressive investments. Our caution regarding the likelihood of high-yield defaults for the rest of the year is also a concern with bank loans. According to Moody’s, the trailing 12-month speculative grade default rates for high-yield bonds and loans were 5.9% and 5.8%, respectively, through the end of May. Despite loans having seniority to bonds and being collateralized, they have still been defaulting at a high rate.

Meanwhile, due to their floating coupon rates, income payments have likely declined as the Fed cut rates back to near zero. With the Fed likely keeping rates anchored for the next few years, coupon rates are unlikely to rise anytime soon.

Bank loan prices are up sharply since March

Source: Bloomberg, using weekly data as of 6/18/2020. Past performance is no guarantee of future results.

What to do now

Investors should consider these various investments—cautiously. Given the challenging economic outlook and high level of uncertainty, we believe bouts of volatility are possible, albeit not to the level witnessed in February and March. It’s always important to match investments with risk tolerance, and to keep these investments in line with strategic weights, especially riskier investments like high-yield bonds, preferred securities, and bank loans. We believe those more aggressive investments should serve as a complement to a well-diversified, high quality fixed income portfolio, not a substitute.

1 Source: Securities Industry and Financial Markets Association, US Corporate Bond Issuance through May 31, 2020.

2 As of June 18, 2020.

3 As of June 18, 2020

4 Moody’s Investors Services, “Default Trends—Global, May 2020 Default Report,” June 10, 2020 and Standard and Poor’s, “The U.S. Speculative-Grade Corporate Default Rate Is Likely to Reach 12.5% By March 2021,” May 28, 2020.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

The ICE BofA US Fallen Angel High Yield Index is composed of below-investment-grade corporate debt instruments denominated in U.S. dollars that were rated investment grade at the time of issuance.

The ICE BofA US High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0620-0HWR)

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab