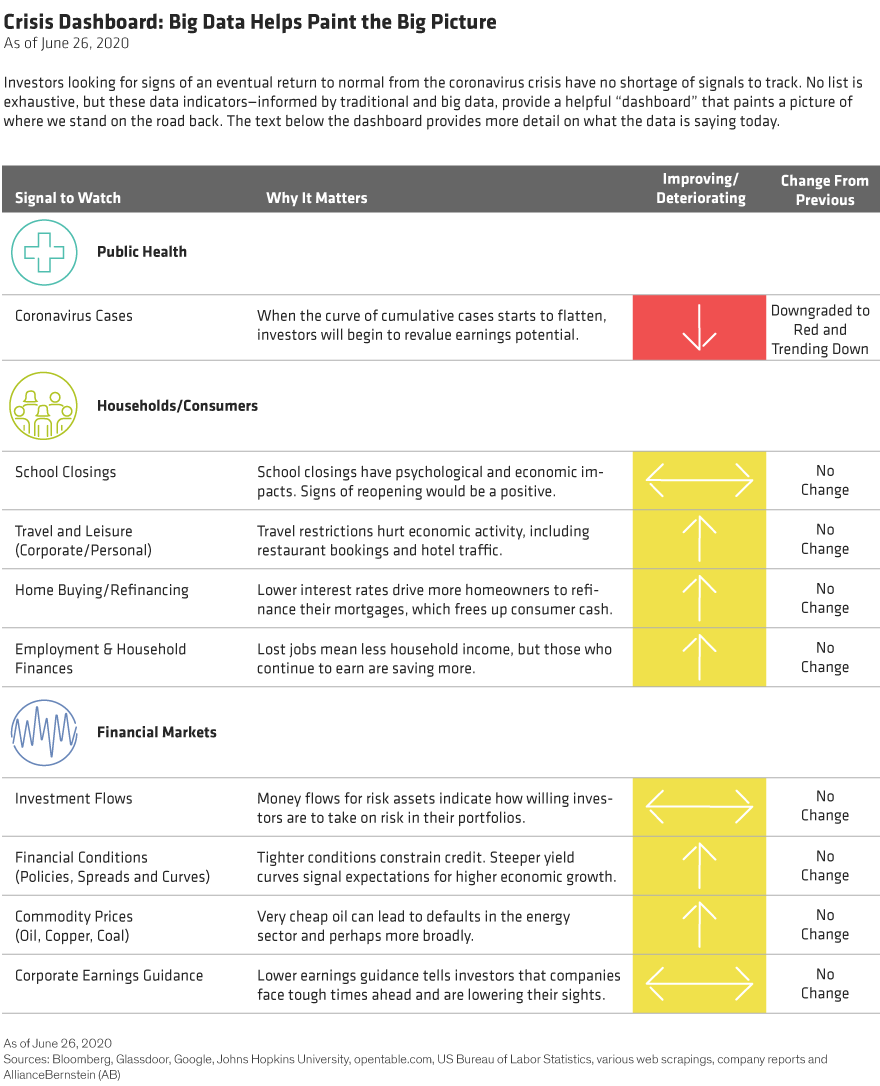

Our crisis dashboard includes signals from three areas: 1) public health, 2) the consumer sector and 3) financial markets. By pulling big data from traditional sources (earnings growth and gross domestic product, for example) and nontraditional sources (like Google Trends and Glassdoor), we can create a better mosaic of the road back. Public health, of course, is the key: until there’s a vaccine, the cascading impact of the virus may continue.

The dashboard color codes (red, yellow or green) indicate the current state of each signal, while the arrows indicate the trend (improving, deteriorating or unchanged).

The dashboard has remained fairly steady since our last update, with one notable exception: the public health front. The number of coronavirus cases continues to climb, and the R0 rate, the average number of people infected by one person, is up. That’s concerning, since so much depends on progress in the fight against COVID-19. We’ve downgraded our public health indicator to red and trending down.

Public Health

- Globally, the number of confirmed coronavirus cases continues to rise—it’s currently over nine million. Cases are rising in some part of the world, such as Brazil and a resurgence of cases in the US.

Employment & Household Finances:

- Job postings have returned to somewhat normal levels versus last year. US jobless claims have slowed, though 47 million people have filed for unemployment benefits over the last 14 weeks.

- Nearly 60 million jobs across the European Union and UK are still at risk.

- Credit card spending data shows a rebound to just below 2019 levels, but the recovery seems to be slowing.

- US personal savings as a percentage of disposable income remained elevated in May at 23.2%, though down from 32.2% in April.

- In Europe, it’s estimated that household savings rates could increase by as much as 20 percentage points to 36% on average in the second quarter, according to Eurostat. That’s a lot of precautionary savings that could represent pent-up demand.

- China’s personal savings rate is expected to reach 34% the end of 2020 (Source: Trading Economics).

Financial Markets

Investment Flows:

- Based on Simfund and ICI data, about $39 billion has moved into bond funds since the beginning of June, as investors shifted out of money-market accounts to slightly riskier but higher-paying investments. Equity flows remain largely flat.

Financial Conditions:

- High yield spreads widened over the past week to 605 basis points (556 basis points excluding energy).

- New issues totaled $15.4 billion this week, taking this month’s total issuance to $50.6 billion, a new all-time record that beats the $46.9 billion in September 2013.Year-to-date issuance is at a record $205 billion, about 71% more than the same point last year, and only $55 billion short of full-year 2019.

- Year to date, 51 companies, totaling $92.3 billion in bonds and loans, have defaulted or completed a distressed exchange. That makes 2020 already the second-highest calendar-year default total on record, trailing only the $205 billion in 2009. US high-yield bond default rates have risen to a 10-year high of 6.11%.

- The US Treasury yield curve is largely unchanged from a month ago.

Commodity Prices:

- Coal consumption in China is slowly picking up again—it’s up about 10% from last year.

- Oil prices are finally stabilizing, having climbed to approximately $40 per barrel, a high since early March.

- Copper prices are also stabilizing (around $2.64 per pound), after rising from March’s levels.

Corporate Earnings Guidance:

- 2020 earnings-per-share (EPS) estimates have declined considerably. However, the market is focusing on 2021 earnings, with stocks trading at a multiple of about 19 times.

Scott Krauthamer is Global Head of Product Management and Strategy at AB. Jonathan Berkow is Senior Quantitative Research Analyst and Alternative Data Lead for Equities at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein