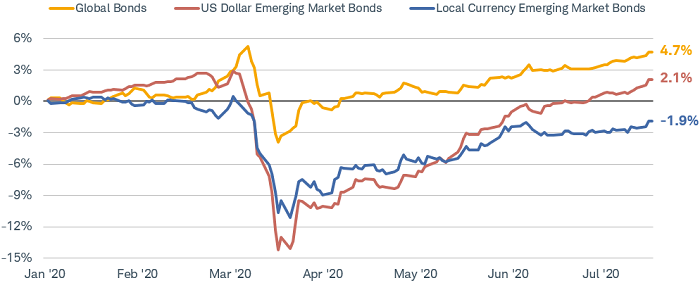

Emerging-market (EM) bonds have been exceptionally volatile since the onset of the COVID-19 crisis. In March, prices dropped 16% in a matter of weeks, resulting in the worst monthly decline since 2008.1 After central banks stepped in to provide liquidity, EM bonds rebounded sharply in the second quarter. Year to date, the total return for U.S.-dollar-denominated EM bonds is up 2.1%, while local-currency bond total return is down 1.9%.

Emerging-market bond total return has been volatile

Source: Bloomberg Barclays Global Aggregate Total Return Bond Index, Bloomberg Barclays Emerging-Market U.S. Dollar Aggregate Total Return Bond Index and Bloomberg Barclays Emerging-Market Local Currency Government Total Return Bond Index. Daily data as of 7/22/2020. Past performance is no guarantee of future results.

Weighing the ongoing risks of the virus against the extra yield the bonds provide, begs the question: Is an allocation to EM bonds worth the risk? The short answer is yes—but only for investors with the tolerance and capacity for risk. We believe an allocation to EM bonds can still provide income and diversification to a fixed income portfolio, but it is likely to come with a lot of volatility.

While emerging-market bonds have rebounded off the depressed lows of March, spreads are still generally wide, presenting opportunities for those willing and able to accept the risks. EM bonds are not an asset class for the faint of heart—those with little tolerance or capacity for the volatility, lack of liquidity, and potential loss should turn back now. For those of you who are still interested, here’s what you need to know.

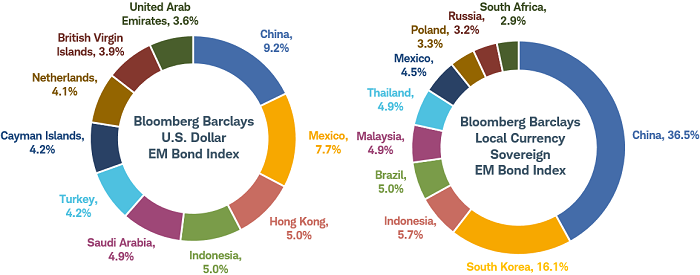

The emerging-market debt universe has grown

The universe of emerging-market bonds has grown rapidly over the years—from $885 billion in 2008 to $2.7 trillion in 2020.2 Sovereign bonds—those issued by governments—comprise the bulk of the market, but issuance of corporate bonds is growing and now makes up 26% of the universe. With interest rates in major developed countries near zero or even negative, EM countries and corporations have found eager buyers of their bonds as investors search for higher yields.

Over the years, China has issued an increasing amount of debt, dwarfing the rest of the emerging-market debt universe, especially in the case of local-currency sovereign bonds. Also worth noting is that the USD-denominated index has more exposure to oil-producing countries.

The USD EM bond index and the local-currency EM bond index are very different

Note: Shows the top 10 weights by country in each respective index.

Source: Bloomberg Barclays Emerging-Market U.S. Dollar Aggregate Total Return Bond Index, as of June 2020 (left chart). Bloomberg Barclays Emerging-Market Local Currency Government Total Return Bond Index, as of June 2020 (right chart).

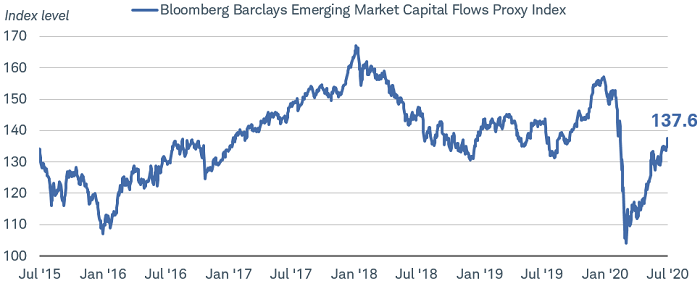

What drives EM debt performance?

The recent driver of emerging-market debt performance was the halt to economic activity to address the coronavirus. The steep decline in EM bond prices and rise in yields during the first half of the year illustrates one of the vulnerabilities of the asset class. In periods of disruption or crisis, investors flee due to concerns that some emerging-market governments and corporations have fewer resources to deal with a sudden shock to economic growth. As a result, their currencies often drop sharply in a crisis as investors seek safer, more-liquid investments. As the chart below shows, investors raced to pull their money out of emerging markets in March, exacerbating the already declining emerging-market debt returns.

Capital flows into emerging markets dropped in March

Source: Bloomberg. Bloomberg Emerging-Market Capital Flows Proxy Index. Daily data as of 7/21/2020.

Concern over high, unsustainable debt levels is another factor to watch. There is no hard-and-fast rule on what level of debt-to-gross domestic product is acceptable for emerging-market countries—it largely depends on the level of stability in a country’s economic infrastructure. For example, Turkey, South Africa and Brazil experienced huge currency declines and portfolio outflows earlier this year amid concern about high debt levels and/or instability in their economies, whereas the more economically stable EM countries in Asia and Eastern Europe fared better.

Whether the debt is denominated in U.S. dollars or in the issuer’s local currency, the direction of the U.S. dollar matters. For USD-denominated debt, a rise in the dollar makes it more expensive for the issuer to service the debt. If the dollar is rising and emerging-market currencies are weakening, the issuer needs to pay more to acquire those dollars to repay bondholders. This increase in debt servicing costs can lead to defaults.

Debt issued in local currencies poses a different risk. While a weaker currency won’t necessarily have a direct impact on an issuer’s ability to repay debt in its own currency, it can lead to a drop in value when translated back into U.S. dollars. This will lead to lower returns for the local-currency bonds. Conversely, if the dollar falls, the value of local currencies may rise, leading to higher returns for the local-currency bonds.

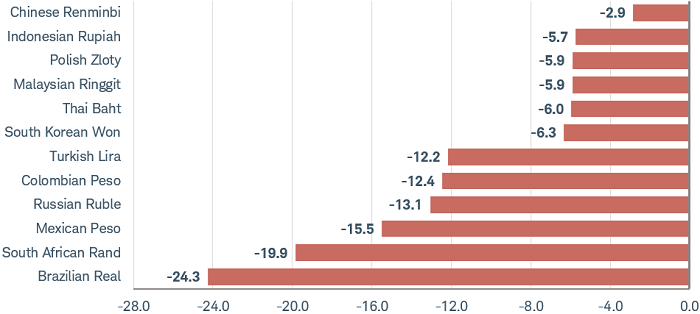

Debt issued in local currencies fluctuates based on the value of the U.S. dollar

Source: Bloomberg. World Currency Ranker (WCRS). Date range 12/31/2019-5/27/2020. Past performance is no guarantee of future results.

Emerging-market currencies pulled back as much as -24% against the U.S. dollar in the first half of the year. These declines had a negative impact on both USD-denominated and local-currency-denominated EM debt.

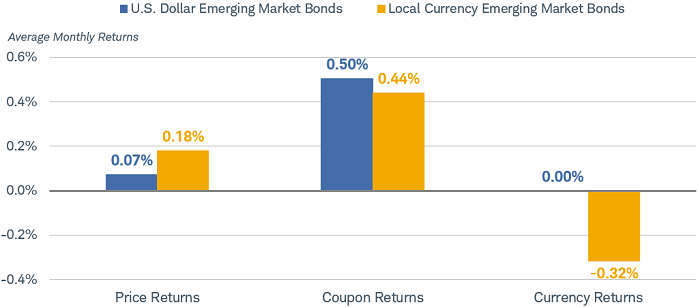

The relatively high coupons on EM bonds are usually the largest contributor to returns, especially when reinvested over time. Compared to the near-zero coupons on many developed market bonds, this feature can be important for income-oriented investors that can handle the added volatility.

Coupon returns on EM bonds are usually the largest contributor to returns

Note: A full market cycle, peak to peak, was used. The dates of the cycle are December 2007 (the end of the previous recession) to February 2020 (the beginning of the most recent recession).

Source: Bloomberg and National Bureau of Economic Research (NBER). The Bloomberg Barclays US-Dollar Denominated Emerging-market Index and the Bloomberg Barclays Local Currency Sovereign Emerging-market Index average monthly returns. Monthly data as of February 2020. Past performance is no guarantee of future results.

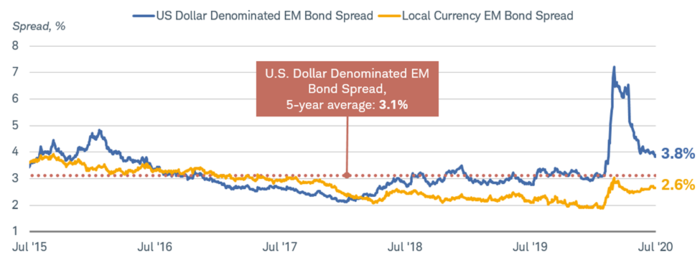

Finally, yield spreads—the additional yield EM bonds provide over Treasuries of comparable maturity—averaged 3.1% for U.S. dollar-denominated emerging-market bonds in the five years leading up to the onset of the coronavirus crisis. As you can see in the chart below, after spiking up to as much as 7%, spreads are back down to 3.8%, but still elevated. The above-average yield may present an attractive entry point for investors interested in gaining exposure to USD-denominated emerging-market debt. Local-currency emerging-market sovereign bonds, however, yield just 2.6% over Treasuries, making them appear less attractive on a risk/reward basis.

Although U.S. dollar EM bond spreads have narrowed, they’re still attractive relative to Treasuries

Source: Bloomberg. Bloomberg Barclays Emerging Market U.S. Dollar Aggregate Option Adjusted Spread Index, and the spread between Bloomberg Barclays U.S. Aggregate Treasury Yield to Worst Index and Emerging Market Local Currency Government Yield to Worst Index (EMUSOAS Index, LUATYW Index, and EMLCYW Index). Daily data as of 7/22/2020. Past performance is no indication of future results.

Portfolio considerations: liquidity and correlations

We classify emerging-market bonds in the “aggressive income” segment of the market because they are typically more volatile, more likely to default, and less liquid. The lack of liquidity—that is, the ability to buy or sell a bond at a reasonable price in a reasonable time frame—can be challenging, especially when the market is under stress. We suggest investors allocate no more than 20% of their investments to EM bonds and use mutual funds or exchange-traded funds (ETFs) to gain exposure, due to their diversification benefits.

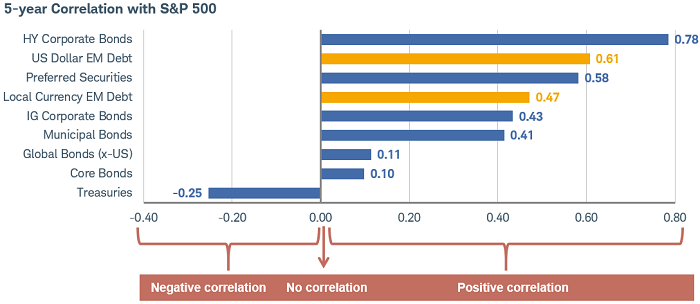

Another portfolio consideration is correlations. EM bonds tend to be more highly correlated with equities than with U.S. Treasuries. The correlation over the last five years between emerging-market debt and equities ranges from 47% to 61%, depending on whether local-currency or USD-denominated EM debt is used. That’s not quite as high a correlation as high-yield bonds, but it’s still significant. Emerging-market bonds can offer similar returns to high-yield debt, but with lower correlations to U.S. equities.

EM bonds tend to be more highly correlated with equities than with U.S. Treasuries

Note: Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated. Correlations shown represent an equal-weighted average of the correlations of each asset class with the S&P 500 during the five-year period between June 2015 and June 2020.

Source: Indexes representing the investment types are: Bloomberg Barclays U.S. Aggregate Bond Index (U.S. Agg), Bloomberg Barclays U.S., Treasury Inflation-Protected Securities Index (TIPS), Bloomberg Barclays Municipal Bond Index (Municipals), Bloomberg Barclays U.S. Corporate, Bond Index (IG Corporates), Bloomberg Barclays Emerging-market USD Index (USD EM), ICE BofA Merrill Lynch Preferred Stock Fixed Rate Index (Preferreds), Bloomberg Barclays U.S. Corporate High-Yield Bond Index (High-Yield), and the Bloomberg Barclays U.S. Treasury Long Bond Index (Long Treasuries). Diversification strategies do not ensure a profit and do not protect against losses in declining markets. Past performance is no guarantee of future results.

What investors can do now

After the steep decline and subsequent recovery in EM bonds over the past six months, the market appears to have priced in the sudden onset of COVID-19 and central bank responses. For U.S. dollar-denominated EM bonds, yield spreads are still above the five-year average that prevailed prior to the crisis, providing a relatively attractive entry point.

If the coronavirus crisis abates, we would expect that spread to decline further. However, to a large extent, we believe the markets are at the mercy of the virus, which means volatility is likely to remain high and the risk of periodic selloffs is elevated. For those willing and able to accept the risks, we prefer U.S. dollar-denominated EM bonds over local-currency debt.

1 Source: Bloomberg Barclays EM USD Aggregate Total Return Index

2 Source: Bank for International Settlements Debt Statistics.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

The Bloomberg Emerging Market Capital Flows Proxy Index is a daily composite index of the performance of four asset classes that appears to mimic the flow of money into and out of emerging markets.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging-markets may accentuate these risks.

Currencies are speculative, very volatile and are not suitable for all investors.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.