U.S. stocks and economy: Climbing out of contraction

The deepest point of economic contraction looks to be behind us, as U.S. gross domestic product (GDP) growth fell at a quarter-over-quarter annualized -32.9% rate in the second quarter. Estimates for third-quarter growth are pointing to a double-digit gain, but they’ve come down of late, as a midsummer resurgence in the virus and subsequent re-closings of some areas of the economy have halted activity.

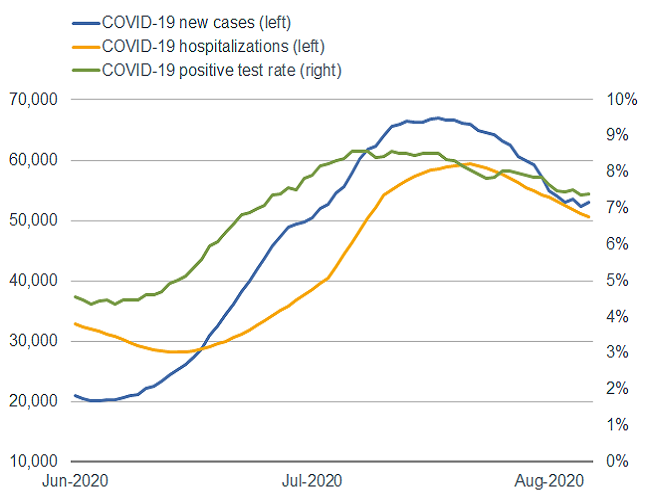

Even though certain high-frequency data—such as TSA traveler throughput, initial jobless claims, and OpenTable seated diners—haven’t improved markedly, the threat of the virus has started to recede. In relative terms from the spike in late July, new COVID-19 cases, hospitalizations, and the positivity rate have trended down, as you can see in the chart below.

The virus’ trajectory in the United States is improving

Source: Charles Schwab, COVID Tracking Project, as of 8/11/2020.

We’ve continued to affirm that much of the economic recovery is dependent on the virus—both its trajectory as well as progress on a vaccine or other therapeutic remedies. Yet despite a slowdown in the spread, some state and local governments have already halted or reversed their reopening plans, while businesses and consumers continue to decide how soon to reopen and how much to go out, respectively—all substantial risks to the recovery.

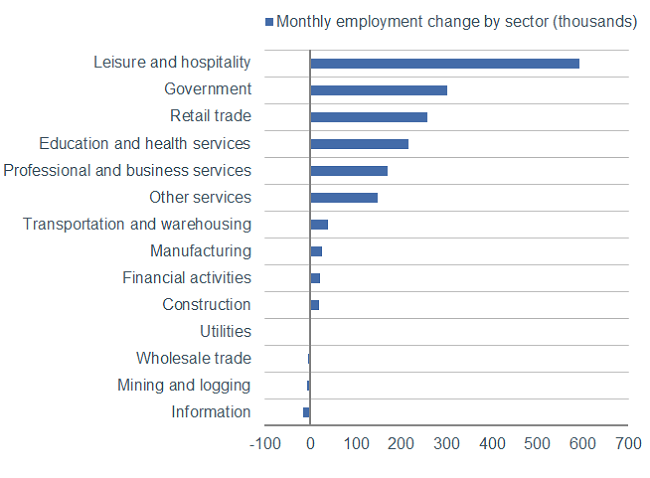

Fortunately, even staggered reopening efforts across the country have brought back a considerable number of jobs. The July nonfarm payrolls report from the Bureau of Labor Statistics showed an impressive gain of 1.76 million jobs—which beat the estimate of 1.48 million—and a decrease in the unemployment rate from 11.1% in June to 10.2% in July. Notably, as you can see in the chart below, some of the hardest-hit sectors during the depths of the crisis gained the most.

July’s increase in nonfarm payrolls favored the hardest-hit sectors

Source: Charles Schwab, Bureau of Labor Statistics (BLS), as of 7/31/2020.

The jobs report isn’t without caveats, the first being the slowdown in the pace of gains. Even though monthly changes have made the recovery look like a “V,” the level of payrolls is still nearly 13 million below the pre-pandemic peak. Hours worked fell in July, and there are still nearly 31 million individuals collecting some form of weekly unemployment insurance. Given the gap between less-rosy higher-frequency data (such as initial jobless claims) and the BLS report, future gains in the labor market may be more muted.

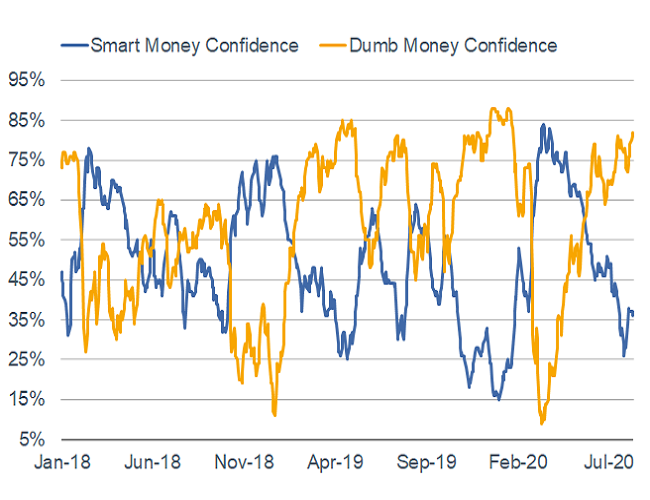

U.S. stocks have faced multiple headwinds of late, but none have been strong enough to derail the rally. Most recently, Congress has thus far failed to reach an agreement on an extension of fiscal relief, which stands to dent consumption and income for millions of Americans. Yet investors have paid more attention to the liquidity provisions from the Federal Reserve (on top of what Congress has already spent), which has kept SentimenTrader’s “Dumb Money” in extreme optimism territory for the past month.

Source: Charles Schwab, SentimenTrader, as of 8/12/2020. Confidence Indexes are presented on a scale of 10% to 90%. Past performance is no guarantee of future results.

The good news for now is that the “Smart Money” (a non-contrarian indicator) is not nearly as pessimistic as it was before the bear market selloff. Yet that doesn’t mean investor sentiment isn’t looking a bit frothy—making stocks increasingly vulnerable to a pullback associated with any negative virus- or economic-related catalyst.

Global stocks and economy: Diverging recoveries

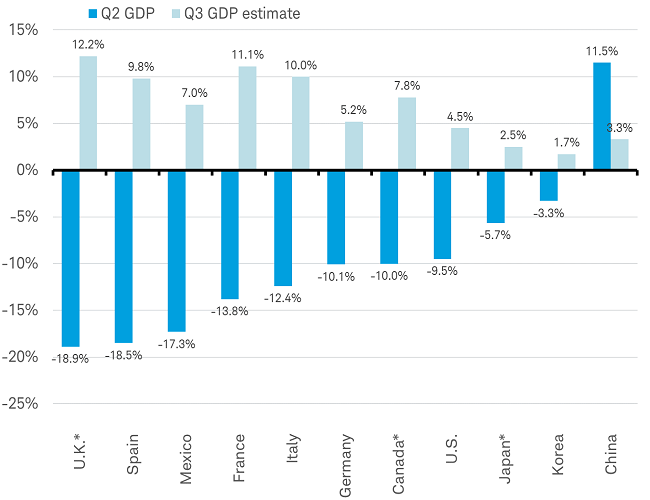

The deep global recession seen in the recently released second-quarter GDP reports for many countries reveal a wide range of severity by country, from a nearly -20% quarter-over-quarter drop in the United Kingdom to an +11.5% quarter-over-quarter rise in China (which felt the brunt of COVID-19 related shutdowns in the first quarter). Less-restrictive lockdowns helped the U.S. post a better-than-average -9.5% quarter-over-quarter decline (-32.9% when the quarter is annualized).

GDP recession and rebound varies widely by country

*U.K., Canada and Japan have estimates for Q2 GDP.

Q3 GDP estimates are from Bloomberg-tracked economists’ consensus. Source: Charles Schwab, Bloomberg data as of 8/6/2020.

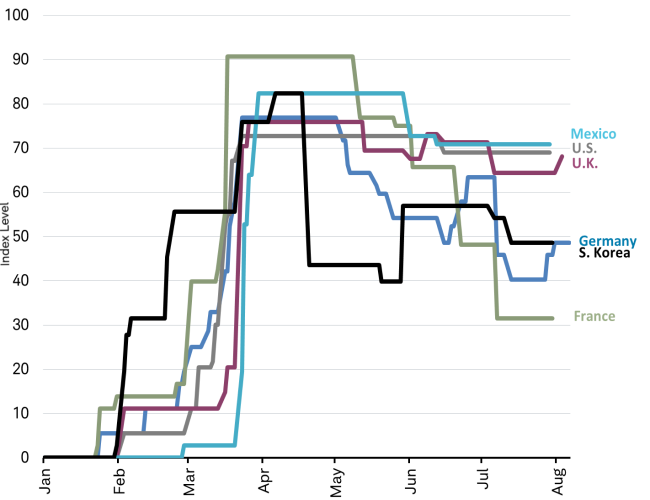

Looking ahead to the third quarter, relative GDP growth may again be dependent upon the severity of the pandemic lockdowns. We might see stronger rebounds in Europe and Asia than in the Americas, based on the easing of COVID-19 lockdown stringency measures tracked by the Oxford University Stringency Index. Economic performance in both China and South Korea was aided by substantial easing of containment measures during the second quarter as the virus was brought under control. At the other end of the scale, second-quarter lockdowns were most severe in European countries, such as Germany and France, which provoked sharp drops in economic output. Any rebounds in third-quarter GDP may benefit from the decline in restrictive measures by more than half from their peak in Germany and France, but could be at risk where restrictive measures have remained elevated, as seen in the U.S., UK, Mexico and Canada.

Oxford University Stringency Index reveals differing COVID-19 lockdowns by country

Source: Charles Schwab, Bloomberg data as of 8/6/2020.

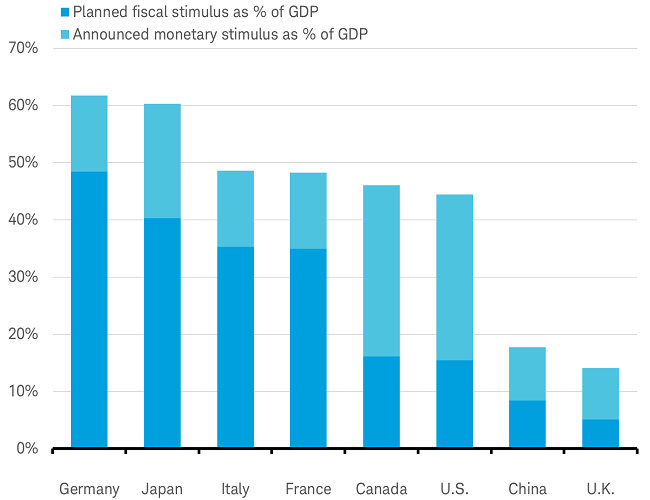

Third-quarter GDP may also rebound in economies with strong and enduring policy stimulus. The combination of fiscal and monetary stimulus as a percentage of GDP, reflected in the table below, suggests that recoveries in Europe are well supported. On the other hand, the expected strong rebound in the U.K. is challenged by weak policy support and intense lockdowns. Similar circumstances apply to India, Mexico and other South American countries. An exception is China’s fading stimulus, a reflection of the country’s already well-advanced recovery.

Policy support is massive, but varies widely by country

Source: Charles Schwab, data totaled from various official reports and announcements issued from 2/1/2020 through 8/6/2020.

The synchronized global recession in the second quarter may be turning into a divergent recovery for the third quarter and beyond. A widening divergence may lead to a widening spread of stock market performance by country and could mean the overall stock market struggles to make further gains.

Fixed income: Where do bond yields go from here?

Bond yields are hovering near record lows. In recent weeks, the pace of decline has slowed, but the trend is still lower for yields of all maturities. In the Treasury market, short-term interest rates are pinned near zero by the Federal Reserve’s policy, while 10-year yields are trading at just 0.55%. Moreover, real bond yields—yields adjusted for inflation—are now in deeply negative territory.

Real 10-year Treasury yields continue to hit new all-time lows

Source: Federal Reserve Bank of St. Louis. 10-Year Treasury Inflation-Indexed Security, Constant Maturity, Percent, NSA (DFII10) and 10-Year Treasury Constant Maturity Rate, NSA (DGS10). Daily data as of 8/10/2020.

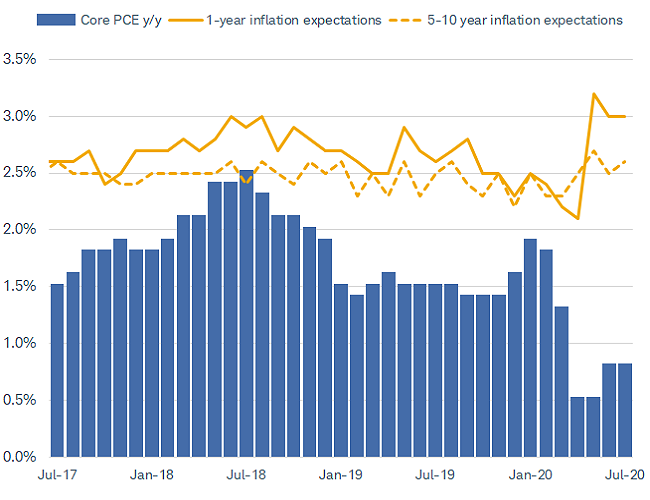

With the economy having fallen into a steep decline in the second quarter due to the coronavirus crisis and the pace of recovery in question, low yields are to be expected. Yet at the same time, inflation expectations are rising, suggesting investors are concerned that the Fed’s aggressive response to the pandemic may be sowing the seeds of inflation longer-term. Whether expectations are measured by the implied future inflation rates in the Treasury Inflation-Protected Securities (TIPS) market or surveys, the trend is higher.

Unrealistic inflation expectations

Source: Bloomberg. U.S. Personal Consumption Expenditures Chain Type Price Index YoY SA (PCE DEFY Index) University of Michigan 1-year inflation expectations (CONSEXP Index) and 5-10 year inflation expectations (CONSP5MD Index). Monthly data as of 7/31/2020.

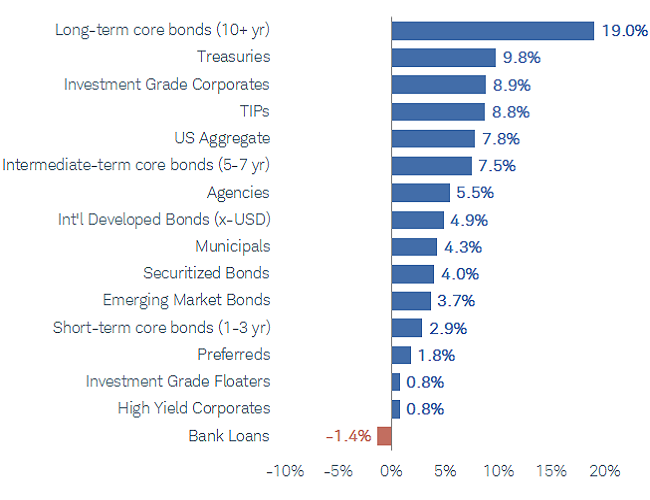

Bond investing in this environment is challenging. Long-term bonds, which have posted strong returns year to date, would continue to outperform if yields continue to fall. However, if inflation begins to rebound, as expectations suggest, then a rebound in yields is a risk.

Fixed income total returns by asset class, year-to-date

Source: Bloomberg. Returns from 12/31/2019 through 8/7/2020. Indexes representing the investment types are: US Aggregate = Bloomberg Barclays U.S. Aggregate Index; Short-term core = Bloomberg Barclays U.S. Aggregate 1-3 Years Bond Index; Intermediate-term core = Bloomberg Barclays U.S. Aggregate 5-7 Years Bond Index; Long-term core = Bloomberg Barclays U.S. Aggregate 10+ Years Bond Index; Treasuries = Bloomberg Barclays U.S. Treasury Index; Municipals = Bloomberg Barclays US Municipal Bond Index; Investment Grade Corporates = Bloomberg Barclays U.S. Corporate Bond Index; HY Corporates = Bloomberg Barclays US High Yield Very Liquid (VLI) Index; Preferreds = ICE BofA Merrill Lynch Fixed Rate Preferred Securities Index; Int'l Developed (x-USD) = Bloomberg Barclays Global Aggregate ex-USD Bond Index; Emerging Market USD = Bloomberg Barclays Emerging Markets USD Aggregate Bond Index; TIPS = Bloomberg Barclays U.S. Treasury Inflation-Protected Securities Index. Returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

In our view, the risks to long-term bonds are starting to outweigh the potential rewards. While we don’t look for a big move in yields in either direction near term, we see a greater likelihood of an increase over time than a decrease. The market is pricing in a gloomy outlook for the economy already. We believe there’s a good chance that the worst of the economic downturn is behind us and even a slow recovery could mean higher yields from here. On the positive side, the development of an effective vaccine for the coronavirus could lead to a rebound in economic activity that would lift real and nominal yields. In addition, the rising budget deficit is increasing the supply of long-term bonds that need to be financed in the market. With increased supply, higher yields may be needed to attract buyers.

We suggest investors keep the average duration in their fixed income portfolios below their target. That doesn’t mean abandoning long-term bonds—especially if those bonds are generating above-average income, or are providing diversification from stocks. It may mean increasing holdings in short-term bonds to balance out the duration risk.

For new investments, we favor focusing on bonds of short-to-intermediate-term duration that are high in credit quality, such as investment-grade municipal or corporate bonds. While yields are low in the entire fixed income market, the extra yield provided by taking some credit risk in the corporate bond market looks reasonable on a risk/reward basis. Similarly, the after-tax yields in the municipal bond market can make sense for investors in higher tax brackets. Finally, for investors with a higher tolerance for risk, an allocation to high yield or U.S. dollar-denominated emerging-market bonds, or preferred securities, could provide added income.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0820-00RV)

© Charles Schwab & Co.

© Charles Schwab

More Global Markets Topics >