Key Points

-

Confidence matters; faith in a brighter future drives risk taking, fueling growth through investment and consumption.

-

Real-time measures of confidence by consumers, analysts, and business leaders continues to improve.

-

Three potential developments over the rest of the year could shake confidence: the virus progression as schools and universities reopen, the ramifications of the U.S. election, and the outcome of post-Brexit trade talks.

The old adage “confidence is everything” applies to the economy as it does to how we approach our lives. While it’s true that too much confidence can be a vulnerability, too little can be worse by allowing negative feedback loops to deepen. Low interest rates simply can’t boost borrowing if confidence remains weak. Rising confidence is generally a positive; faith in a brighter future drives risk taking, fueling growth through investment and consumption. Keeping tabs on measures of confidence by consumers, business leaders, and analysts may tell us about what’s ahead for the economy, earnings, and the stock market. Confidence has been on the rise, but faces three big risks during the next three months.

Improving consumer confidence

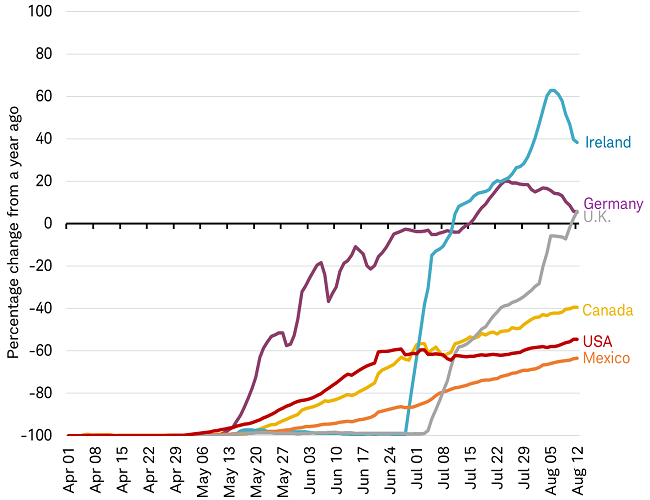

Official consumer confidence survey results are generally reported on a monthly basis. However, a lot can happen in a month, so we prefer indicators with more frequent updates on how consumers may be feeling. One real-time gauge of consumer confidence is restaurant reservations. Although the data is limited to a relatively small number of major countries, the trend in seated diners at restaurants on the OpenTable reservation network since re-openings began in May has been on the rise, as you can see in the chart below. Although there is some recent softening in Ireland and Germany, the trend still reflects growth from the same period a year ago. Improving real-time readings on consumer confidence can also be found in weekend cinema box office revenues and shopper traffic in retail stores.

Rising restaurant reservations on OpenTable network (7 day moving average)

Source: Charles Schwab, OpenTable.com data as of 8/13/2020.

Improving analyst confidence

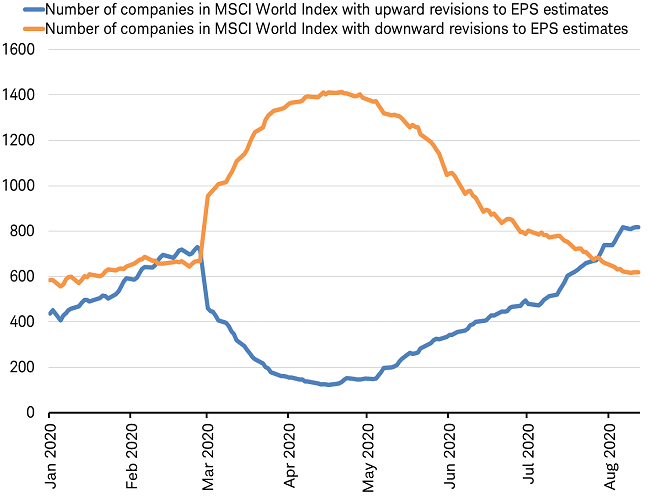

Earnings results for the second quarter and guidance for the rest of the year have been better than Wall Street analysts had been expecting, likely giving a boost to their confidence in an earnings recovery. In fact, upward revisions to analyst earnings per share (EPS) estimates in August are exceeding downward revisions for the first time since February.

Analyst upgrading their earnings outlook

Source: Charles Schwab, Factset data as of 8/13/2020. Past performance is no guarantee of future results.

Improving business confidence

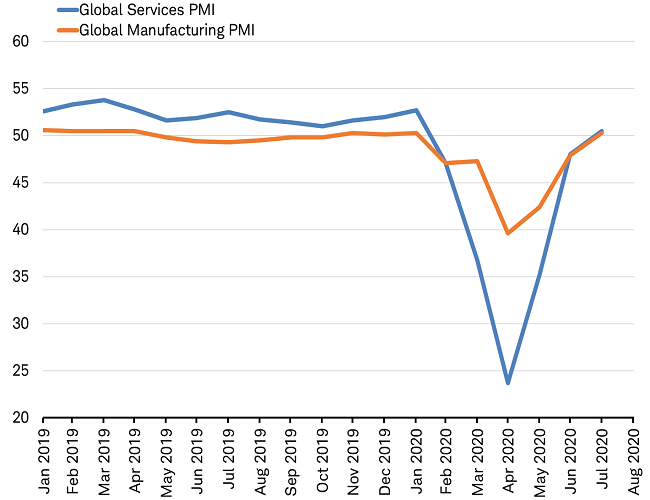

Timely surveys of business leaders also reflect a sharp rebound in confidence. The global purchasing managers index for both manufacturing and service sectors of the economy have fully rebounded above 50, the threshold between growth and recession. The rebound of confidence reflected in the latest survey, taken in late July and reported last week, suggests an improvement may be ahead in lagging economic indicators like business investment and employment.

Business leaders see improving growth

Source: Charles Schwab, Bloomberg data as of 8/13/2020.

What could shake confidence?

Rising confidence by consumers, analysts, and business leaders bodes well for near-term growth. However, during the remainder of the year, there are three major developments that could substantially alter the economic landscape and shake confidence in the recovery.

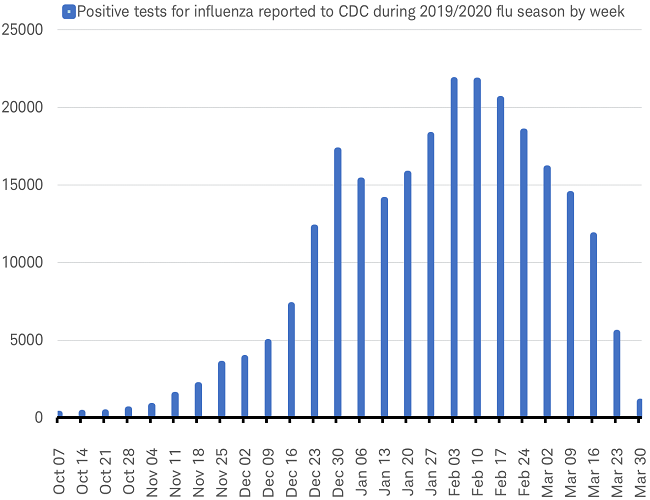

First, as students go back to school this fall we will know if it had an impact on the spread of COVID-19 and by early November we will be entering the early weeks of the flu season in the Northern Hemisphere when viruses tend to spread more readily. As a result, the biggest driver of changes in confidence this year will be going through its next stage for better or worse.

Three months from now: the flu season begins

Source: Charles Schwab, Center for Disease Control data as of 8/13/2020.

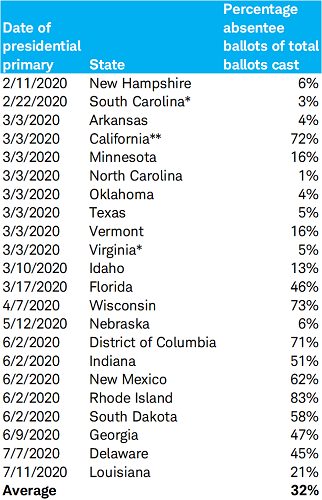

Secondly, the results of U.S. elections in early November could imply substantive changes in policy that may weaken analysts’ confidence in their earnings outlook. Also, confidence could be shaken if a close election doesn’t yield an immediate result, and the outcome isn’t known for days or weeks. Based on the average in the table below of primary voting this year, mail-in ballots constituted more than 30% of all ballots cast, with the trend increasing as the year progressed. It’s reasonable to consider that at least half of all ballots cast in November will be by mail, and those votes take more time to count. If election night turns into election month, it could undermine confidence (listen to Schwab’s political analyst Mike Townsend talk about this with Amy Walter, national editor of The Cook Political Report, in a recent podcast).

Potential for record absentee ballots

* Indicates a Democratic party primary only.

** California adopted universal vote-by-mail on a county-by-county basis for the 2020 primaries.

The table lists the states that have held presidential primaries this year and the percentage of ballots cast absentee. It includes absentee ballots as a percentage of overall ballots in the more than 20 states that have had primaries in 2020 and for which absentee ballot numbers are available. It excludes another eleven states that used what is called a universal mail ballot, where there are very few or no in-person polling places and ballots are sent to all registered voters and returned mostly by mail.

Source: Charles Schwab, Brookings Institution data as of 8/13/2020.

Thirdly, the outcome of the post-Brexit trade relationship with the European Union (EU) will be determined in the next few months. The United Kingdom left the EU on January 31, but no changes to the trade relationship have taken place during the transition period which expires at the end of this year. If a new trade deal is not at or near completion by early November it may be difficult to avoid a “hard” Brexit trade scenario. This could be a blow to confidence in U.K. policymakers and the U.K. economy (the world’s sixth largest), which is already suffering the worst COVID-19 recession among major economies.

These three issues—the viral progression as schools and universities reopen this fall, , the ramifications of the U.S. election, and the outcome of post-Brexit trade talks—are likely to be the key drivers of confidence and in turn, the economy, earnings and stock market.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular siNotuation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0820-0B7H)

© Charles Schwab

More Global Markets Topics >