Treasury bond yields have been drifting quietly lower since early June. But there is more going on beneath the surface than it might seem at first glance. Real yields—nominal yields less inflation—have declined steeply into negative territory. While nominal yields are near record-low levels from the deep economic decline, inflation expectations are picking up.

While nominal yields have been range-bound, real 10-year Treasury yields have been trending lower

Source: Bloomberg. 10-Year Treasury Inflation-Indexed Security, Constant Maturity, Percent, NSA (USGGT10YR Index) and 10-Year Treasury Constant Maturity Rate, NSA (USGG10YR Index). Daily data as of 8/18/2020. Past performance is no guarantee of future results.

If markets reflect the collective wisdom of investors, then the current message from the bond market seems muddled. Declining bond yields normally indicate that bond investors have a gloomy outlook on the economy. However, the message from the Treasury Inflation-Protected Securities (TIPS) market suggests that investors believe inflation risk is rising, a phenomenon usually associated with an overheating economy.

Despite the lack of evidence of inflation, expectations have been rising

Source: Bloomberg. U.S. Breakeven 10 Year (USGGBE10 Index) and U.S. Breakeven 5 Year (USGGBE05 Index). Daily data as of 8/18/2020. The breakeven rate is calculated as the difference between the yield of a nominal Treasury and the yield of a TIPS with a similar maturity. Past performance is no guarantee of future results.

The drop into negative real yields actually makes sense—at least in the near term. Nominal yields are being held down by the weakness in the economy and the Federal Reserve’s aggressive policy response. Due to the economic damage caused by the COVID-19 crisis, the Fed has lowered short-term interest rates to near zero and indicated it will keep rates low for at least a few more years. Fed Chair Jerome Powell also has stated that the Fed likely will keep its policy rate near zero until at least 2022, and that the members of the policy-setting committee aren’t “even thinking about thinking about raising interest rates.” In fact, the Fed is likely to adopt a policy in the next few months that explicitly indicates it will let inflation rise above its 2% target without pre-emptively raising interest rates. The market sees the Fed’s actions as sowing the seeds of inflation longer term.

Central banks see low nominal rates as a tool to stimulate the economy. By making the cost of borrowing so low, they encourage households to borrow and spend, and businesses to borrow for hiring and investment. When nominal yields are below the inflation rate, the returns to saving in risk-free investments are low relative to riskier investments. Given the depth of the economic downturn as a result of the coronavirus pandemic, it’s not surprising that real yields are negative. Investors are anticipating a very long, slow recovery that requires a lot of stimulus from the Fed to get the economy back on its feet.

However, at some point, nominal yields should respond to rising inflation risks. Why hasn’t that happened yet? It may be that investors expect any inflation to be short-lived. After all, the Fed has missed hitting its 2% target for inflation for several years. More likely, investors believe the Fed will adopt “yield-curve control” if long-term Treasury yields start to rise in response to inflation. Yield-curve control entails the Fed purchasing long-term bonds to hold down yields, in order to help stimulate economic growth and perhaps help finance the expanding federal debt. In either case, it means investing in long-term bonds requires a high tolerance for risk and a strong view of future inflation.

Consequences of negative real yields

Negative real bond yields also have implications for other assets. When Treasury yields are below the inflation rate, investors are inclined to look at other investments for better returns. The rally in the riskier segments of the bond market and alternative investments, like gold, can be seen as a potential consequence of negative real yields. When investors compare these assets to negative real yields, they tend to look more attractive, mitigating the perception of risk.

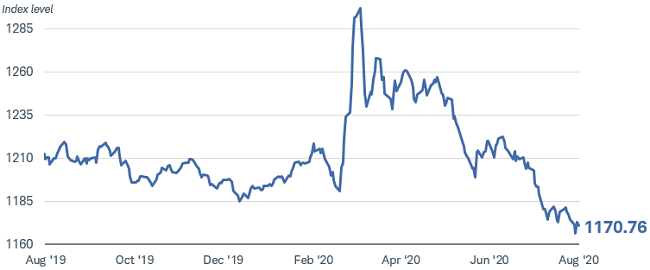

The drop in the U.S. dollar is also a consequence. The dollar has dropped by about 9% against a broad basket of currencies since the Fed pushed interest rates below the inflation rate. Holding dollars is less appealing when real interest rates are negative.

Negative real interest rates make holding dollars less appealing to investors

Source: Bloomberg. Bloomberg Dollar Spot Index (BBDXY Index). Daily data as of 8/18/2020. Past performance is no guarantee of future results.

What investors should consider

While it might be tempting to dive headlong into riskier assets on the prospect that real yields in the Treasury market will stay low for the long run, it could result in jumping from one risky situation to another. We have suggested lowering the average duration in portfolios due to the risk of rising rates longer term. Even a modest rise in yields could cause a sharp drop in long-term bond yields. However, Treasuries still provide ballast in a portfolio and valuable diversification from stocks. Moreover, there is no certainty that the Fed will succeed in pushing inflation higher. In an ongoing slow-growth environment, long-term yields could still move lower, as they have for nearly 40 years.

We would consider shifting some investments in nominal Treasuries to TIPS. TIPS are designed to keep pace with inflation. Selectively investing in more-aggressive income securities might be appropriate for those with the risk appetite. Abundant liquidity provided by central banks around the world and economic recovery should bode well for corporate and emerging-market bonds. However, we would focus on higher-rated bonds within those categories, as these are considered aggressive income investments.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Currencies are speculative, very volatile and are not suitable for all investors.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the U.S. government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the U.S. government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0820-0N0J)

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab