As expected, Federal Reserve Chair Jerome Powell announced a shift in policy that stems from a year-long review that the Fed has done. In a speech entitled “Navigating the Decade Ahead,” the key shift in policy is a move to an “average inflation” target instead of a precise 2% target. The change suggests that the Fed will likely maintain its zero-interest-rate policy for several more years until it sees inflation rise, rather than acting pre-emptively to address inflation expectations.

Bygones are no longer bygones

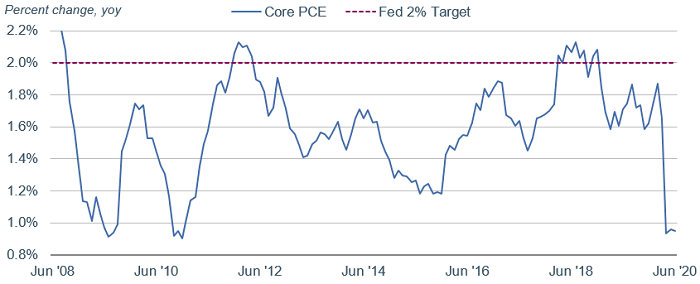

The Fed’s shift in policy implies that it will allow inflation to run at a pace above 2% for a period of time to offset the undershooting of inflation over the past decade. It is often referred to as letting inflation run “hot” for a while—although it’s hard to argue that 2.5% to 3.0% inflation is “hot.” In the past, the Fed viewed each inflation reading discretely. The past was gone, and all that mattered was the present and prospects for inflation based largely on the unemployment rate.

Inflation has fallen short of 2% for most of the past decade

Source: Bloomberg. Personal Consumption Expenditures: All Items Less Food & Energy (Core PCE) (PCE CYOY Index), percent change, year over year. Monthly data as of 6/30/2020.

The reasoning behind the Fed’s change in policy is the evidence that the relationship between the unemployment rate and inflation has changed. Lower levels of unemployment have not led to higher inflation during the past 10 to 15 years, as they had in previous years. In addition, the Fed has determined that demographic changes, such as the aging of the population along with slowing productivity growth, have led to a decline in the economy’s potential growth rate. The Fed’s estimate of potential gross domestic product growth has dropped to 1.8% from 2.5% in 2012. In turn, that suggests that the level of short-term interest rates associated with stable inflation is lower than in the past. The “neutral” federal funds rate is estimated at 2.5%, compared with 4.2% in 2012.

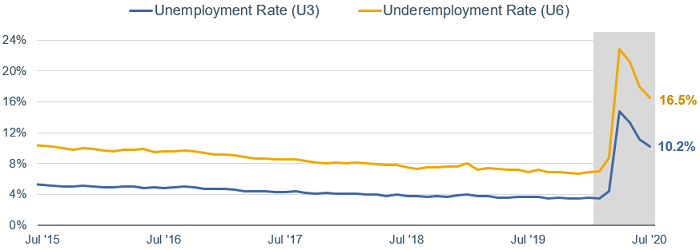

In announcing the Fed’s change in policy, Powell indicated that the fed funds rate would stay near zero until inflation rises above 2% “for some time.” The Fed has allowed itself a lot of flexibility, however. There is a heavy emphasis on achieving full employment, which now appears to be the Fed’s primary goal, considering that inflation remains quite low and unemployment very high.

High unemployment is one of the Fed’s biggest concerns

Source: Bureau of Labor Statistics. Civilian Unemployment Rate and Underemployment Rate, Total unemployed, plus all marginally attached workers plus total employed part time for economic reasons (U6 Rate), Percent, Monthly, Seasonally Adjusted. Shaded area indicates recession. Monthly data as of July 2020.

What’s missing

Powell provided no indication of how the Fed hopes to achieve higher inflation. That’s probably because the Fed has already expanded monetary policy dramatically, without lifting inflation. It can continue to keep short-term interest rates near zero, expand its balance sheet by buying more bonds to hold down long-term interest rates, and use its special facilities to lend. However, these tools are stretched already. Many Fed officials have been urging Congress to pass more fiscal relief, as that would likely have a more immediate effect in boosting growth, employment, and inflation.

Evolution, not revolution

Powell’s speech is important in that it codifies the Fed’s approach to policy. However, it isn’t a big change from the way the Fed has been operating for a while now. It will help set expectations about policy by identifying the key factors that are important to the Fed. However, monetary policy can only do so much. The biggest risk to the policy shift is that long-term rates could rise on the assumption that the Fed would not respond to inflation fast enough to contain it.

Inflation expectations have already been rising, but remain below 2%. The Fed could find itself needing to react more quickly than it would like to quell those expectations. Yield curve control could be employed at that stage—with the Fed buying longer-term bonds to hold down yields. That doesn’t appear to be a near-term issue, but it could be a longer-term issue.

Market expectations for inflation have been rising but remain below 2%

Source: Bloomberg. U.S. Breakeven 10 Year (USGGBE10 Index) and U.S. Breakeven 5 Year (USGGBE05 Index). Daily data as of 8/27/2020.

Bottom line: The Fed’s policy announcement has reinforced our view. We look for the Fed to keep short-term interest rates low for several more years, and the U.S. dollar to weaken further over time.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Currencies are speculative, very volatile and are not suitable for all investors.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0820-0KAB)

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab