Key Points

-

The biggest political risk facing investors may be the potential for politicians to implement national lockdowns in response to a rise in new COVID-19 cases that could lead to renewed recession and a new bear market for stocks.

-

The prospects for a return to lockdowns appear to be on the rise, pressuring stock prices in September.

-

However, we believe a return to widespread national lockdowns is highly unlikely for three reasons: healthcare systems are not overwhelmed, precision pays off when it comes to the effectiveness of restrictions, and national lockdowns are known to have a huge cost.

Many investors are eyeing the politics surrounding the U.S. elections as a major factor for the market in the coming months. But, the politics of a potential return to national lockdowns in response to the resurgence of COVID-19 cases may be a bigger potential market mover for investors to consider. A widespread return to national lockdowns would likely mean a return to recession for the global economy and a bear market for stocks.

The potential for a return to lockdowns appears to be on the rise, pressuring stock prices in September. U.S. virus cases have started to tick back up again, while parts of Europe are experiencing a steady resurgence. Israel has instituted a second national lockdown. The United Kingdom has rolled out new restrictions. Soaring new cases in France and Spain are prompting politicians to consider similar measures. However, we believe a return to widespread national lockdowns is highly unlikely for three reasons:

-

Healthcare systems not overwhelmed: Positive cases are rising in many countries, but the percentage of those tested that are positive, along with hospitalizations and deaths from COVID-19, remain relatively low.

-

Precision pays off: Mid-summer second waves of virus cases in the U.S. and China faded when narrow, localized restrictions were put in place, achieving success while limiting overall economic impact.

-

Huge cost: The economic and human toll of national lockdowns is now known to be severe; the first half of 2020 experienced the worst global recession since the Great Depression.

Examining each of these leads us to believe a return to widespread national lockdowns and a related return to global recession and bear market is highly unlikely.

Healthcare systems not overwhelmed

The outbreaks in Europe differ from earlier this year in that they have not been accompanied by a similar spike in hospital admissions, according to the European Centre for Disease Prevention and Control. Additionally, the hospitalization rate of those with COVID-19 has fallen sharply in the U.S., according to the U.S. Center for Disease Control. These examples provide some reassurance that healthcare systems may not become as overwhelmed as they were earlier this year.

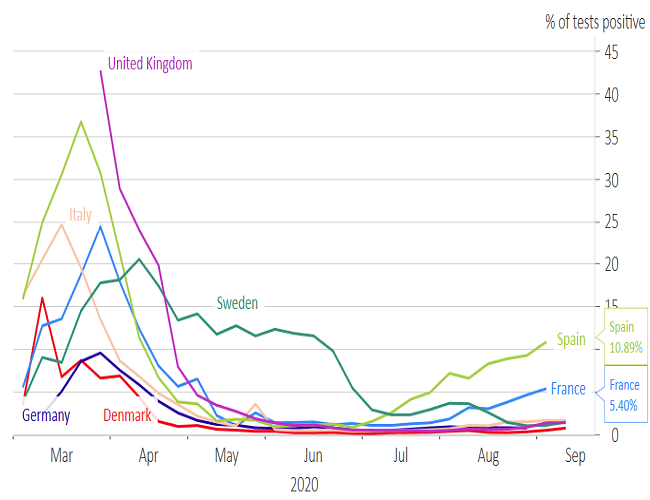

While there has been a rise in the number of new cases of COVID-19, it is the result of the large number of those being tested. The rise in new positive cases isn’t alarming when viewed as a percentage of those being tested, as you can see in the chart below. The percentage of positive tests are really only ticking up in France and Spain.

Positive percentage of COVID-19 tests remains low outside of France and Spain

Source: Macrobond, European Centre for Disease Prevention & Control data as of 9/24/2020.

The global number of deaths each day tied to COVID-19 remains stable, steadily averaging around 6,000 per day since March, even though the number of daily new confirmed cases has more than tripled. It is our opinion that hospitalization and deaths are more important factors (rather than new cases) when it comes to the likelihood of lockdowns.

Precision pays off

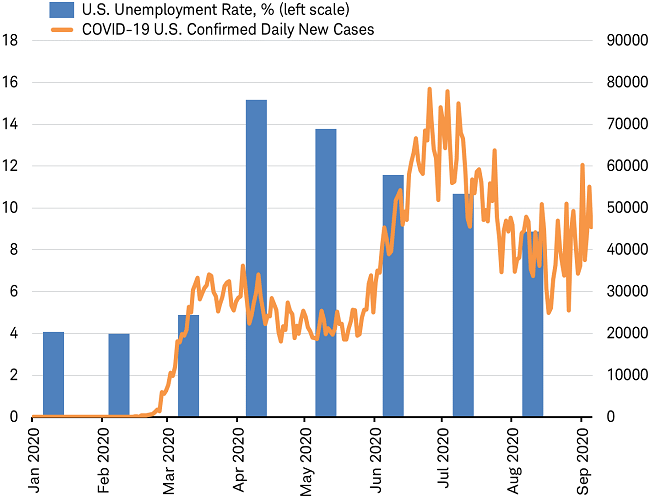

The U.S. experienced a spike in new daily COVID-19 cases this summer, as you can see in the chart below. Although the Fed warned about the danger posed to the economy by the second wave accompanied with expiring fiscal stimulus programs, the return of targeted restrictions in some states did not lead the economy back into recession. In fact, the labor market continued to improve over the summer months, recovering half of the jobs lost earlier in the year.

U.S. daily new cases and unemployment rate

Source: Charles Schwab, Bloomberg data as of 9/27/2020.

China also saw surges in cases in parts of the country this summer and responded with localized and targeted restrictions that were effective, but didn’t reverse the strong economic rebound. The International Monetary Fund forecasts that China will be the only country in the world to grow its economy in 2020, despite experiencing the first wave of COVID-19 at the beginning of the year and a second wave this summer.

France and Spain are seeing a second surge in infections after loosening lockdown restrictions, while Italy has kept the disease under control with local and targeted restrictions. For example, in August, Rome ordered a closure of nightclubs and introduced a rule that face masks must be worn in all crowded places between 6pm and 6am. Visitors to bars and restaurants must record their names and numbers to aid in tracking contact with any infected person. Companies have been encouraged to extend work from home arrangements into the fall and those that have reopened must comply with wearing face masks, body temperature scans, physical distancing and COVID-19 testing.

The economic consequences of these effective measures have so far been modest, but three factors may influence the economic impact of future restrictions, represented by measures taken in the U.K.:

- How widespread they are. If they extend only to travel and entertainment, which make up less than 10% of GDP in most economies, the drag may be minor, especially considering those industries have yet to really recover anyway. But if business closures spread to construction and manufacturing, where working from home isn’t an option, the impact could be far greater. U.K. leaders introduced new restrictions last week, but nowhere near as onerous as a national lockdown with an earlier close for restaurants and bars, reversal of plans to allow live audiences at sporting events next month, a request to work from home when possible, and to wear masks in public places.

- How long they last. So far, many measures introduced to combat the second wave have been announced in advance of being implemented and with limited time frames—often a few weeks—allowing businesses to respond and plan appropriately. The more abrupt and open-ended the measures, the more negative their likely economic impact. The restrictions announced for the UK were timed longer than most, at up to six months.

- If accompanied by new stimulus. Additional fiscal stimulus can help mitigate the impact of restrictions, if targeted appropriately. The U.K. recently coupled new restrictions with new aid in the form of 10 years of guaranteed loans for businesses, pay-as-you-go rates on loans, extend Value-Added Tax cuts, and an extension of benefits for the unemployed.

Huge cost

Politicians now have a much better idea of the economic costs of using widespread lockdowns to bring the virus under control.

- Countries that deployed lockdowns earlier this year experienced an average peak-to-trough fall in GDP of 13.5%, as calculated by Capital Economics.

- The cost of fiscal stimulus pushed up public debt ratios by an average of 35% of GDP, according to research by Capital Economics.

The full impact on the labor market has been obscured by worker furlough programs, but tens of millions of workers have lost their jobs.

- The high economic and social costs make it more likely governments will respond to new outbreaks with equally-effective targeted restrictions rather than new national lockdowns.

Market reaction

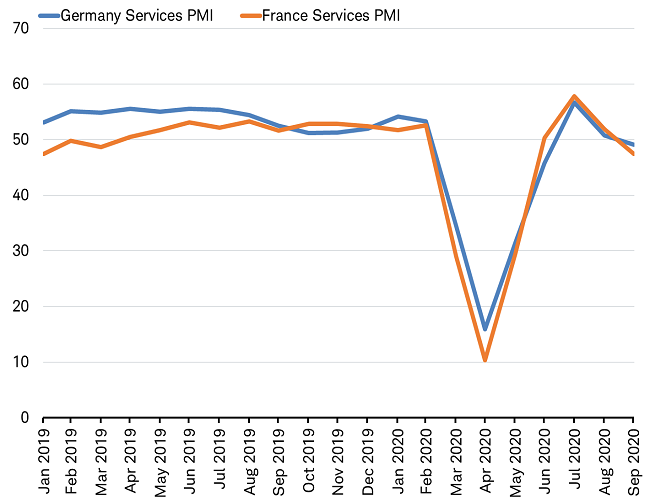

The recent weakness in the purchasing manager indexes for services suggests that the momentum of the rebound in economic activity seen over the past few months is fading, even in countries where new virus cases are falling. Now the risk is will renewed restrictions to contain the outbreaks send the global economic recovery into reverse?

V-shaped recovery losing momentum?

Source: Charles Schwab, Bloomberg data as of 9/25/2020.

Avoiding a boom and bust economic environment generated from the rapid removal of economic restrictions followed by a renewed national lockdown should be a priority for politicians. With broad-based vaccinations unlikely this year, measured restrictions may be needed to effectively contain the virus while being efficient in their economic cost. While stocks have been wary of measures taken in September to contain the outbreaks, investors may soon get comfortable with these effective alternatives to widespread shutdowns.

But the biggest political risk facing investors is the potential for a more dramatic reaction to COVID outbreaks by politicians in the form of national lockdowns that could lead to a new bear market for stocks. In addition, such severe measures could prompt a rotation back into the COVID-winner U.S. tech stocks and away from cyclically-oriented international stocks that have outperformed recently.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request. The policy analysis does not constitute and should not be interpreted as an endorsement of any political party.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(0920-0N1S)

© Charles Schwab

Read more commentaries by Charles Schwab