As China begins the year of the Ox, many investors are wondering whether another bull run is possible in 2021. Given that last year’s rally was extremely narrow, we believe many parts of the market still offer pent-up recovery potential.

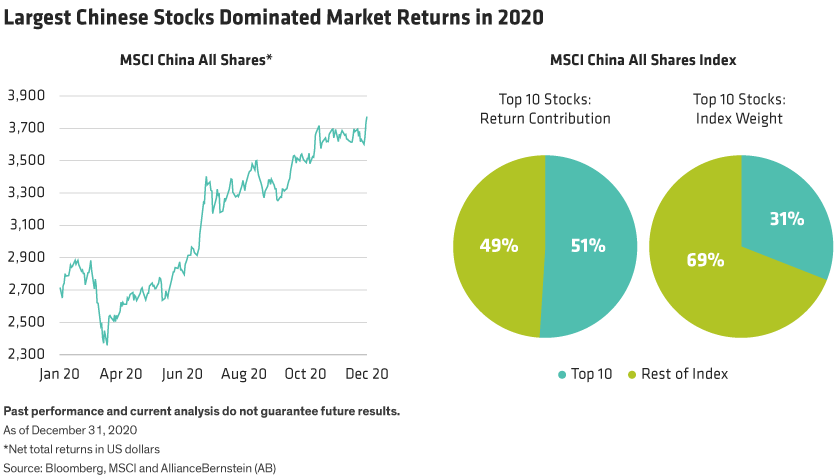

Chinese stocks ranked among the world’s top performers last year. The MSCI China All Shares Index rose 33.4% in US-dollar terms, well ahead of the S&P 500’s 18.4% returns as China’s more aggressive response to COVID-19 aided the market. Better management of the pandemic, along with targeted policy measures, produced fewer sporadic lockdowns, while exports remained resilient. As a result, economic activity bounced back sharply from the first-quarter contraction, and Chinese companies enjoyed a faster earnings recovery than developed market peers.

Growth Giants Dominated the Market

Despite headline returns, however, the market’s performance was heavily concentrated within a few names. Out of more than 800 constituents in the MSCI China All Shares index, the hypergrowth stocks of Alibaba, Tencent, Meituan, Nio and JD.com accounted for more than a third of total performance in the MSCI China All Shares last year. The top 10 stocks accounted for more than half of the index’s returns (Display, below).

The trends echoed similar sector returns in the US. Internet and consumer-growth stocks adapted quickly to an evolving business environment, supporting earnings visibility that bolstered investor confidence. Increasing digitalization of work, shopping and leisure activities during the pandemic fueled returns for new economy stocks, much like in the US.

Economic Recovery Is Accelerating

However, the concentrated performance appears to conflict with the broader recovery. The pickup in infrastructure activity is feeding industrial production activity, while a recovery in overseas demand is lifting Chinese exporters. Share prices of Chinese companies that are sensitive to economic growth, from machinery-makers to commodity producers to life insurers, have trailed far behind more expensive growth stocks, despite the improving macroeconomic backdrop.

We believe that the economic momentum should continue. China’s fourth-quarter GDP growth reached 6.5%, making the outlook for 2021 even more encouraging as consumer spending rebounds after initially lagging the manufacturing recovery. And if momentum is sustained, the pace of China’s GDP expansion in the first half of this year could significantly exceed growth rates of the last five years.

However, the accelerating economy has prompted the People’s Bank of China to begin adopting a moderate tightening bias. Chinese 10-year government bond yields have risen nearly 100 basis points since April lows, while monetary stimulus from the first three quarters of 2020 is now being reversed. Inflation signs are beginning to appear in commodities and select manufacturing segments, which we believe augurs well for Chinese stocks that have not yet participated in the market recovery.

Positioning for a Broader Rebound

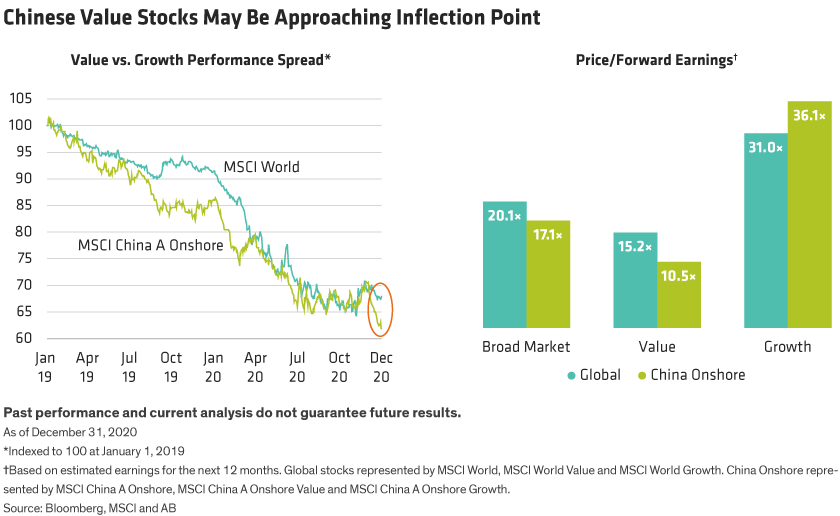

Return patterns for 2020 have left huge disparities: MSCI China A Onshore growth stocks outperformed value stocks by 46%, closing the year at a price/forward earnings (P/FE) multiple of 36.1×, compared to 10.5× in value names (Display, below).

With the P/FE multiples of expensive stocks expanding aggressively, the valuation gap between spread growth and value stocks appears stretched, in our view. However, we believe this creates an attractive risk-reward opportunity mirroring the broader economic recovery unfolding.

Some companies that outperformed in 2020 may struggle to repeat the feat this year. Internet companies may face increasing antitrust regulation that may challenge companies with high valuations. Similar regulatory concerns echo in the pricey healthcare sector, where policy initiatives aimed at lowering drug prices adds uncertainty for investors.

Efforts on regulatory oversight and social welfare should dominate the policy agenda in 2021, in our view. With the Chinese Communist Party celebrating its centennial anniversary, policies will likely prioritize upholding social stability while managing systemic risks. Measures to improve China’s investment landscape are already evident. A string of recent bond defaults at state-owned enterprises reflects Beijing’s efforts to remove an implicit moral hazard by enabling better capital market dynamics.

These actions should help offset other concerns about investing in China. It’s still hard to predict how US-China trade tensions will change under President Joe Biden’s administration. While US-listed Chinese companies still face the risk of delisting from New York, Beijing has simultaneously expanded domestic market access to foreign investors. Secondary listings in Hong Kong and the expansion of the Shanghai-Hong Kong Stock Connect should also support liquidity for Chinese stocks.

Left-Behind Stocks Poised to Deliver

Relatively low valuations and robust earnings fundamentals for select companies that did not participate in last year’s rally deserve attention. As signs of a cyclical recovery in China remain intact, we see opportunities for market leaders in materials, machinery and mining. Beijing’s push to become technologically self-reliant also creates opportunities for advanced semiconductor manufacturers.

While tighter labor market conditions and a recovery in household disposable income support the long-term outlook in the consumer and healthcare sectors, investors must be highly selective, in our view. New stimulus measures for trucks and electric vehicles should serve as a tailwind for automobile manufacturers, where we believe investors have not yet recognized the imminent turning point in sales.

Chinese stocks have much to offer in 2021. With a worldwide vaccination initiative taking place, we believe value stocks could begin to catch up as developed economies begin to reopen. Indeed, global value stocks have bounced back since November, while China value was still underperforming growth (Display, left). What’s more, by year end, Chinese value stocks were much cheaper than global value stocks, while Chinese growth stocks were more expensive than global peers (Display, right).

Last year’s outstanding market returns masked a deep divergence. As China continues to demonstrate its solid management of the COVID-19 crisis, we think steady economic growth will underpin corporate earnings for many overlooked companies, mitigating any potential market volatility. Targeting stocks that were left behind in 2020 is a great way for investors to initiate or expand allocations to Chinese equities ahead of the next stage of the recovery.

John Lin is Portfolio Manager of China Equities at AllianceBernstein (AB).

Stuart Rae is Chief Investment Officer of Asia-Pacific Value Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© AllianceBernstein

Read more commentaries by AllianceBernstein