Despite questions over financing the European Union’s (EU’s) new Green Deal, the green transition is now under way. The implications for bond investors are clear and urgent.

Global efforts to combat climate change are about to get a welcome boost from US reengagement. One of President Biden’s first acts was taking the US back into the Paris climate accord. But while the US was shunning the climate agreement, the EU was taking the lead.

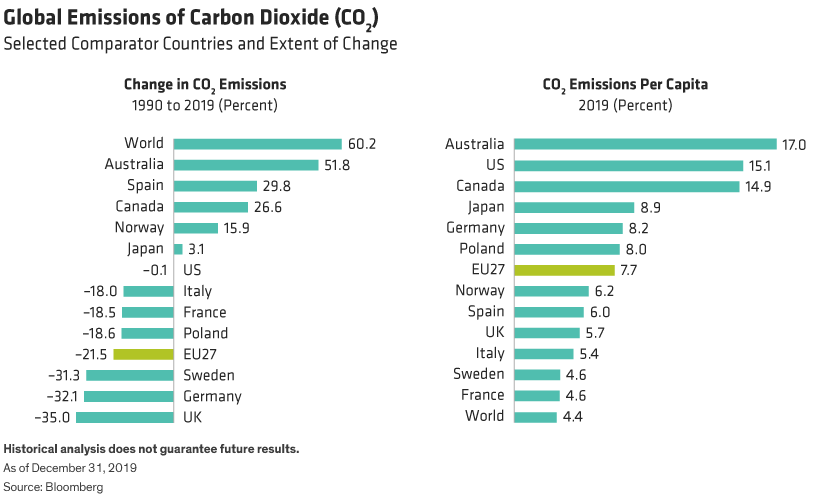

Understanding the Green Picture

The European Green Deal is the centrepiece of the EU’s climate strategy. Launched in December 2019, it is a comprehensive plan to cut greenhouse gas emissions, invest in new technologies and protect the natural environment. It aims to make Europe the world’s first climate-neutral continent by 2050.

Europe can justifiably claim to be leading the world in reducing emissions. Since 1990, the EU’s net CO2 emissions have fallen by over 20% while globally net emissions increased by over 60%. Of course, the EU has advantages. Most of its economies passed peak industrialisation many years ago and have relatively high carbon starting points. That’s why euro-area net CO2 emissions per capita are still well above the global average―7.7 tonnes per person per annum against 4.4 globally (Display, above).

Although the EU compares favorably with other developed economies―including the US and Japan―in curbing emissions, the Green Deal recognizes that this is still not good enough. So, to achieve climate neutrality by 2050, EU leaders have pledged to reduce net greenhouse gas emissions by at least 55% of 1990 levels by 2030.

Such a big step up from the old target of 40% will require a huge effort in new legislation, oversight mechanisms and increased public and private sector investment. The transition will be tricky, as many measures will disproportionately hit poorer countries and social groups.

High Commitment to Success

Critics of the Green Deal have focused on the financing. The European Commission initially proposed €1 trillion of additional investment spending. But roughly half of this “new” money represents rebranded spending from the existing EU budget. And much of the remainder relies on private sector contributions―which may or may not be forthcoming. Tellingly, €1 trillion falls well short of what the EU itself thinks is necessary to reach its new 2030 target.

But focusing on the Green Deal’s shortcomings misses the bigger picture. While COVID-19 is currently the number one priority for Europe’s governments, climate change is now clearly at the top of the short-, medium- and long-term policy agendas. For example the new €750 billion recovery fund, branded Next-Generation EU (NGEU), is mandated to spend 37% of its budget on green projects. Even if all of the spending isn’t quite as “new” and “green” as advertised, the impetus for change is clear.

Finally, all key players are now pushing in the same direction on climate change, notably the European Commission, national governments, the European Parliament, the corporate sector and the European Central Bank (ECB). The ECB has put climate change at the heart of its latest strategy review. It’s hard to predict how this new initiative will develop. But over the last year, monetary and fiscal policy in the euro area have become “joined at the hip” to fight a global pandemic. And it isn’t a big step from fighting the virus to using the central bank balance sheet to counter an even more important threat.

Investment Risks and Opportunities

The EU is also harnessing its legislative powers to shape the green agenda, as with recent regulatory changes to align investment flows with a more sustainable economy. The Sustainable Finance Directive Regulation (SFDR) and the EU taxonomy establish standardized disclosure rules for investment activities defined as sustainable and that are aligned with climate change mitigation.

For corporate bond issuers, these developments represent both opportunity and threat. Companies that are naturally aligned with climate mitigation or are in the process of addressing their climate risks stand to benefit. But issuers in unaligned industries (e.g., energy and mining), and with no transition plan, risk being shunned by investors, resulting in a higher cost of capital.

For example, power utilities use multiple fuels to generate electricity. While some rely solely on coal and have no comprehensive plans to transition to the low-carbon economy, others have invested heavily in renewables. Credit spreads don’t always reflect sustainability levels of competing businesses, and we believe the EU’s mandatory disclosures will lead to greater differentiation between their bond prices. When the market adjusts, the cost of capital will start rising quickly for climate laggards.

Other industries―such as automotives or chemicals―are even further behind. In their current form, many may struggle to align their activities with the EU taxonomy. But looking ahead, we see large divergences in their plans to address climate change. Investor engagement with company management will be key to understanding their decarbonization strategies and to unlocking value in dirtier companies.

Green Deal Needs Green Bonds

Green bonds represent a further major opportunity. More investors are seeking to address climate change within their fixed-income portfolios, and the green bond market has seen rapid growth of both outstanding volume and issuer variety. The EU Green Bond Standard is coming of age. This sets guidelines for acceptable use of proceeds (UoP) for green bonds in alignment with the EU taxonomy standards, and we believe it will promote more issuance and sector diversification.

Corporate green bonds can help increase the speed of transition for “brown” industries, and the much-touted NGEU recovery plan and related sovereign issuance will also help direct capital towards the green transition. Alongside green bonds, some bond issues now feature key performance indicators (KPIs). These bonds link their coupons to firm-wide improvement in specific sustainability metrics, creating another powerful tool to advance sustainability.

Despite question marks over the amount of new investment that will be unlocked by the Green Deal, Europe’s green transition is now under way. Investors need a process for green evaluation and engagement to detect greenwashing. It will be extremely important to track and engage with both corporates and governments on their alignment of proceeds with the EU taxonomy and the green recovery. And both should be held equally accountable when scrutinizing their UoP and material impacts on climate change.

Darren Williams is Director–Global Economic Research at AllianceBernstein (AB).

Shawn Keegan is Portfolio Manager–Credit at AB.

Salima Lamdouar is Associate Portfolio Manager–Credit at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorized and regulated by the Financial Conduct Authority in the United Kingdom.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein.

© AllianceBernstein

Read more commentaries by AllianceBernstein