Italy’s new prime minister, Mario Draghi, has a well-earned reputation for turning around difficult situations. But can he reverse Italy’s relative economic decline? And what does his program mean for Italian bond yields?

As president of the European Central Bank (ECB) Mario Draghi made his name for doing “whatever it takes” to save the euro. Now, as Italy’s prime minister, he faces another daunting challenge.

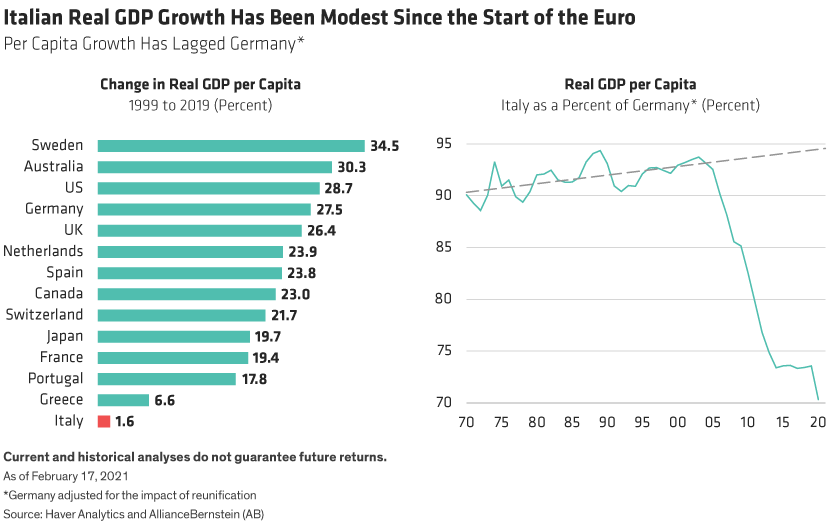

Italy’s Growth Has Lagged Peers

It will be a tough task to transform Italy’s longer-term outlook. The Italian economy has performed poorly in recent years. Real per capita GDP has lagged developed-world peers (Display below, left), and the relative decline has been stark against euro-area comparators such as Germany (Display, right).

Governance Is Key

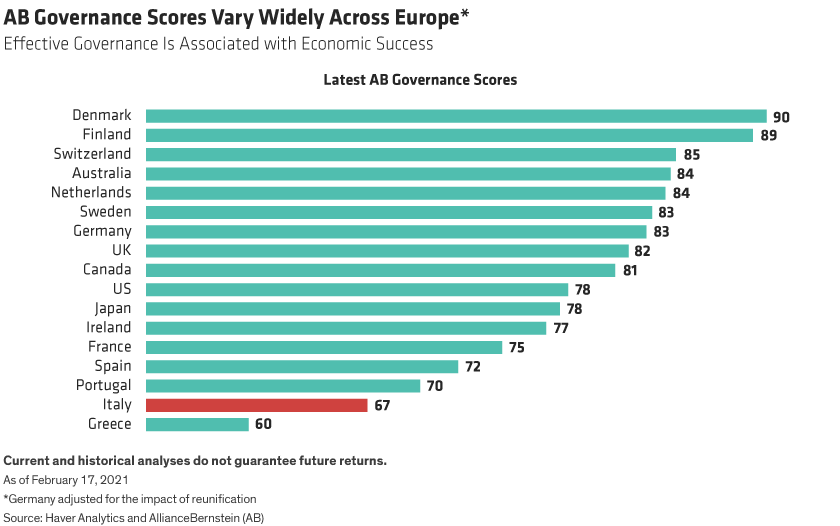

Our research indicates that effective sovereign governance has a direct link to positive economic outcomes. As part of our ESG scoring framework, we regularly calculate sovereign governance ratings including the principal euro-area nations (Display, below). Our results suggest that Italy’s relative decline is rooted in deep-seated structural weaknesses. These have weighed more heavily on growth since Italy joined the euro in 1999, losing the safety valve of periodic currency realignment.

Reform Will Be Challenging—But Draghi Can Make a Strong Start

Now, with devaluation ruled out, it’s going to take a gargantuan reform effort to turn the Italian ship around. Still, early signs are encouraging. The new prime minister’s immediate focus is, rightly, on steering the economy out of the pandemic and drafting a recovery and resilience plan to unlock NextGenEU funding from the EU. (This new money will be focused on digitization and speeding up the green transition.) After that, Draghi will turn his attention to long-overdue reforms of the judicial, public administration and taxation systems, areas in which there’s ample scope to improve Italy’s governance score and longer-term economic outcomes.

Of course, the further Draghi stretches, the more difficult it will be to sustain the political consensus needed for deep-rooted change. Even so, with most of Italy’s main political parties supporting him (and representing roughly 80% of parliamentary votes), the new prime minister has room to maneuver.

But focusing too heavily on the longer-term outlook risks ignoring some very important near-term positives. First, while Italy’s political parties will start jostling for position ahead of the next general election (due by June 2023), a period of political stability lasting a year or more now looks almost guaranteed. And in a strong show of unity even the right-wing populist League has joined the government and adopted a more constructive stance towards the EU. Finally, with Draghi at the helm, there’s now a much lower risk that Italy will squander the opportunity presented by NextGenEU funding. Assuming grants worth roughly 4.5% of GDP over the next three to five years, this new money won’t be enough to solve all of Italy’s problems. But it would provide a welcome start and might even act as a catalyst for further reform.

Financial Markets See Positive Change

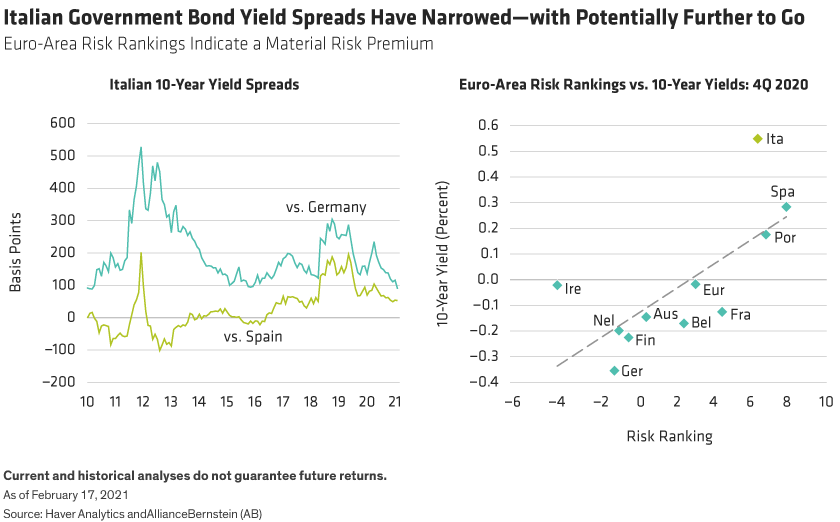

These developments represent positive surprises for financial markets, and it’s quite possible that the Italian treasury bond (BTP) spread versus Germany will narrow even further from recent lows (Display below, left). Indeed, our risk rankings (Display, right) suggest that there’s still a material premium embedded in Italian sovereign bond yields.

Although BTPs have already rallied, several factors may drive spreads even tighter. As noted above, the near-term political outlook has improved. And in terms of sentiment, the market will be optimistic that Draghi will deliver structural reforms and make efficient, effective use of EU funds.

The technical backdrop for BTPs is also set to stay strong. ECB quantitative easing (QE) bond purchases will continue to support spreads, and, while foreign buyer demand will likely be high, net issuance is expected to turn negative (and supportive of lower yields) going into the second quarter. With global sovereign bond yields still ultra-low, BTPs appear to offer attractive value and should remain supported in global bond markets that have ample excess liquidity.

While the short-term outlook is constructive, longer-term uncertainties remain. Beyond the next six to nine months, political risks could resurface, fears of ECB tapering may revive, and optimism could start to fade in 2022. So, while Italy has the potential to outperform many other sovereign markets, investors need to be aware of the timeframes involved.

Darren Williams is Director—Global Economic Research at AllianceBernstein (AB).

Nicholas Sanders is Portfolio Manager—Global Multi-Sector at AllianceBernstein (AB).

The value of an investment can go down as well as up and investors may not get back the full amount they invested.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein