A boom in spending has stirred fears of economic overheating, which has coincided with a surge in commodity prices and a lift in traditional inflation metrics. Europe’s economy is finally turning the corner, leaving its double-dip recession behind. Meanwhile, interest rates have been in a holding pattern over the past month despite inflation fears, suggesting the bond market has already discounted much of the rebound in the economy since last year.

U.S. stocks and economy: Overheating chatter

As we move into the summer, the pace of economic growth remains robust, notwithstanding a weak April jobs report. Gross domestic product (GDP), although a lagging indicator, grew at an annualized quarter over quarter rate of 6.4% in the first quarter. That undercut economists’ consensus estimates slightly, but much of the drag was due to inventories—consumption was quite strong, growing at a 10.7% rate.

Much of the strength is rightly attributed to the fiscal aid that has been injected into the economy. The concurrent boom in spending has stirred fears of economic overheating, which has coincided with a surge in commodity prices and a lift in traditional inflation metrics.

While prices have generally increased, much of the rise has been due to base effects, given that metrics like the consumer price index (CPI) are measured relative to the prior year—which, at this point, was when the economy was broadly shut down. Sustained inflationary pressures have historically come from a severe tightening in the labor market, which pushes up wages to a significant degree—generating the type of “wage-price spiral” inflation that became systemic in the 1970s.

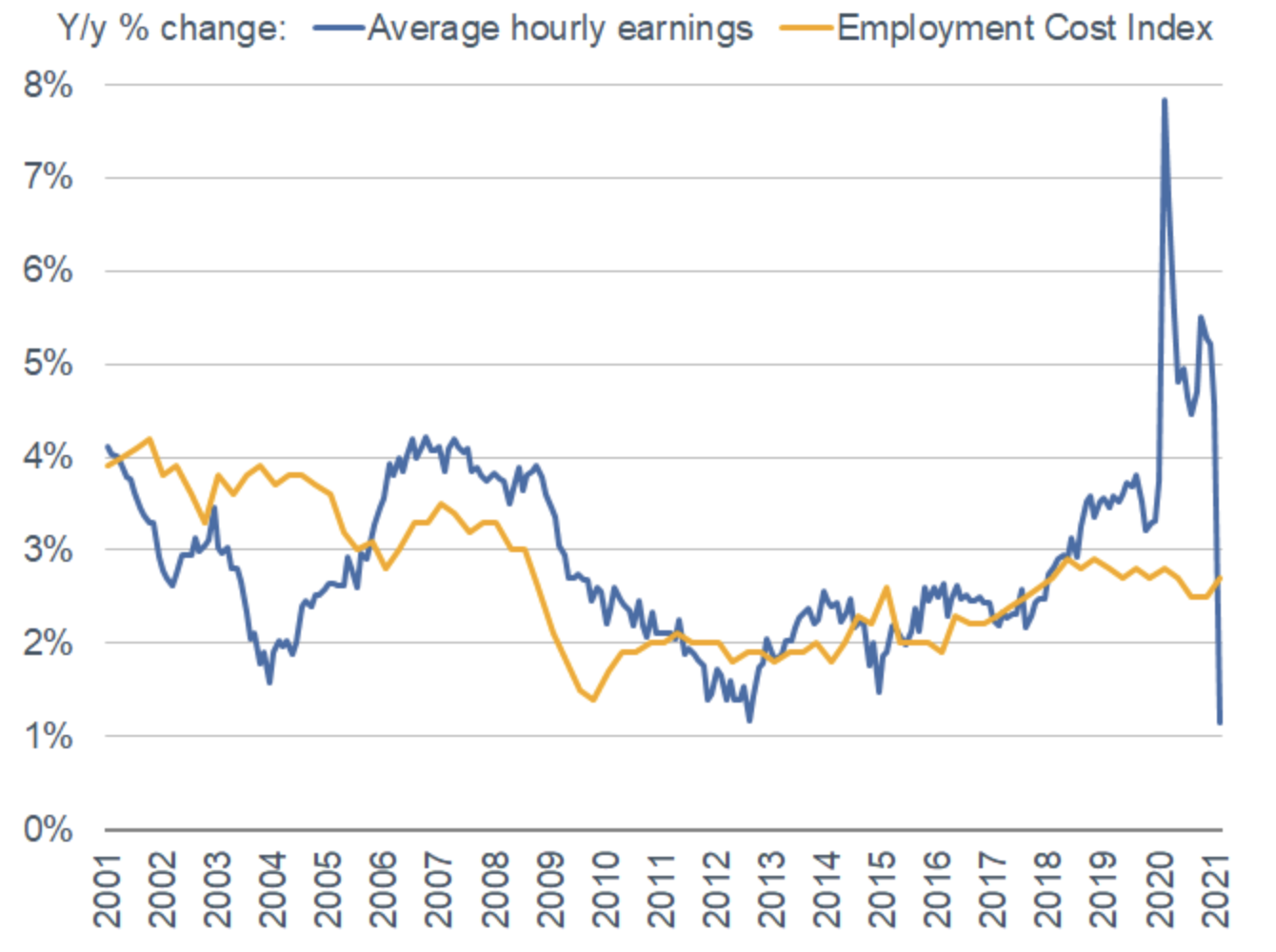

There was a spike last year in average hourly earnings, but that was due to the drastic loss of lower-paying jobs, which kept a large number of high earners in the equation (which is a simple average) and artificially boosted the index. With lower-paying jobs now coming back, the gauge has reversed markedly, as you can see in the chart below.

Average hourly earnings spiked last year as lower-wage jobs were lost

Source: Charles Schwab, Bloomberg, Bureau of Labor Statistics (BLS), as of 4/30/2021. The Employment Cost Index (ECI) is a quarterly economic series published by the Bureau of Labor Statistics that details the growth of total employee compensation. The index is prepared and published by the Bureau of Labor Statistics (BLS), a unit of the United States Department of Labor.

Given those distortions, we prefer to focus on the Employment Cost Index, which accounts for the wage level mix shifts and had a more modest uptick. We may see an upward trend take hold as the economy continues to recover, but inflation would likely become a larger issue only if the increase in the index were unaccompanied by a rise in productivity.

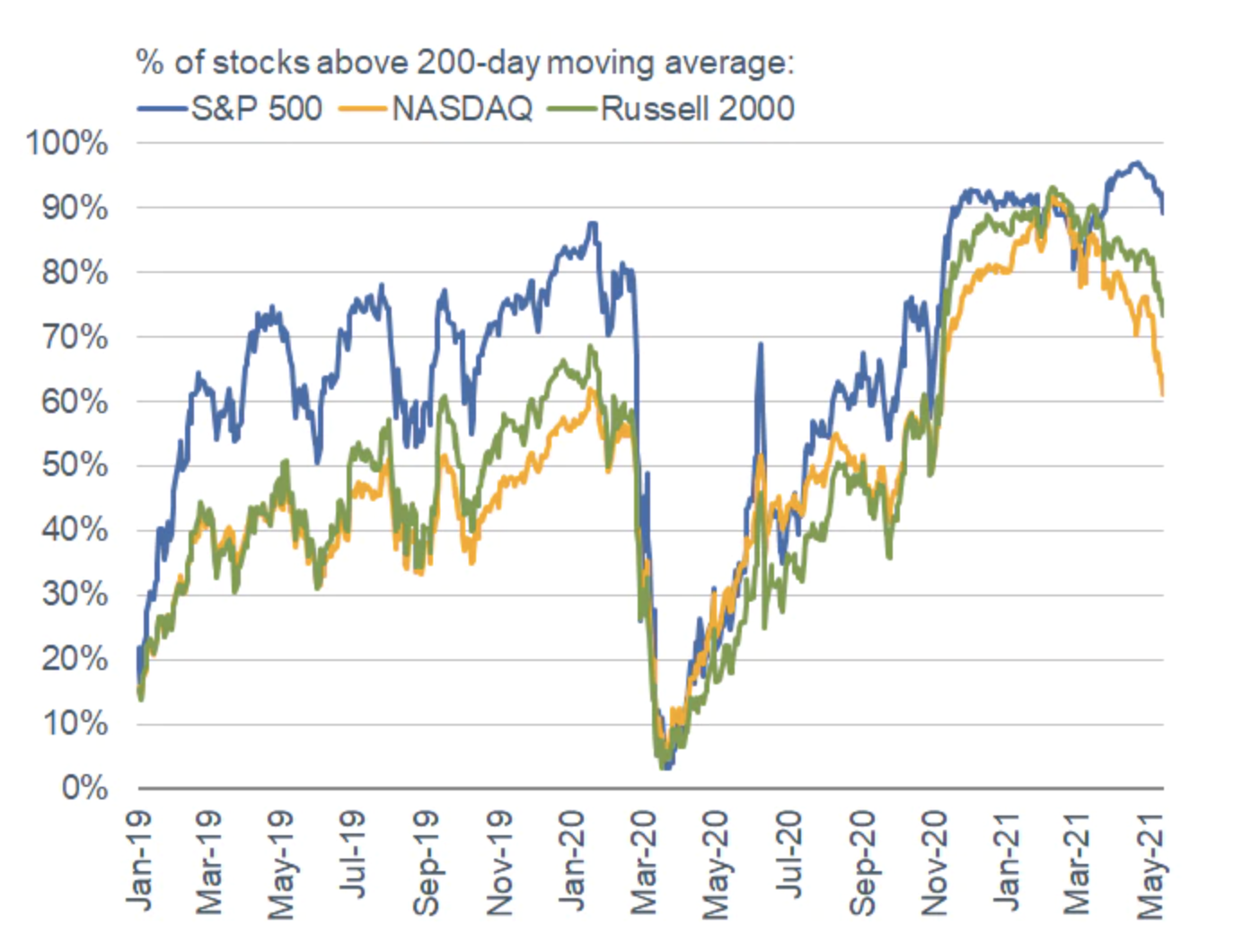

Stronger economic and corporate earnings growth has been priced in by the stock market for a good portion of the rally since the March 2020 lows, as breadth among the major averages was healthy for much of that period. You can see in the chart below that more than 90% of S&P 500® index members are still trading above their 200-day moving averages. But there has been breadth deterioration in both the NASDAQ and Russell 2000 over the past couple of months as inflation concerns have put downward pressure on higher-valuation segments of the market.

Breadth strong for the S&P 500, but has deteriorated for the NASDAQ

Source: Charles Schwab, Bloomberg, as of 5/12/2021. Past performance is no guarantee of future results.

Some of the deterioration is natural, as stocks’ rapid climb and lofty breadth statistics bring on overbought technical conditions. The stark contrast between the S&P 500 and NASDAQ underscores the broader shift away from the Information Technology sector—which outperformed its peers decisively last year—and toward cyclical areas associated with accelerating economic growth—namely, Energy and Financials, which are the leaders year-to-date.

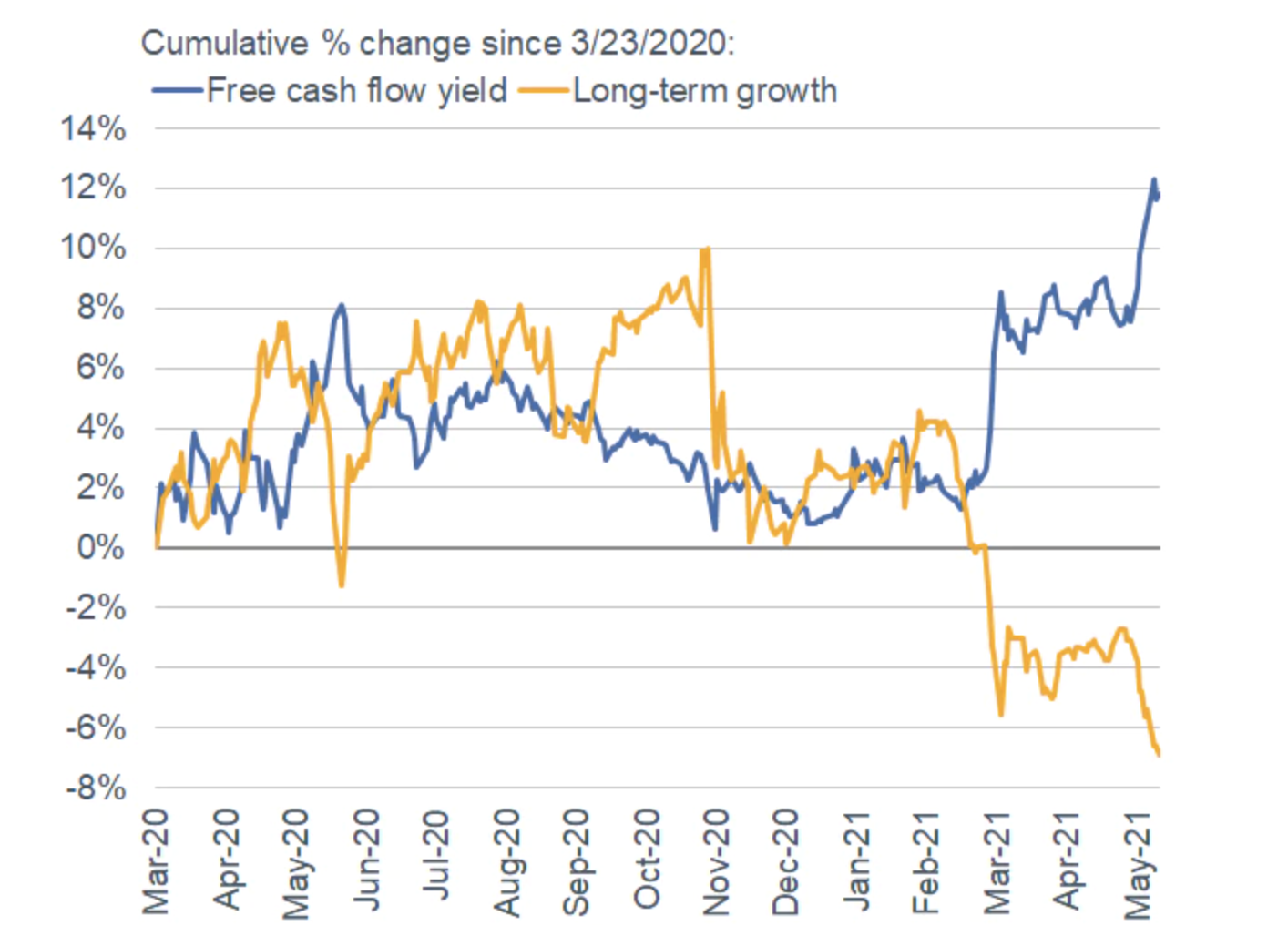

Moving forward, the focus on factors is just as important. We believe value factors—which may be distinct from what is in value indices—will continue to outperform traditional growth factors. You can see in the chart below that long-term growth had strongly outperformed free-cash-flow yield—a typical proxy for value—since last November. Yet that value factor took the lead in mid-February and has outperformed strongly since. In fact, the value factor bias over the growth factor has been evident among all 11 S&P 500 sectors, not just those typically thought of as value-oriented sectors.

Value has outpaced growth significantly this year

Source: Charles Schwab, Cornerstone Macro, as of 5/12/2021. Factors based on sector-neutral S&P 1500. Free cash flow yield is defined as the last twelve months of free cash flow divided by the share price. Long-term growth is defined as mean estimated five-year earnings per share growth. Past performance is no guarantee of future results.

Sectors are still experiencing rapid shifts in leadership, and with the virus and vaccine efforts still the key deciding factors in the economy’s recovery, volatility among the market’s internals may continue—especially if behavioral and attitudinal investor sentiment measures remain stretched.

Global stocks and economy: Inflection point

After delays due to lockdowns, slow rollouts of vaccines, and held-up fiscal stimulus, Europe’s economy is finally turning the corner, leaving its double-dip recession behind. A negative GDP reading of -0.6% quarter/quarter in the first quarter is likely to reverse into positive territory in the second quarter. The easing of lockdowns—propelled by accelerating vaccinations, increased bond purchases by the European Central Bank (ECB), and the coming rollout of Europe’s largest-ever stimulus plan—should aid economic growth. In late April, the brightening outlook led ECB Chief Economist Philip Lane to declare that the economy is at “an inflection point.”

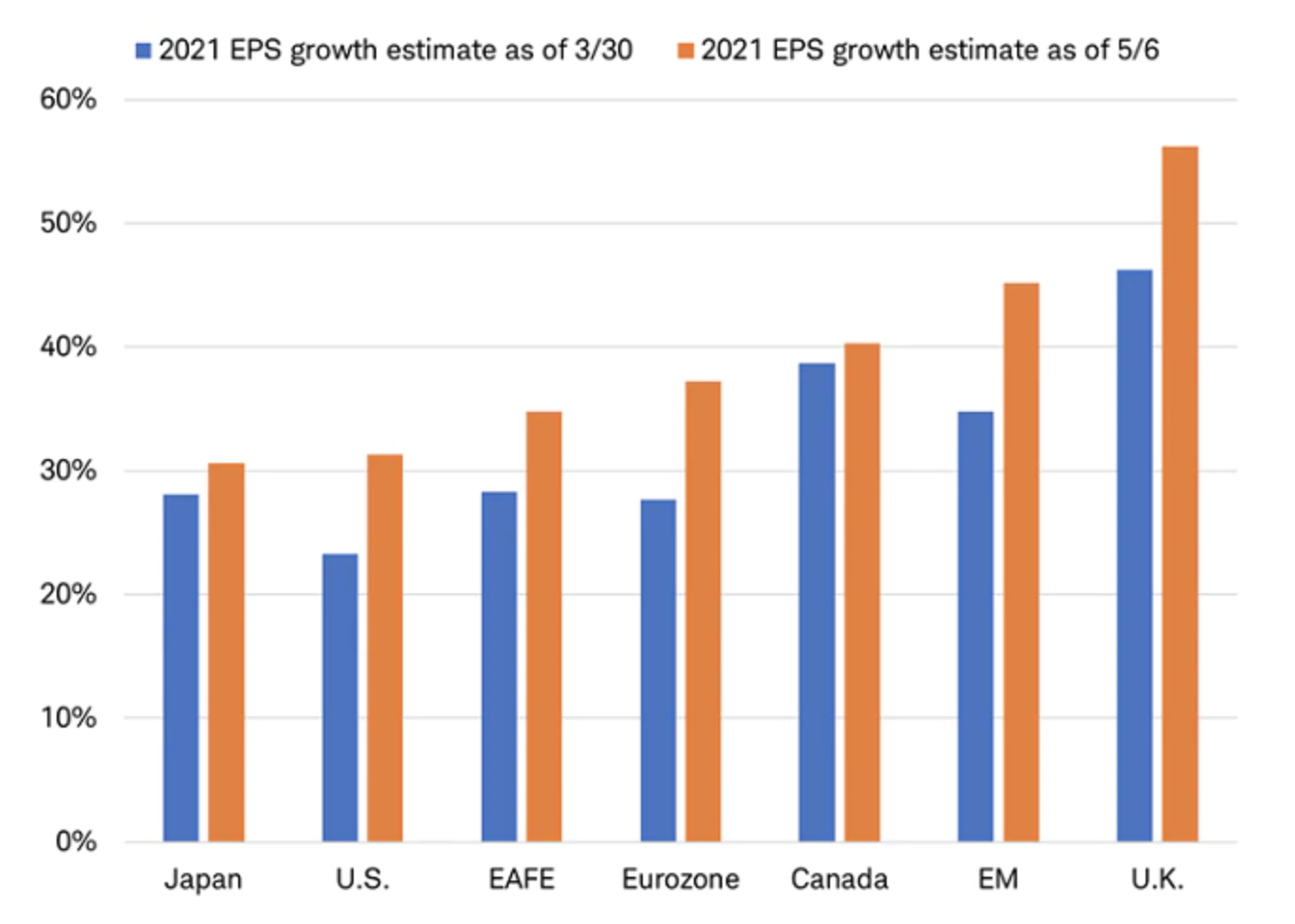

The brighter outlook for Europe is evident in analysts’ forecasts for earnings per share. First-quarter earnings in Europe outpaced those in the United States for the first time in years. Estimates for Europe in 2021—now up 10 percentage points to 38%—have risen the most among developed areas since the end of the first quarter, as you can see in the chart below.

Europe leads the upward revisions to 2021 EPS growth

EM = Emerging Markets.

Source: Charles Schwab, FactSet, as of 5/6/2021. MSCI Indexes used for all countries and regions.

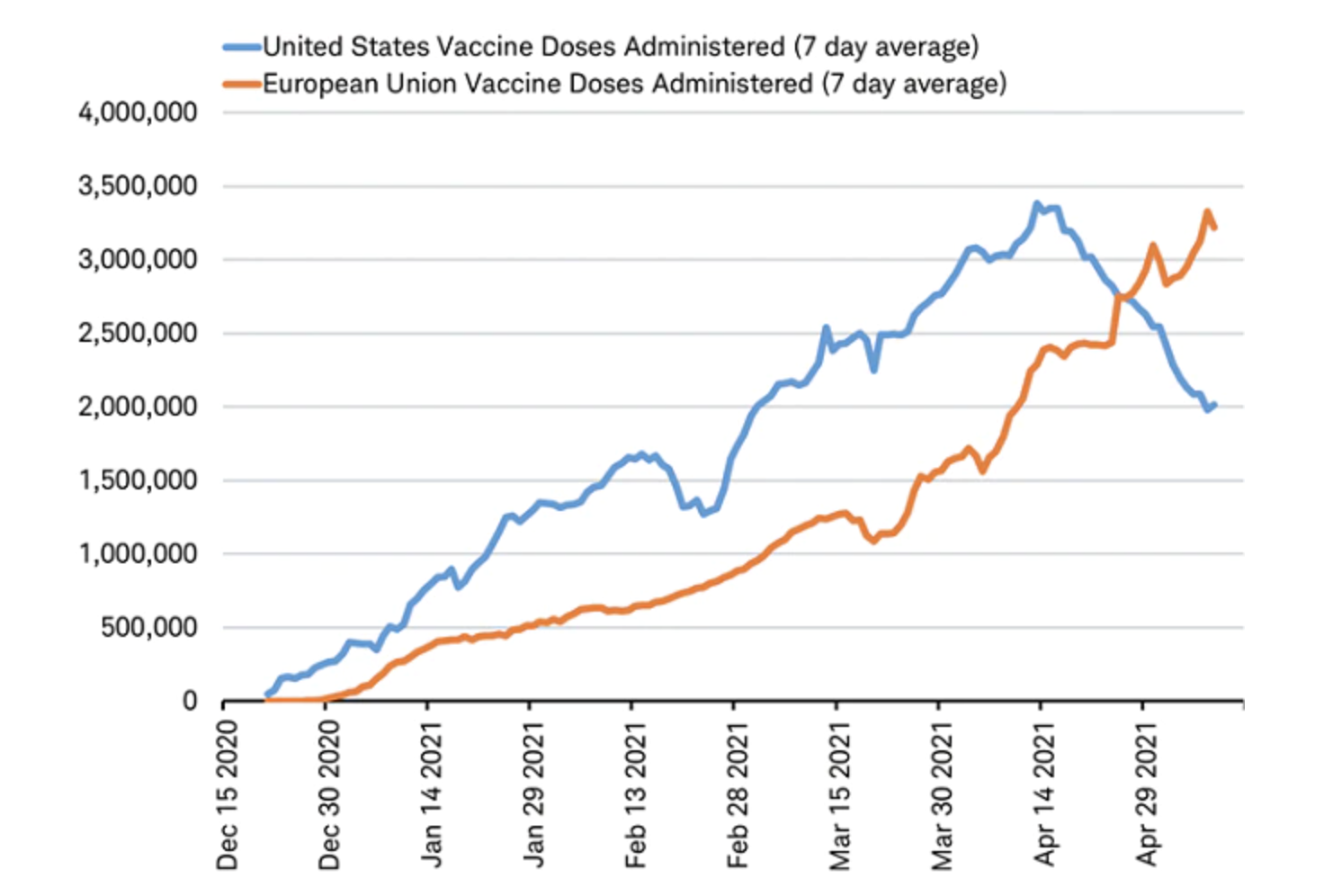

Both the inflection point in GDP growth in the second quarter and continued earnings momentum are dependent upon the vaccination rollout. Securing additional supplies has helped accelerate Europe’s pace of vaccinations. By the end of April, Europe was vaccinating twice as many people per day compared to the end of March. In May, Europe has even outpaced the United States in vaccine doses administered, as you can see in the chart below.

Europe’s accelerating pace of daily vaccinations

Source: Charles Schwab, Bloomberg data as of 5/9/2021.

Like others around the world, Europe’s manufacturers are seeing strong orders on improved demand. Yet, inventories are near all-time lows and tight supplies of several inputs (from semiconductors to workers) may increasingly act as constraints on output. Nevertheless, the supply issues threatening to slow production in manufacturing may be offset by the European Union’s huge fiscal stimulus program and the reopening of its service sector.

Although it was approved last year, plans for the rollout of the rescue program this summer have just been put in place. The delayed fiscal stimulus finally kicking in, combined with re-openings, is expected to revive substantial pent up demand and power a robust recovery that may translate to stock market outperformance this year. Since the start of the year, the blue-chip stocks of the Europe STOXX 50 Index have outperformed the U.S. S&P 500 Index, while the broader Europe STOXX 600 Index has performed in-line.

Fixed income: Range-bound rates

Interest rates have been in a holding pattern over the past month. Short-term rates remain anchored near zero by Federal Reserve policy, while 10-year Treasury yields have traded between 1.5% and 1.7% despite signs of strong growth and rising inflation concerns.

The relative calm in the market likely indicates that the market has already discounted much of the rebound in the economy since last year. With the latest disappointing April employment report, there are questions of a slowdown in the pace of the recovery.

However, we see this as a pause in the upward trend in yields rather than the start of a reversal for three reasons:

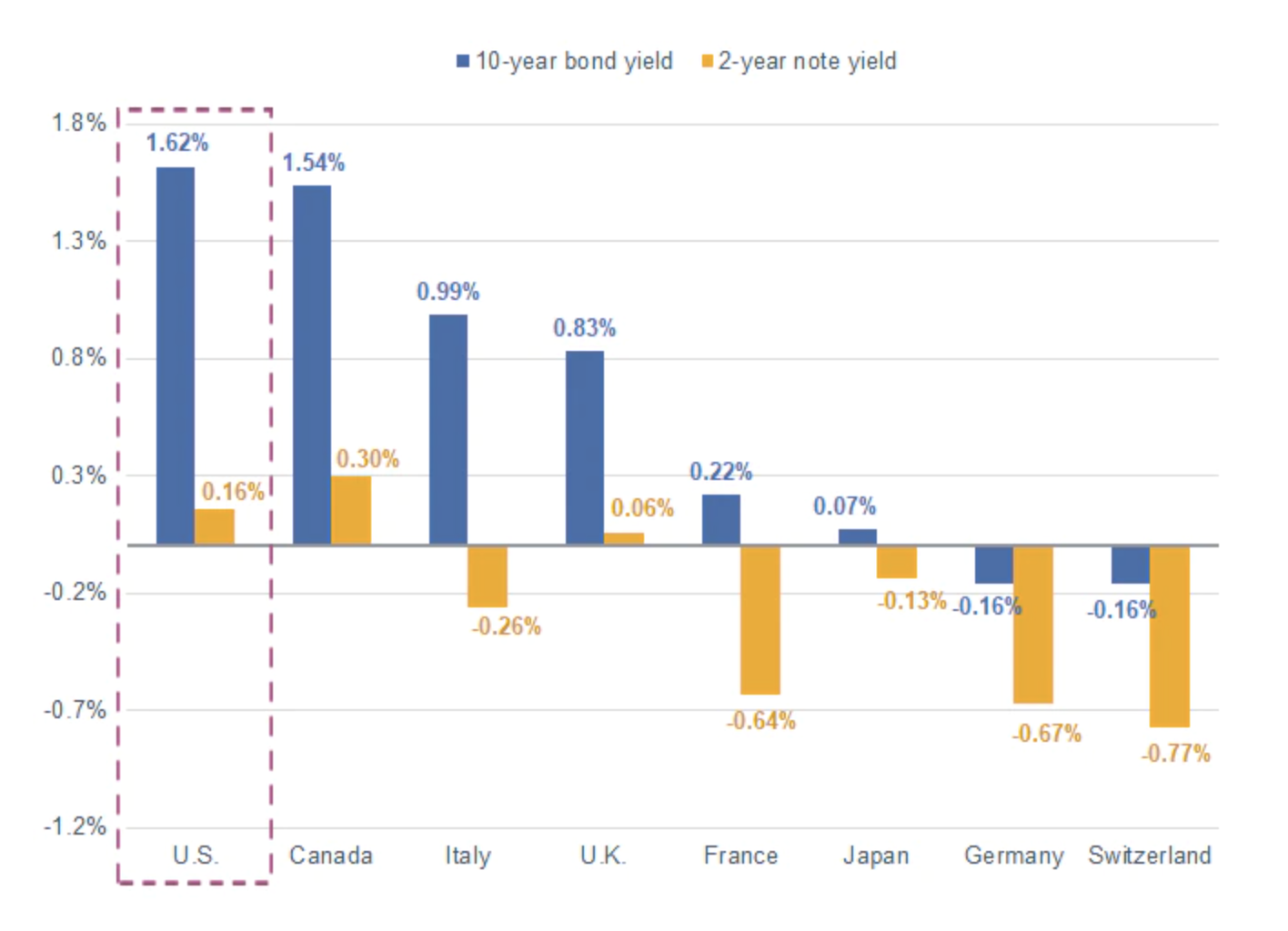

1. The global recovery should pick up in the second half of the year as more widespread vaccinations allow economies to open. Bond yields in other major developed countries will likely move higher as economic momentum picks up. Currently U.S. Treasury yields are significantly higher than those in Europe and Japan. Consequently, strong global demand for U.S. bonds has helped cap yields. In the second half of the year, improving growth should lead to rising global yields, potentially pulling U.S. yields higher as well.

U.S. Treasury yields are above other major developed-country yields

Source: Bloomberg. Data as of 5/11/2021. Past performance is no guarantee of future results.

2. Fiscal and monetary policies are supportive for growth and inflation. The American Rescue Plan should continue to influence consumer spending and aid small businesses and state and local governments. With the pick-up in activity, yields are likely to keep rising.

3. Real interest rates are steeply negative, which isn’t consistent with such strong economic growth prospects. Inflation expectations are rising faster than nominal yields, resulting in negative real yields. Assuming the Fed achieves its 2-2.5% inflation target, nominal yields should rise to at least that level.

Real yields aren't reflecting the strong economic outlook

Source: Bloomberg. US Generic Govt TII 10 Yr (USGGT10Y INDEX). Daily data as of 5/11/2021. Past performance is no guarantee of future results.

For investors, rising long-term yields should present an opportunity to extend duration later this year. For now, we continue to suggest keeping average portfolio duration low.

Senior Investment Research Specialist Kevin Gordon contributed to this report.

© Charles Schwab

Read more commentaries by Charles Schwab