Key Points

-

The recovery is now over; a new global economic expansion has begun. The new economic cycle has seen stock market leadership pass from the U.S. to Europe.

-

A risk to the expansion is the prevalence of COVID-19 variants and the presence of antibodies waning over time which may mean yet another wave of infections in the late fall/winter.

-

A potential positive is that signs signal a deceleration in some of the upsurge in price pressures in the second half of the year which may lessen market worries over the pace of the rebound in inflation.

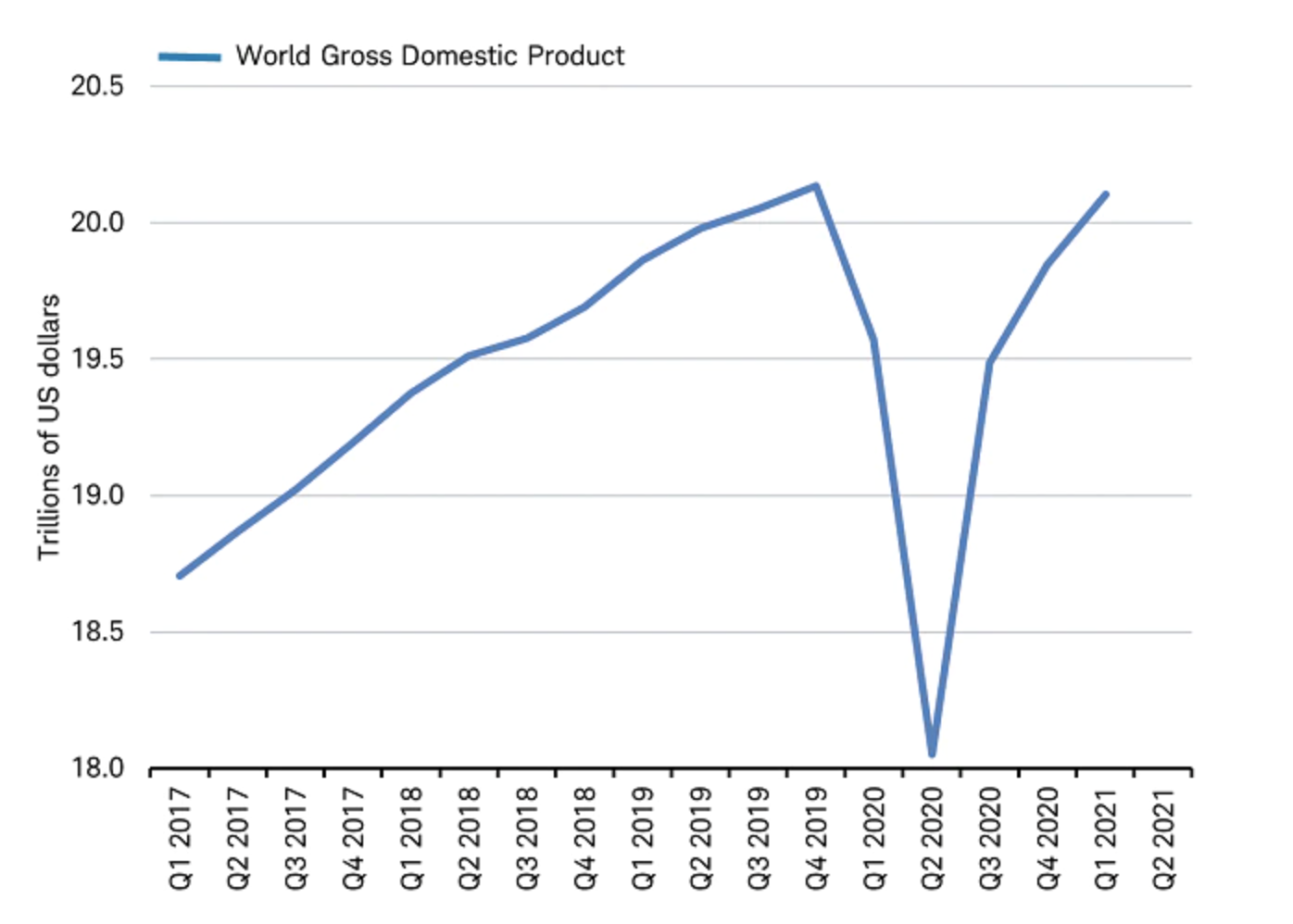

In the first half of 2021, the world economy seems to have rebounded back above its pre-pandemic peak, transitioning from the recovery phase to the start of a new economic expansion. Some countries, businesses and families have not fully recovered from the pandemic-led recession. Yet, overall, global GDP fully recovered by the end of the first quarter and continued economic expansion in the second quarter of 2021 will likely lift output above its pre-pandemic high. This pattern marks the sharpest economic “V” in history, with its deep recession and rapid recovery both contained within just five quarters.

And we’re back

Global Q1 estimate based on official reports for many countries.

Source: Charles Schwab, World Bank data as of 5/27/2021.

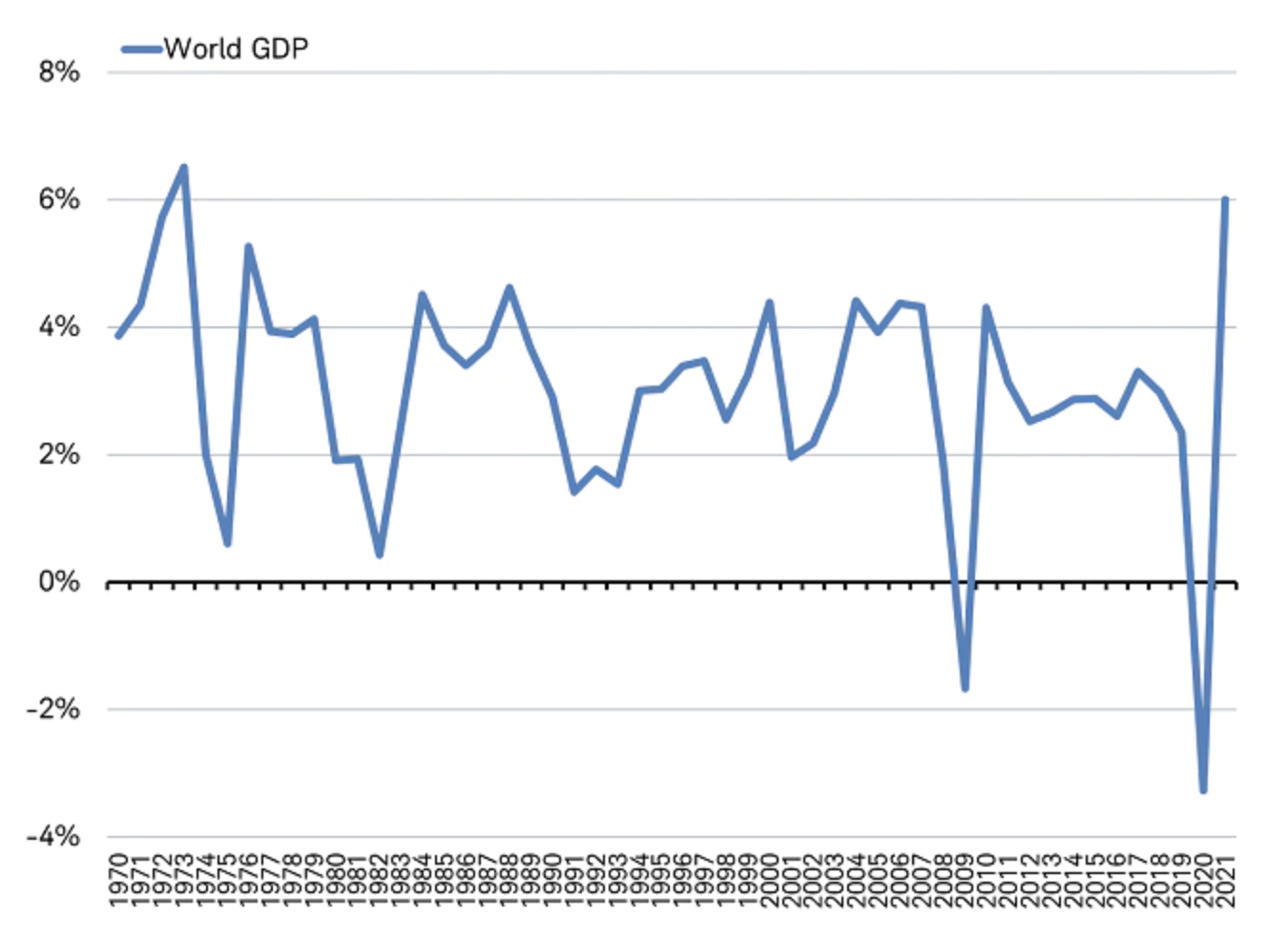

The global growth forecast of 6.0% for 2021 by the International Monetary Fund (IMF) is supported by the global vaccine rollout, expanded fiscal stimulus, business adaptations to the pandemic and the anticipation of a demand snapback as restrictions are eased. If this forecast is realized, it would be the fastest pace of growth for the global economy seen in nearly 50 years, as you can see in the chart below.

2021 growth expected to be fastest in nearly 50 years

Includes IMF forecast for 2021.

Source: Charles Schwab, International Monetary Fund and World Bank data as of 5/27/2021.

European leadership

The new economic cycle has seen stock market leadership pass from the U.S. to Europe this year, as we forecast in our 2021 Global Outlook: New Cycle, New Leadership.

While past performance is no guarantee of future results, the MSCI Euro Index, which tracks stocks in the Eurozone, has delivered a total return of 16.7% in U.S. dollar terms while the S&P 500 Index has managed only 13.3%, year-to-date through June 4. Since the beginning of November, when hopes of COVID-19 vaccines began to boost confidence in the recovery, Eurozone stocks have returned 46.5%, compared with 30.6% for U.S. stocks.

The Eurozone has outperformed even though vaccination programs lagged those in the United States. Ending restrictive lockdowns, ramped up bond buying by the European Central Bank (ECB), and the nearing rollout of Europe’s largest-ever stimulus plan should aid growth heading into the second half of 2021. This may mean the peak in Eurozone economic momentum may not come until later this year, unlike other major economies such as the U.S. where growth may have peaked in the second quarter of this year or China where it peaked in the fourth quarter of last year.

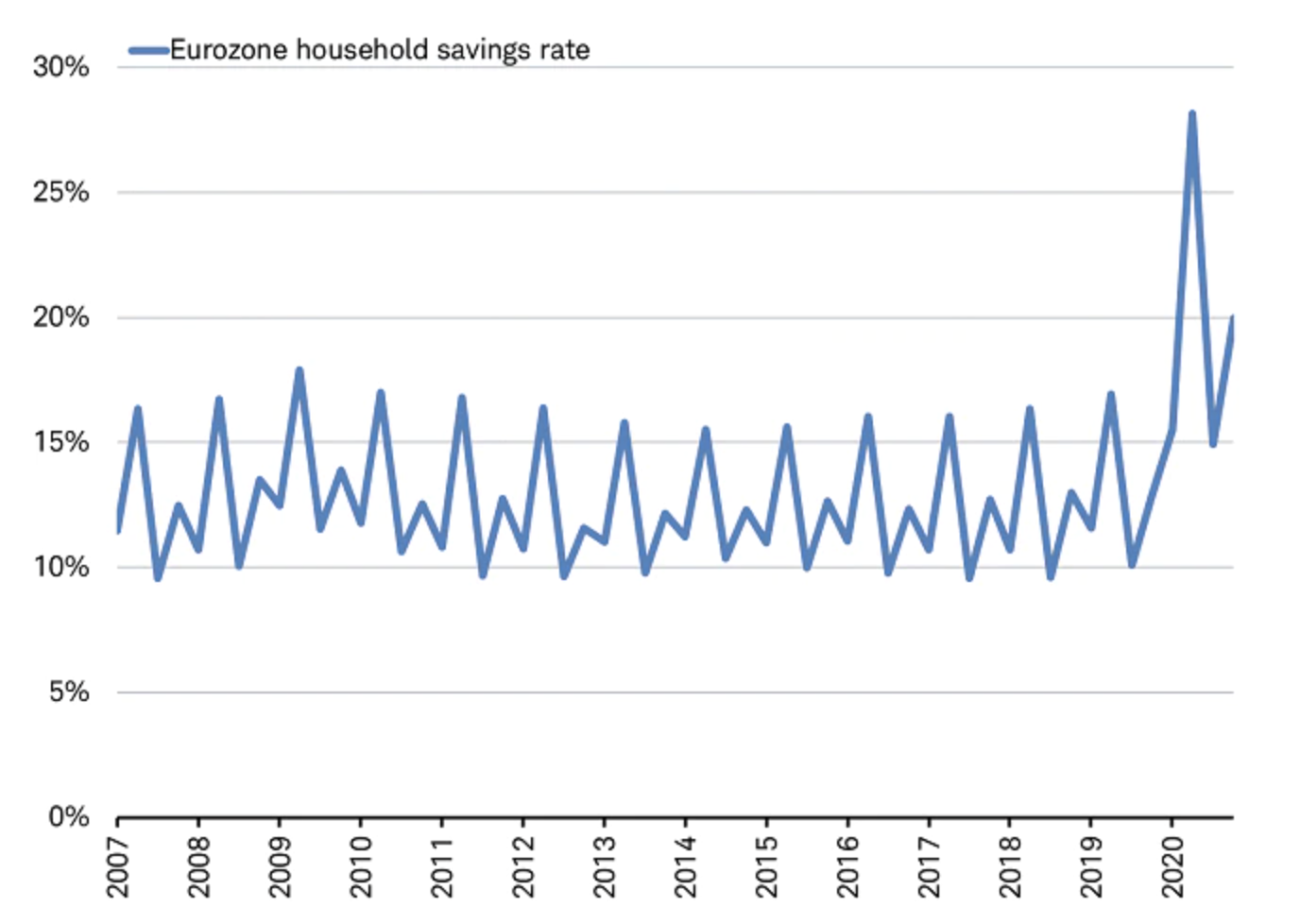

As vaccination programs have accelerated and service industries have begun to reopen, sentiment surveys have rebounded. France’s index of business confidence climbed to its highest in three years in May. Similarly, Germany’s IFO survey of business expectations showed its strongest reading since January 2011. Even more importantly, consumers seem set to unleash pent up demand. Thanks to worker furlough programs relatively few workers lost their jobs in the Eurozone. That resulted in household disposable income rising +0.3% in 2020, despite the deep Eurozone recession that shrank GDP by -6.6%. Last year, savings as a percent of income almost doubled to 20%, ending the year 7.1% above the 20-year average and pre-pandemic level (12.9), as you can see in the chart below. Much of this lockdown-induced excess savings could be deployed in the second half of 2021. Europeans appear ready to spend with May’s Eurozone consumer confidence index reading coming in well above its long-term average. Consumer spending is the biggest driver of Europe’s economy.

Pent up demand

Source: Charles Schwab, Bloomberg data as of 6/4/2021.

Adding further fuel for growth, a year after approval, the European Union (EU) will kick off its Recovery Fund of 806.9 billion euros (about $1 trillion US dollars) by beginning to issue bonds in June. EU countries will soon start receiving those funds to boost economic activity with Italy and Spain as key beneficiaries.

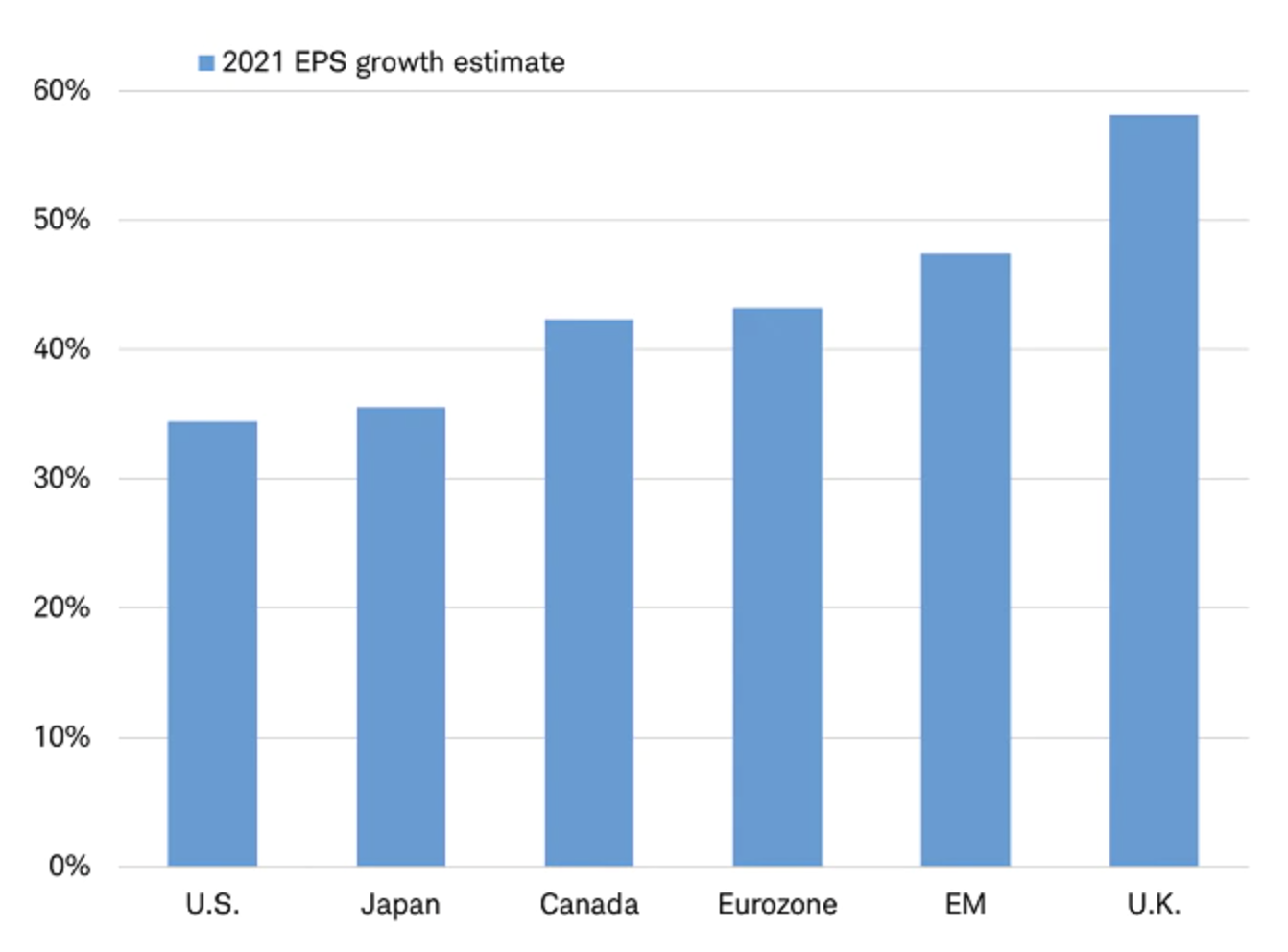

The brighter outlook for Europe is evidenced in analysts’ forecasts for earnings per share to surge to new all-time highs. First quarter earnings in Europe outpaced those in the U.S. for the first time in years. Estimates for Europe in 2021 have risen the most among developed countries since the end of the first quarter; up 16 percentage points to 43%.

Europe leads the upward revisions to 2021 EPS growth

EM = Emerging Markets.

Source: Charles Schwab, Factset, as of 5/26/2021. MSCI Indexes used for all countries and regions. Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly.

Emerging Markets

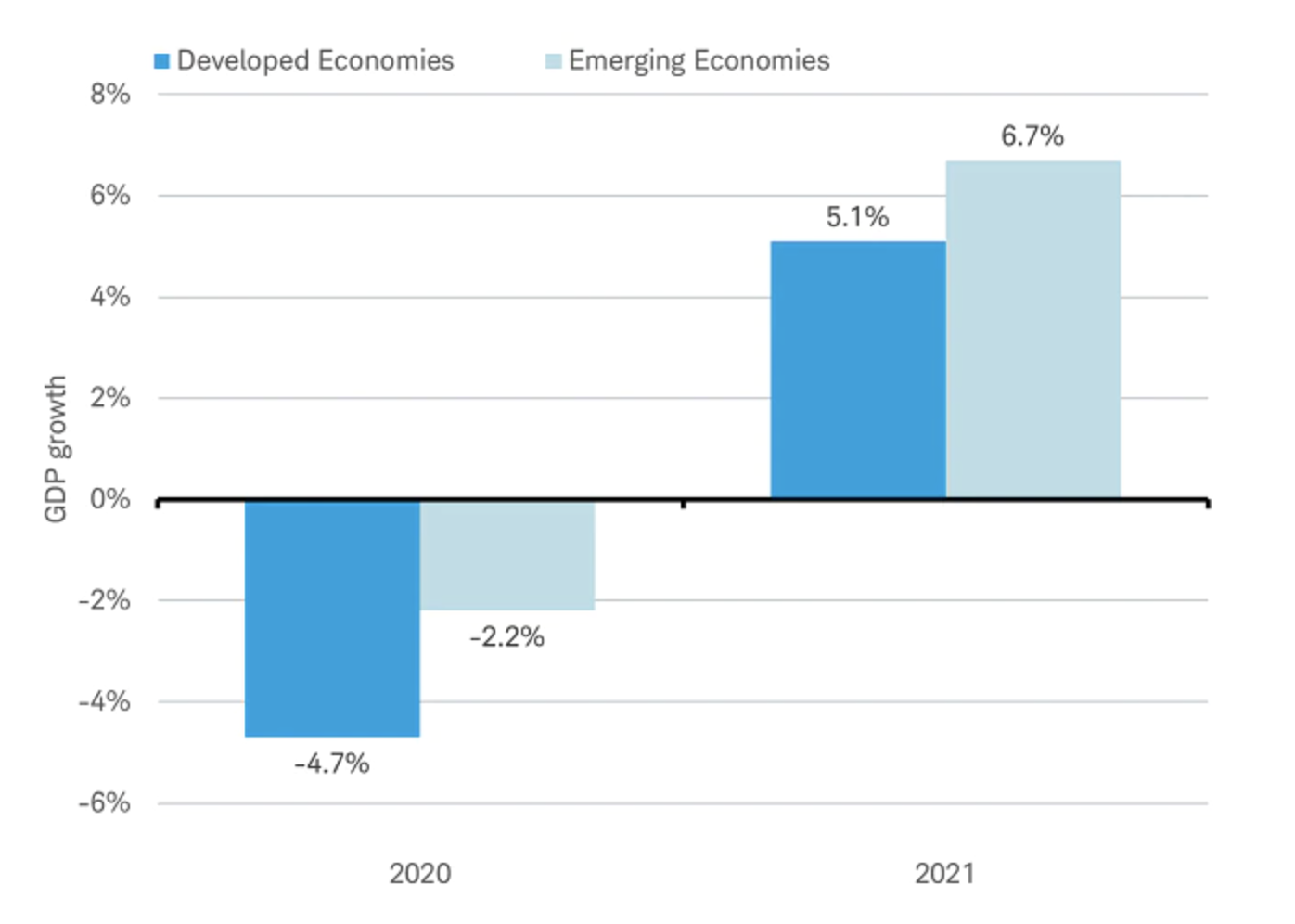

In past global recessions, emerging markets (EM) suffered crises which led to deeper economic declines than in developed markets. They often saw their currencies plunge which also contributed to poor investment performance. This recession, tied to a health crisis rather than a financial one, has been different. As the chart below shows, EM economies suffered less in 2020 than their developed counterparts and are expected to experience more rapid growth in 2021. Currencies have also fared well; the MSCI Emerging Market Currency Index hit a new all-time high in late May.

Emerging market economies besting developed markets in 2020 and 2021

Source: Charles Schwab, International Monetary Fund April 2021 World Economic Outlook data and forecasts as of 5/29/2021. Past performance is no guarantee of future results.

Notably, these countries engaged in much lower levels of fiscal and monetary stimulus than developed nations, avoiding sowing seeds that can lead to potential future financial problems.

Vaccinations

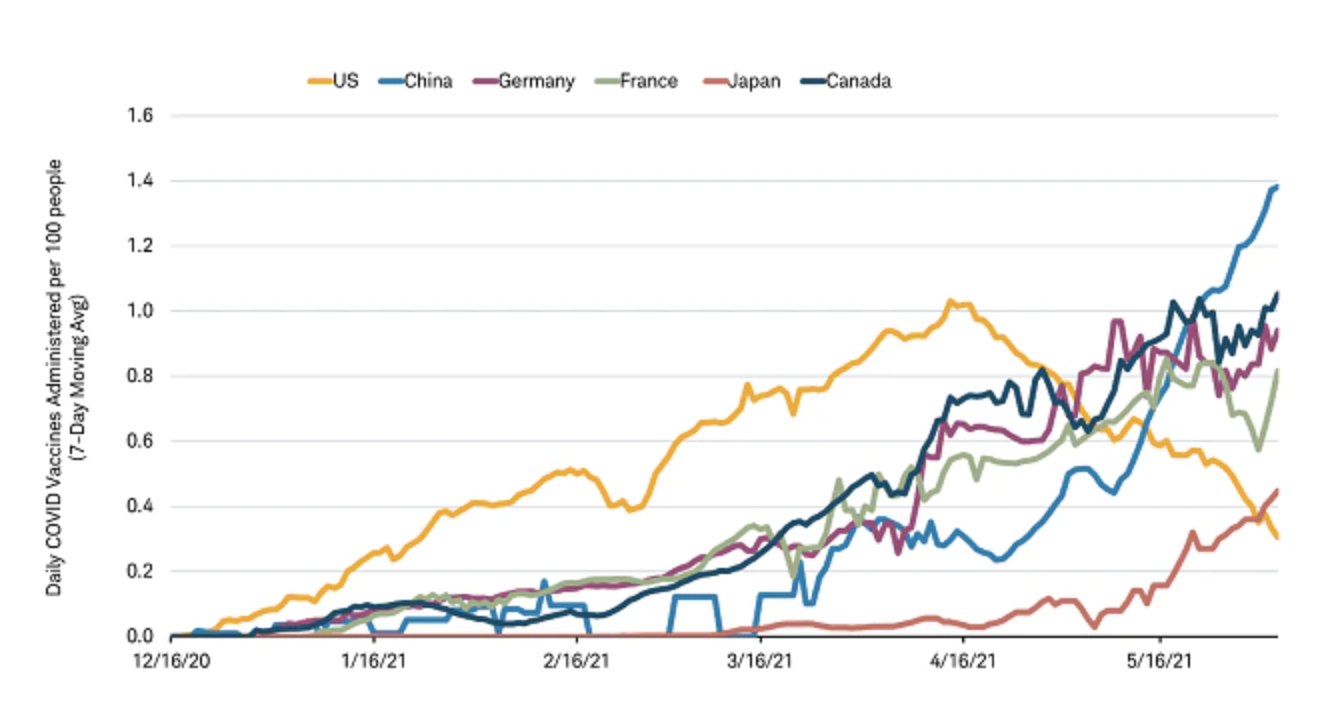

The COVID-19 vaccine rollout had a bumpy start in most countries. After logistics were worked out and production ramped up, the pace of vaccinations increased and aligned with the path to recovery we outlined in our 2021 Global Outlook. Major countries, including China, are on track have more than 50% of their populations vaccinated this summer.

Securing additional supplies has helped accelerate Europe’s initial lackluster pace of vaccinations. In April, Europe vaccinated twice as many people per day compared with March. By May, European nations, along with China, outpaced the United States in vaccine doses administered, as you can see in the chart below.

Vaccinations picking up overseas

Source: Charles Schwab, Bloomberg, as of 6/7/2021.

However, the prevalence of variants and presence of antibodies waning over time may mean the late fall/winter timeframe could see yet another wave of infection. Currently, the vaccines are proving to be very effective against severe cases and appear to provide protection from variants, reducing hospitalizations and the need for lockdowns. In the absence of variants that escape vaccines, economies could face fewer economically impactful lockdowns, even in the face of another virus wave.

Outside of China, few cases of infections among citizens in Asian nations have resulted in little urgency to get vaccinated, but recent outbreaks and restrictions may prompt increased desire to be vaccinated. The global supply of doses is anticipated to ramp up in the fall, but the supplies may be inadequate to include coverage for all countries. Aid by developed countries may be needed for low-income countries to prevent unvaccinated areas from evolving new variants.

Inflation

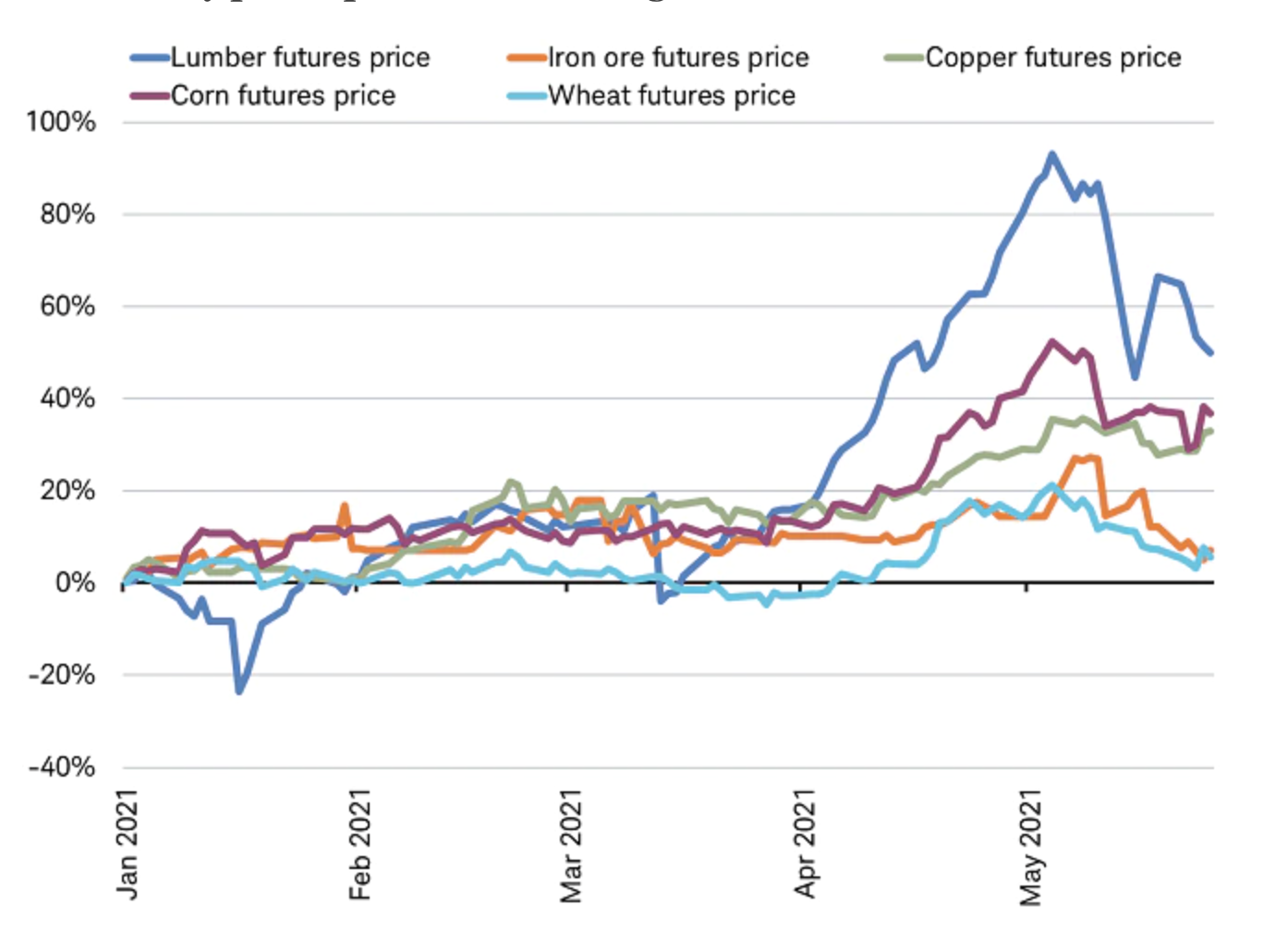

Inflation is rising along with the return of strong growth, buoyed by transitory factors tied to supply chain bottlenecks and easy comparisons to a year ago. As the economic reopening broadens, raw materials and component shortages are expected to improve and supplier delivery times shorten, lessening price pressures. Looking further ahead, inflation is anticipated to settle inside most central banks’ comfort zones.

There are signs inflation’s surge is already proving to be transitory as raw material prices pull back from the highs of early May and supply chains for intermediate goods, like semiconductors, start to improve. Collectively, these factors could moderate the pace of gains in inflation by late summer, just in time for the annual meeting of the world’s central bankers in Jackson Hole, Wyoming.

Commodity prices pullback after surge

Source: Charles Schwab, Bloomberg data as of 5/29/2021.

Inflation is likely to be higher in the years ahead compared to the last economic cycle spanning 2009-2019. Inflation during the last cycle was very low on a historical basis, remaining stubbornly below global central bank targets. If these early signs continue to signal a deceleration of the upsurge in price pressures, the risk of market worries over the pace of the rebound in inflation could begin to lessen.

Takeaways

As the new global economic cycle moves into its next phase, European countries are only now starting to ease their restrictions on economic activity just as Europe’s largest ever stimulus plan is about to be deployed. This suggests Eurozone growth still has some way to go before peaking and that Eurozone stocks can likely still deliver further gains after outperforming in the first half of the year. Strong confidence by business leaders and consumers should help cushion the markets against any soft spots in jobs or manufacturing output. Continued solid growth combined with signs of easing pipeline pressures on prices may ease concerns over the risk of premature policy tightening by central banks that weighed on Emerging Market stocks in the first half of the year.

Michelle Gibley, CFA®, Director of International Research, and Heather O’Leary, Senior Global Investment Research Analyst, contributed to this report.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Currencies are speculative, very volatile and are not suitable for all investors.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see www.schwab.com/indexdefinitions.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

(0621-1EWL)

© Charles Schwab

More Global Markets Topics >