Schwab Market Perspective: Beneath the Surface

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTo get the facts, sometimes you need to look beneath the surface. For example, although the U.S. economic growth rate may be peaking, economic growth itself likely isn’t. Similarly, while it’s natural to wonder how global central banks will manage rising inflation, investors may want to focus on what China’s government is doing to rein in commodity prices. Even in the Treasury bond market, recent calm may be hiding risk below the surface.

U.S. stocks and economy: Peak growth rates

Some key economic data—notably income, spending, and home sales—have cooled lately, reflecting the waning effect of direct government fiscal aid and the fact that we’re likely in an environment of peak economic growth rates. Importantly, that doesn’t necessarily mean we are at peak growth in level terms.

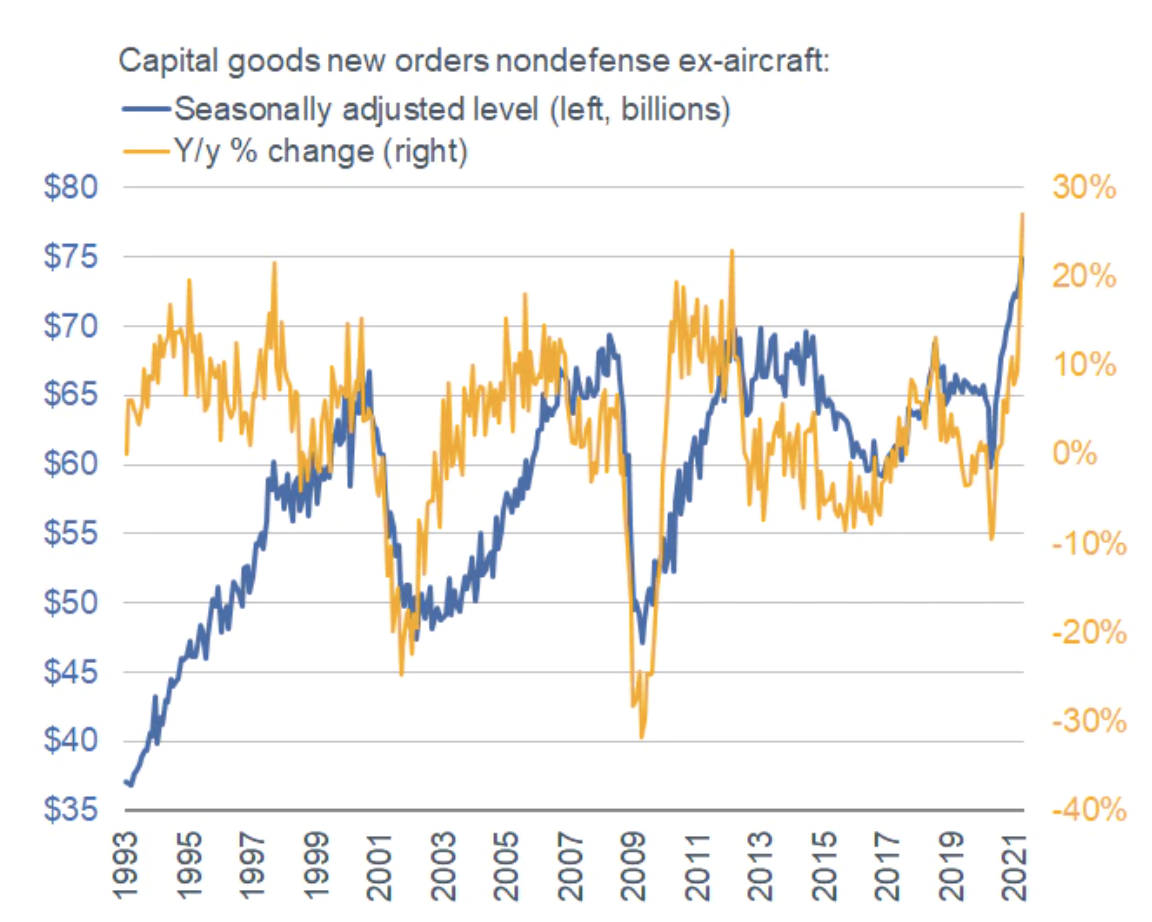

The distinction is crucial, given we continue to see staggering rates of change for data in year-over-year terms. For example, capital goods spending has picked up considerably since the depths of the pandemic. Growth in new orders for non-defense-related capital goods, at 27%, has never been stronger.

Capital spending continuing to break out and strengthen

Source: Charles Schwab, Bloomberg, as of April 30, 2021.

The surging growth rate confirms that business spending has indeed come back to life—aided by companies’ ability to weather the COVID-19 pandemic, the immense amount of aid provided by the federal government, and the more-than-full recovery in goods consumption throughout the past year.

Although double-digit annual growth rates aren’t likely to last forever, the level of capital spending may remain quite strong. This should continue to ease fears of higher, sustained inflation in the long term as companies maintain the ability to provide jobs and remain productive. Undoubtedly, base effects and supply shortages continue to put upward pressure on price measures such as the consumer price index (CPI), but we would need to see an accompanying persistent climb in wages. So far, that hasn’t been confirmed by several wage-tracking metrics, such as the employment cost index, or various business surveys.

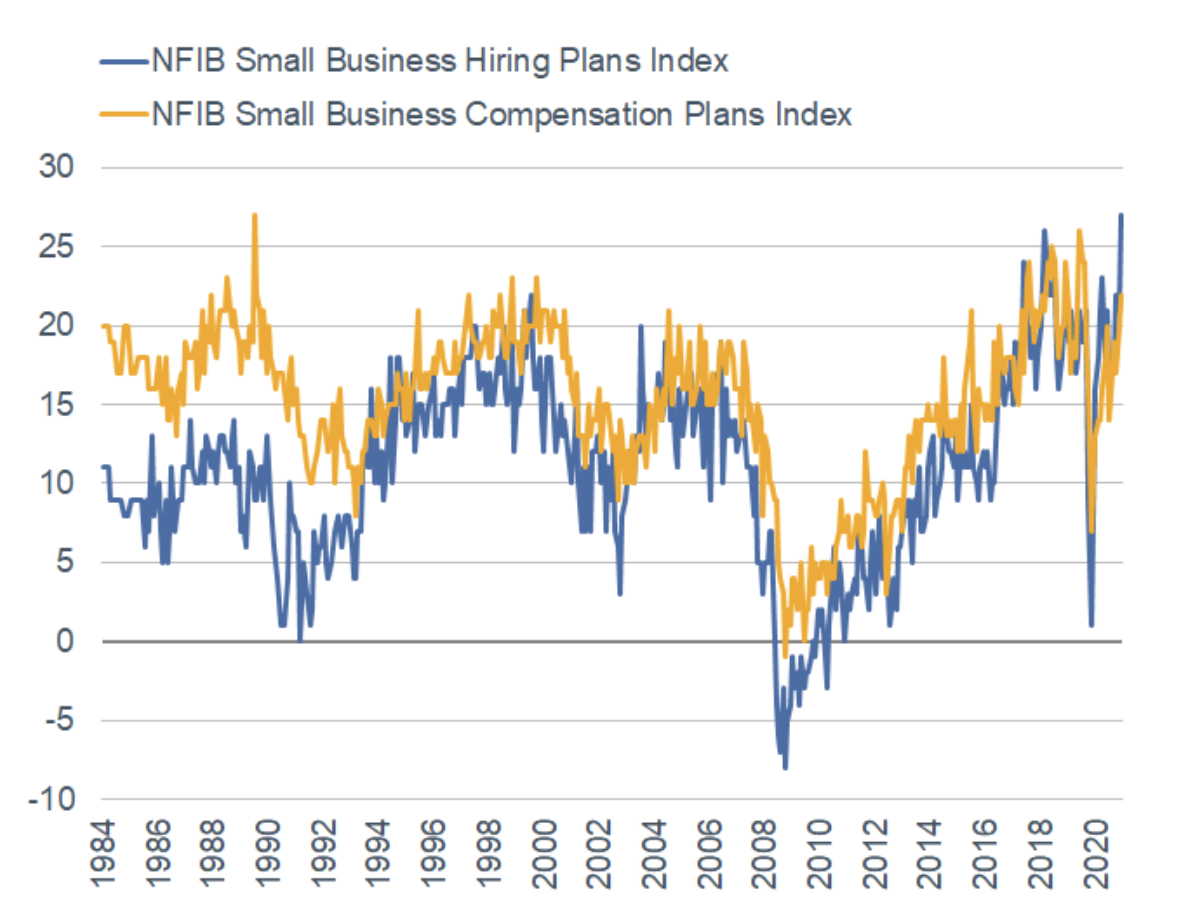

Small businesses continue to say they plan to ramp up hiring, but plans to increase compensation haven’t seen a similar surge. In fact, the percentage of businesses expecting to do so is below its November 2019 peak.

Small business plan to hire, but not necessarily to raise wages

Source: Charles Schwab, National Federation of Independent Business (NFIB), Bloomberg, as of 5/31/2021.

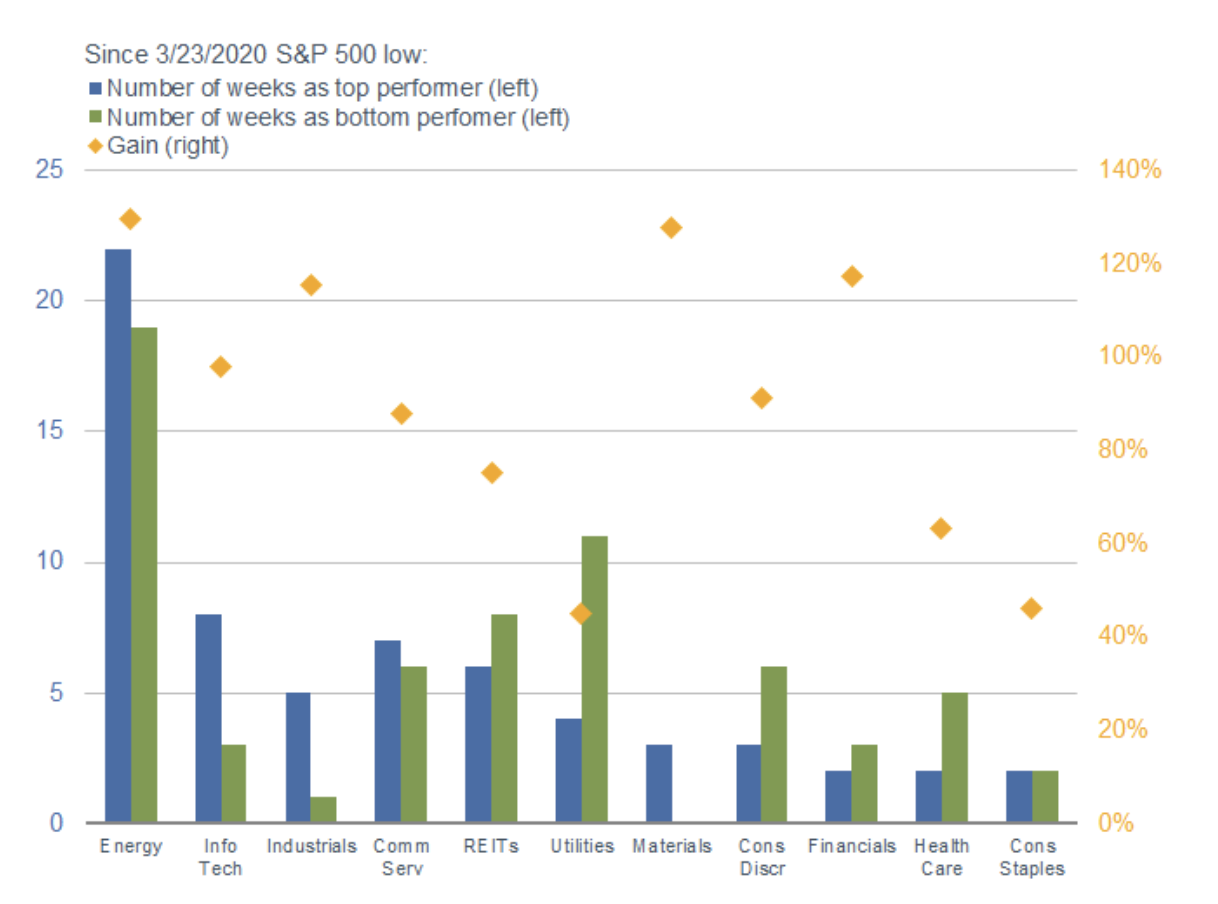

The labor market appears poised to continue to improve, as reflected in the continued decline in weekly initial jobless claims and the still-strong breadth in nonfarm payrolls. That should continue to bode well for the more cyclical and value-oriented sectors of the stock market—typically more sensitive to economic growth, such as Energy, Financials, and Industrials—which remain in the lead since the market’s bottom in March 2020.

Cyclical sectors retain their top spots among sectors

Source: Charles Schwab, Bloomberg, as of 6/6/2021. Past performance is no guarantee of future results.

However, some sectors’ gains have gotten quite stretched. While that confirms that cyclical areas had correctly priced in the strength of the rebound as broader swaths of the economy reopened, it also likely means these sectors have become increasingly driven by momentum. For example, the Financials sector appears to be overbought after outperforming the S&P 500 index during the past year.

Global stocks and economy: Watch China

Rather than ruminating over various central bank communications to see how and when they might seek to manage rising global inflation, investors may want to focus on what China’s government is doing.

While prospects for new fiscal stimulus in the United States and Europe, coupled with existing emergency monetary stimulus, are adding upward pressure to commodity prices, China is pushing back through tighter policy and aggressive regulatory actions—and it appears to be working.

The “commodity super cycle” of the 2000s was driven largely by China’s voracious demand to build. From 2001-2008, the pace of commodity prices was positively correlated to China’s growth, possibly even the only reliable indicator for the country’s economic momentum. But now, China fears soaring commodity prices will feed through to higher consumer prices, acting as a drag on economic growth in an economy now dependent on consumer spending, (rather than government infrastructure investment).

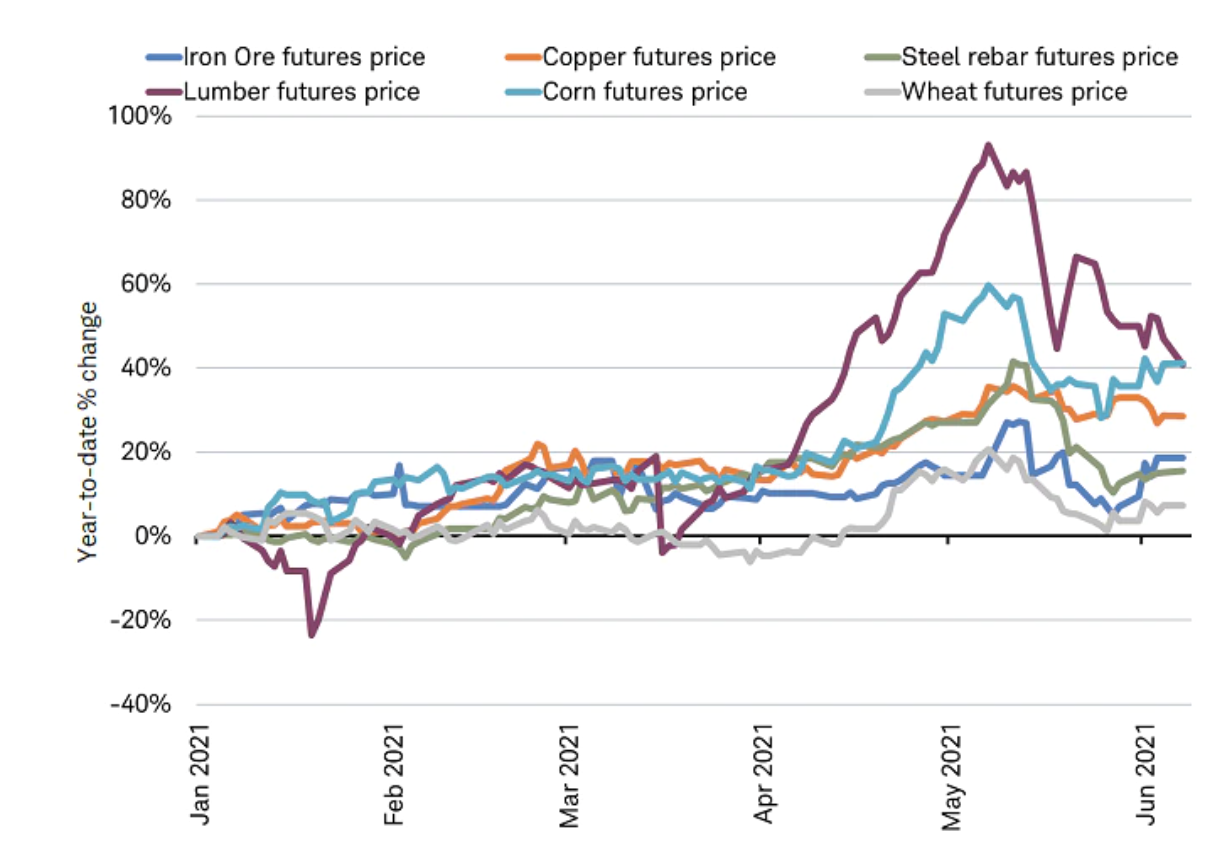

Over the past month, China’s Premier Li Keqiang and other policymakers have focused their messages and actions on reining in the surge in commodity prices. Chinese authorities have raised trading limits, fees, and margins on commodity markets. Trading firms have been asked to cut their bullish best in efforts to keep speculation from driving up costs. Steelmakers have been banned from discussing price hikes, tax rules were changed to restrict exporting, import orders have been slashed to reduce stockpiles, and producers have been compelled to sell inventories.

It appears to be working, given markets from materials to agriculture have pulled back sharply from multi-year highs as China’s crackdown began.

China pushes back

Source: Charles Schwab, Bloomberg data as of 6/8/2021.

While not the only factor weighing on commodity prices, Chinese actions coincide with this year’s price peak:

- On May 10-11, China’s major commodity exchanges increased trading limits, margin requirements and transaction fees on some commodities and pledged to strengthen market supervision.

- On May 14, authorities in China’s steelmaking hub, Tangshan, threatened to revoke steel producers’ licenses if they engaged in “price manipulation.” Steel makers began to reverse capacity cuts put in place last year in compliance with government carbon emission targets.

- During mid to late May, news reports emerged about Chinese customs authorities allegedly restricting imports of corn into free trade zones and cancelling incoming shipments.

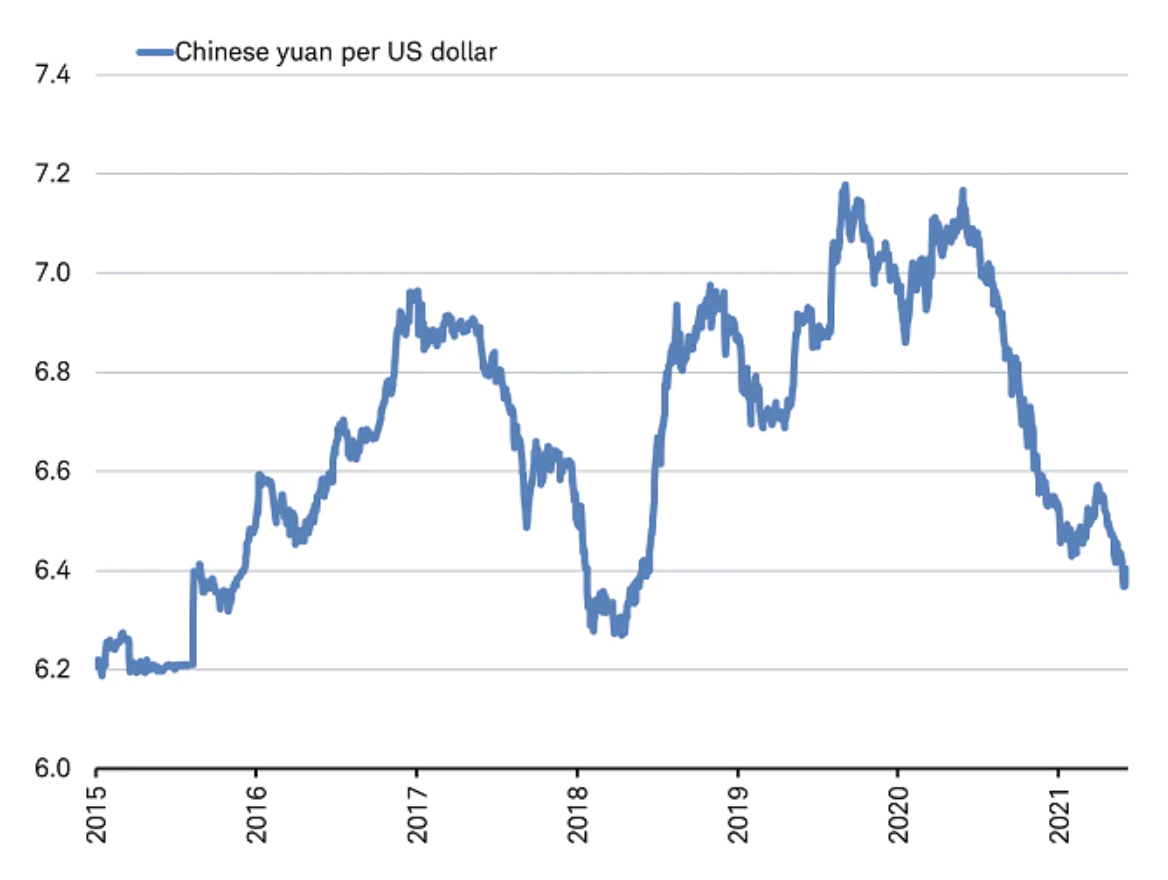

Many commodities have slipped into a bear market, with prices falling over 20% from their peak in early May. However, they have stabilized or crept higher in early June. If trading restrictions by exchanges and other administrative measures fail to keep prices from climbing, China may pursue more powerful tools to keep inflation in check. China could further tighten monetary policy, roll back fiscal stimulus, or let the yuan appreciate considerably beyond multi-year highs to offset the rising cost of imports. Any or all of these actions would need to be balanced against the risk of slowing China’s economy—the outcome they are trying to avoid.

The yuan has strengthened

Note: A declining number of yuan per dollar indicates yuan strength.

Source: Charles Schwab. Bloomberg data as of 6/7/2021.

While China’s administrative actions to control the global market for commodities is limited, an aggressive effort to curb Chinese demand could create enough disinflationary pressure to constrain commodity prices. Investors and central bankers should consider factoring in China’s policy actions when thinking about managing inflation pressures.

Fixed income: Quiet, but with risks below the surface

The recent news in the bond market hasn’t been bullish. Inflation has surged to its highest level in over a decade, economic growth has rebounded on the back of strong fiscal stimulus, and the Federal Reserve is talking about reducing the size of its bond purchases. Yet, 10-year Treasury yields have been stuck near 1.6% for nearly three months.

The key to the market’s calm is the belief that the recent growth and inflation surge will prove “transitory,” as Federal Reserve officials have suggested. While we agree with the transitory view, we still see potential for bond yields to rise in the second half of the year.

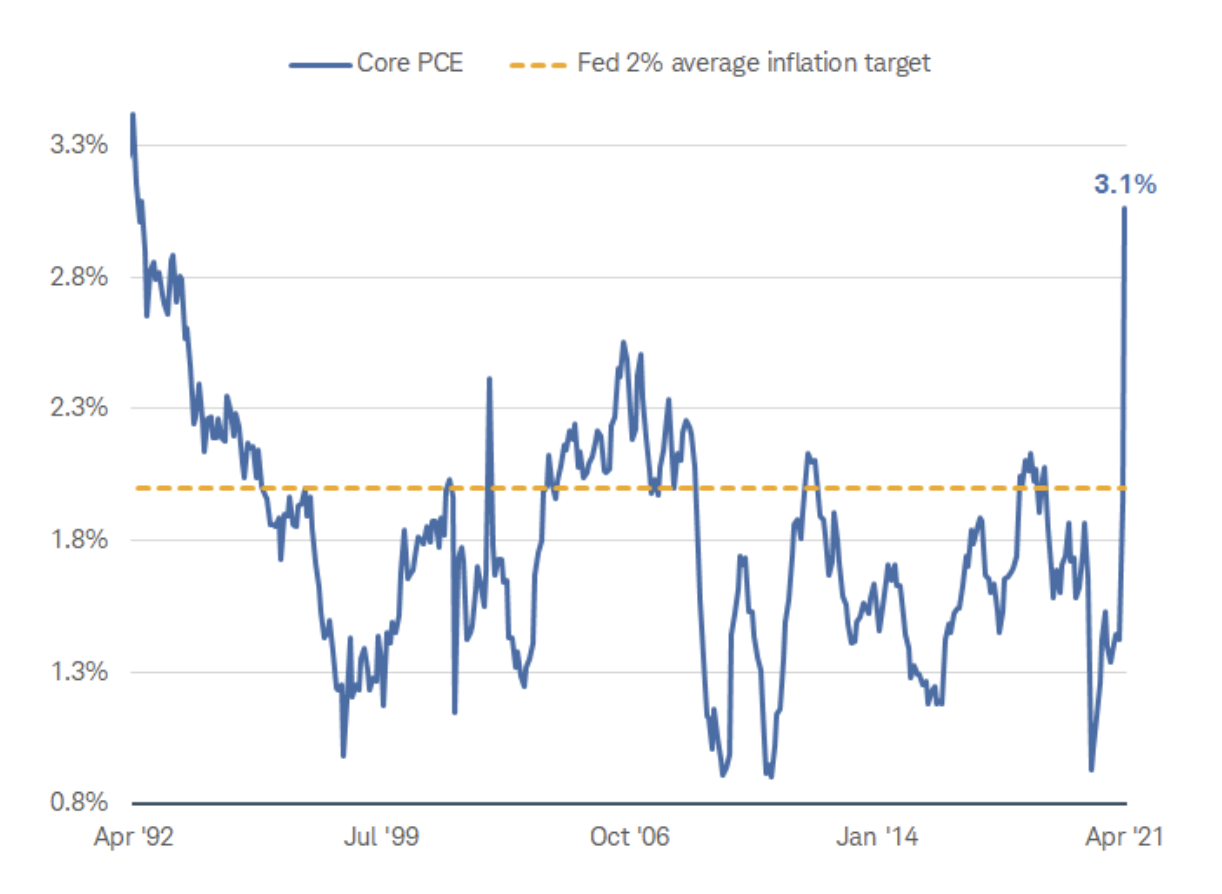

To understand why, we look beneath the surface. The inflation reading that the Fed uses as its benchmark—the personal consumption expenditure (PCE) price index excluding food and energy, or “core PCE” —rose 3.1% year-over-year in April, the highest level since the 1990s. This is notable because core PCE spent most of the past 20 years below the Fed’s 2% target. Much of the year-over-year gain in inflation is attributable to base effects—the comparison to collapsing prices a year ago. In addition, short-term supply constraints for some goods and services have driven up prices and should subside over time.

Core PCE is the preferred inflation measure of the Fed

Source: Bloomberg. U.S. Personal Consumption Expenditure Core Price Index (PCE CYOY Index). Monthly data as of 4/30/2021.

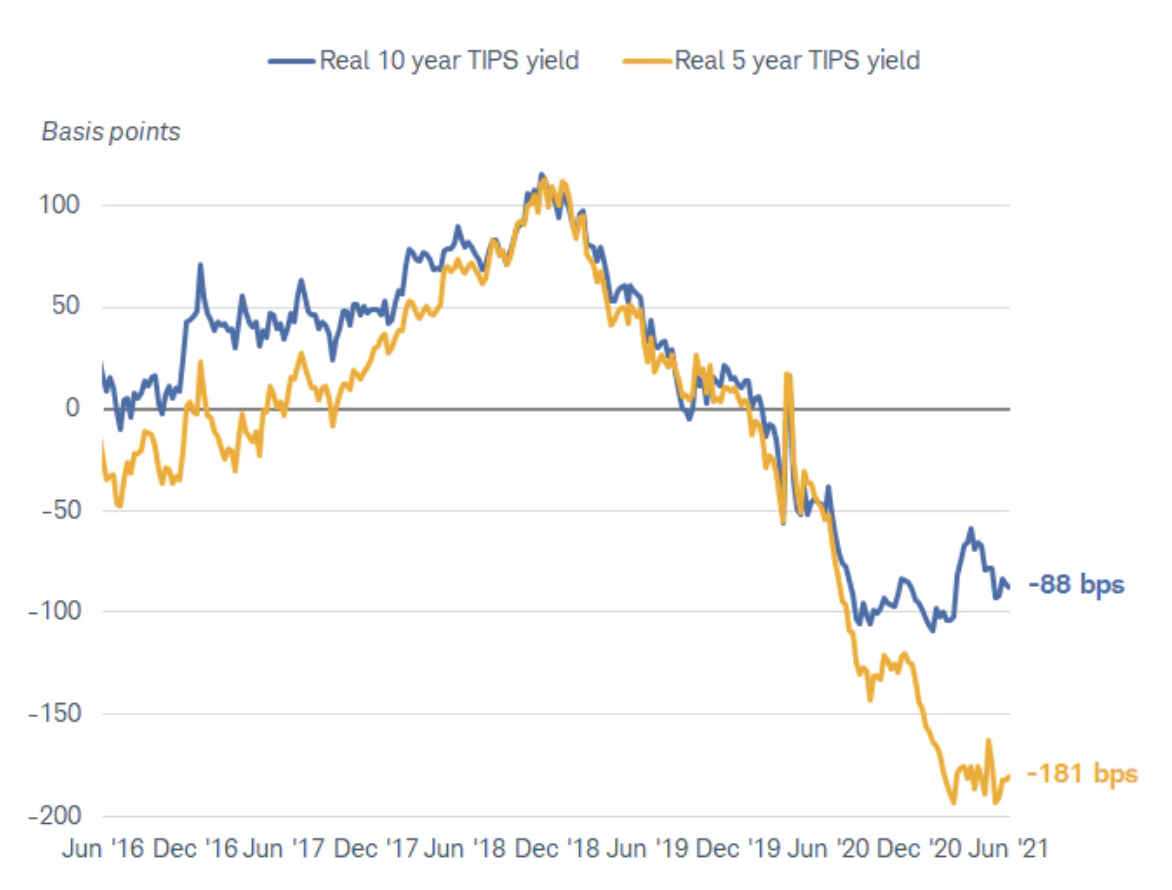

However, we believe that when inflation stabilizes, it may be above 2%. The Fed has indicated it is willing to allow inflation to overshoot its 2% target for an extended time, and ample fiscal stimulus is pushing economic growth to exceed its long-term trend rate. Consequently, we see a risk that inflation could stabilize at a higher level than in the past. Inflation expectations suggest that the market is currently pricing in a rate of about 2.5% over the next five to 10 years. That leaves real yields—yields adjusted for inflation expectations—in negative territory.

Real yields remain deeply in negative territory

Source: Bloomberg. US Generic Govt TII 10 Yr (USGGT10Y INDEX) and US Generic Govt TII 5 Yr (USGGT05Y INDEX). Daily data as of 6/4/2021. Past performance is no guarantee of future results.

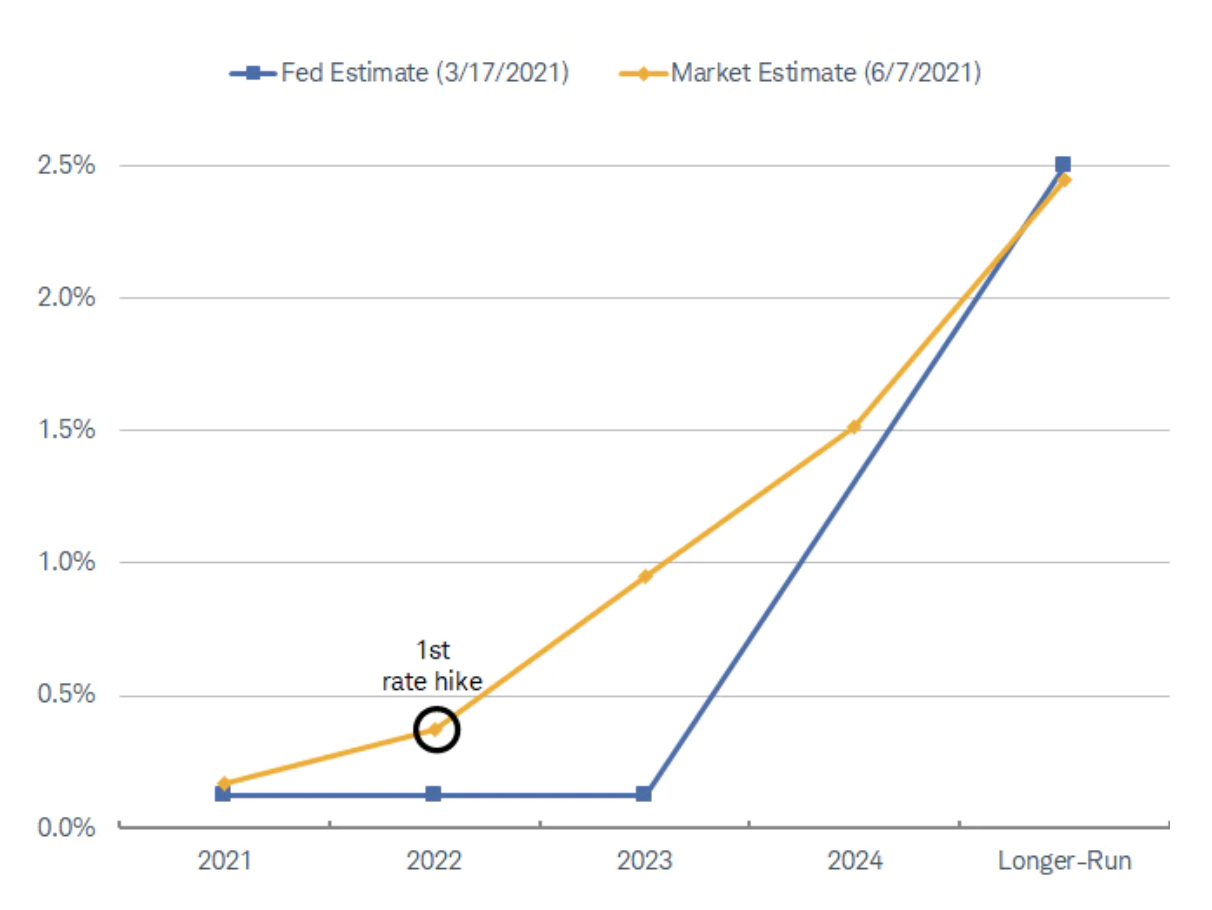

The mid-June meeting of the Federal Open Market Committee (FOMC) likely will result in no change to current interest rate policy, but expectations for the timing of its initial rate hike for this cycle could be pulled forward from beyond 2023. The markets are estimating “lift off” in late 2022.

The Fed versus the market

Note: The “forward curve” represents future interest rates implied by the market for interest rate swaps. Market estimate for "Longer Run" represents the Euro Dollar Synthetic Rate (EDSF) for December 2027.

Source: Bloomberg. Fed estimate as of 3/17/2021, market estimate as of 6/7/2021.

The Fed is also likely to reveal its plans for reducing the size of its bond purchases soon. We expect the process to be gradual and don’t anticipate a major market reaction. Unlike the 2013 “taper tantrum,” it won’t come as a surprise, and yields are well above the recession lows. Nonetheless, we do expect bond yields to rise moderately over the second half of the year. At current levels, bond yields are inconsistent with a strengthening economy, increasing supply of Treasuries to be absorbed by the market, and the risk that inflation settles at higher than 2% longer-term.

We continue to suggest that investors keep the average duration of their bond portfolios below their preferred benchmark. The combination of easy monetary policy and expansive fiscal policy provides a positive backdrop for corporate and municipal bonds. Although yield spreads relative to Treasuries in those markets are low, we don’t anticipate a significant widening and maintain a neutral view.

Senior Investment Research Specialist Kevin Gordon contributed to this report.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All