Earnings Bounce Poses Quality Test for Equity Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs the world convalesced from the pandemic, stocks advanced in the second quarter and earnings rebounded across sectors. With business gains broadening amid complex market risks, we think investors should lean on quality to find stocks that will perform well in a normalizing world economy.

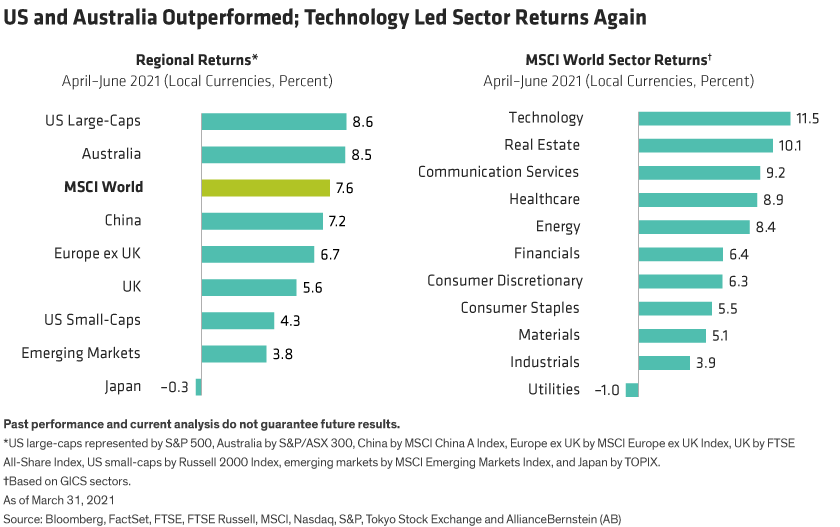

Global stocks continued to rise in the second quarter. The MSCI World Index advanced 7.6% in the three-month period through June in local currency terms, and was up 14.2% since the beginning of the year. US and Australian stocks led the gains, while emerging markets and Japan underperformed (Display, left). Technology was the top performing sector again after a relatively weak first quarter. (Display, right). Real estate stocks staged a robust rebound from last year’s underperformance, helped by growing evidence that the sector’s worst-case outcomes are less likely post-pandemic.

The global economy is progressing through the reopening phases in fits and starts. Some countries have seen rapid progress in containing COVID-19 through successful vaccination programs, while others faced setbacks as new variants emerge. Similarly, in equity markets, style leadership was volatile. Value stocks have been the best performing strategy this year, but lagged in the second quarter (Display). In fact, quality stocks—typically the most consistent performers through cyclical changes—performed well in the second quarter and through the rotation from growth’s dominance in 2020 to value’s reawakening.

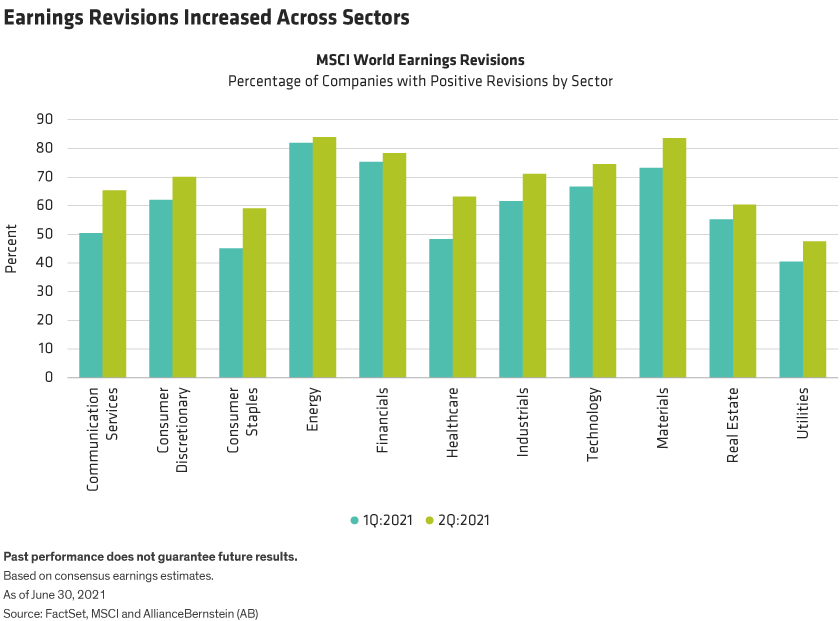

Market gains were fueled by a return-to-business boom as economies reopened and consumers unleashed pent-up spending. This was reflected in earnings—where, globally, the percentage of companies that have seen upward earnings revisions has risen across every sector (Display). According to our research, many companies that suffered negative revisions in the first quarter enjoyed positive revisions in the second, indicating a healthy broadening of profit growth.

The earnings landscape is reshaping the equity investing environment. During 2020, earnings estimates of MSCI World companies for 2021 dropped by 15%, while the index advanced by 14% in US dollar terms. As a result, the benchmark’s price/earnings ratio surged by 35%. This year, earnings estimates for 2021 rose 13%, while the market increased by 12%—leaving the P/E unchanged.

What do these trends mean? First, last year’s share price gains were predominantly driven by multiple expansion—not by earnings growth, largely on the back of lower interest rates. Second, during the collapse, investors focused on companies whose long-term success wasn’t affected by the short-term economic disruptions, favoring many superstar growth companies whose earnings are far out in the future. Today, share-price gains are more closely linked to current and near-term earnings trends, which is in line with more normal market behavior.

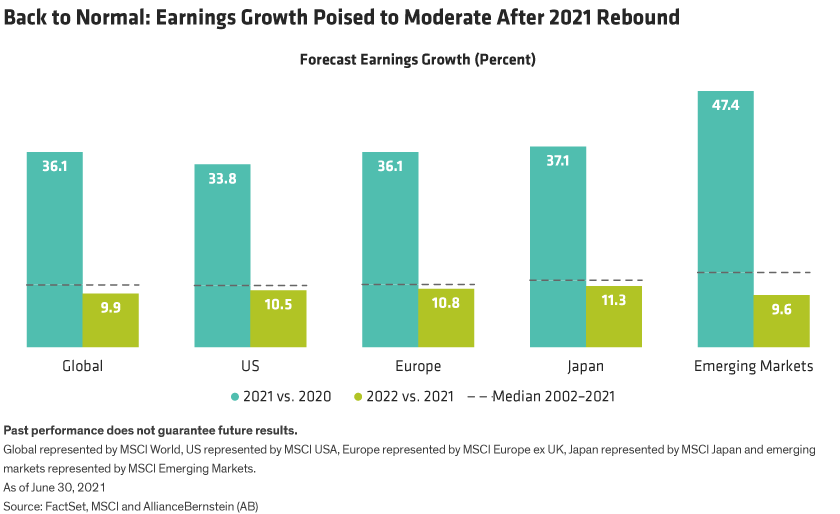

This return to normal poses a test for investors. After this year’s rebound from a dramatic pandemic-induced collapse, earnings growth is forecast to fall back to more normal levels in 2022 (Display). As a result, investors will need to sift for companies with sustainable business drivers and competitive advantages to support healthy long-term cash flows when the initial recovery boost subsides.

But the path from recovery toward normalcy raises questions. Navigating the economic cycle is tricky, as the unique nature of the coronavirus crisis may have unanticipated and lasting impacts on companies and industries. In addition, the threat of inflation and monetary policy changes is palpable. Meanwhile, in many sectors and industries, valuations remain elevated.

Is This Cycle Different?

Macroeconomic cycles usually provide investors with important clues for market trends. For example, in the US, our research shows that the purchasing manager’s index—a key leading indicator for the stages of an economic cycle—is often a good way to identify effective equity return factors. Over three decades, cyclical value stocks have typically done best during recoveries from recession, while growth stocks excelled when economic growth moderated and defensive stocks led in the expansion and contraction stages. Quality stocks are rarely the stars of the stock market show but tend to be relatively resilient through all four stages.

COVID-19 may have upended some of these trends, at least for now. Indeed, in contrast to the historical evidence, growth stocks thrived during the pandemic in a major global GDP contraction while defensive stocks underperformed. The PMI itself may be distorted by massive central bank actions undertaken to help keep the global economy afloat.

Growing concerns about inflation add another risk to the outlook. Signs of inflation continued to accumulate in the second quarter, with the US Core Consumer Price Index registering a 0.7% month-on-month leap in May, marking a 3.8% year-over-year increase—its highest annual rate in 25 years. Research by AB economists suggests that this jump is temporary, and historical evidence indicates that, as long as inflation doesn’t rise above 4% for a prolonged period of time, equity returns should not be threatened.

In mid-June, stocks briefly fell and shorter-term bond yields rose when the US Federal Reserve signalled a possible change in its policies. US Fed Chairman Jerome Powell said that the Fed was considering tapering purchases of Treasuries and mortgage securities, and several Fed board members brought forward their forecasts for when policy interest rates would rise. These moves prompted an outperformance of growth stocks in June, probably because they reduced fears that inflation could get out of control, leaving longer-term interest rates lower than at the start of the quarter.

Macroeconomic uncertainty adds risks to equity markets, while elevated valuations are a lingering concern. At the end of June, the MSCI World Index traded at a price/earnings ratio of 19.8x (Display, left), toward the upper end of its historical range since 1996. However, regional valuations remain diverse. Stocks in the Europe, Asia and emerging markets trade at deep discounts to the global index, and, in most cases, well below their average historical discount (Display, right). It may be a good time for investors who have been underweight non-US stocks to diversify global allocations, in our view.

Quality Matters in the Next Phase of Recovery

No matter where you invest, we believe focusing on quality is essential today. In different regions and across value, growth and lower-volatility stocks—companies that score high on quality—have a better chance of delivering more consistent results over time, in our view.

But identifying quality can be tricky, and its definition may need to be adjusted for investment style or context. For example, among value stocks, we believe that lower leverage, capital discipline and higher profitability—measured by return on equity—are good quality indicators; our research shows that value stocks with the highest free-cash-flow yields and the highest return on equity (ROE) have delivered strong returns in recoveries from previous recessions. Profitability indicators such as return on assets and return on invested capital are good guides for growth companies. But beyond any specific metric, quality is really defined by the caliber of a company’s competitive advantages, innovative capabilities and management skill. Good companies win over time.

Finding companies with these traits is always important, but especially so given the uncertainties that prevail about the outlook today—and the potential for a correction after a prolonged bull run in the markets. Investors should check that their portfolio managers are applying a coherent definition of quality—backed by fundamental research—in their stock-selection process.

Instead of trying to time the rotation between growth and value stocks, we believe that diversifying exposures to different types of equities can be effective when complemented with a quality tilt. By focusing on quality stocks—regardless of style or sector—investors can identify the most resilient return potential as the world faces unusual economic, policy and business hurdles along the path back to normal.

Chris Hogbin is Head of Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All